2014 has been a great year for SaaS companies. By my count, 9 of them will have gone public. Meanwhile, SaaS companies in both the public and private markets continue to fetch premium valuations.

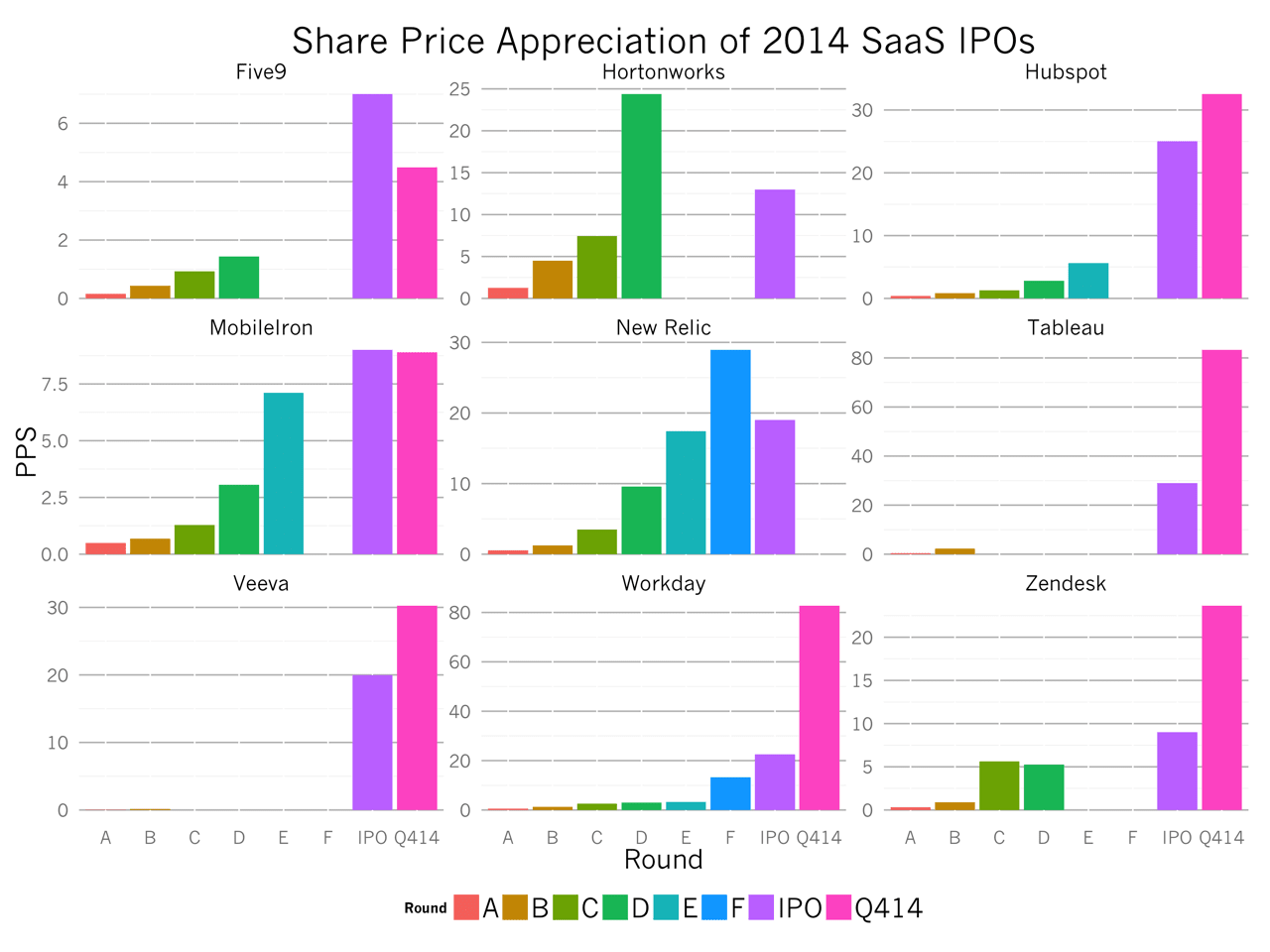

To illustrate the rapid appreciation in the value of these SaaS companies, I’ve plotted the share price by round of each business. The color bars in the chart represent Series A, B… through to IPO. The last bar, called Q414, is yesterday’s share price (if the company has already IPO’ed).

A few interesting trends emerge from the data:

First, the two last IPOs, New Relic and Hortonworks both have priced their IPO at below their last round price. On paper, the investors participating in the Series F of New Relic and the Series D of Hortonworks seem to be underwater.

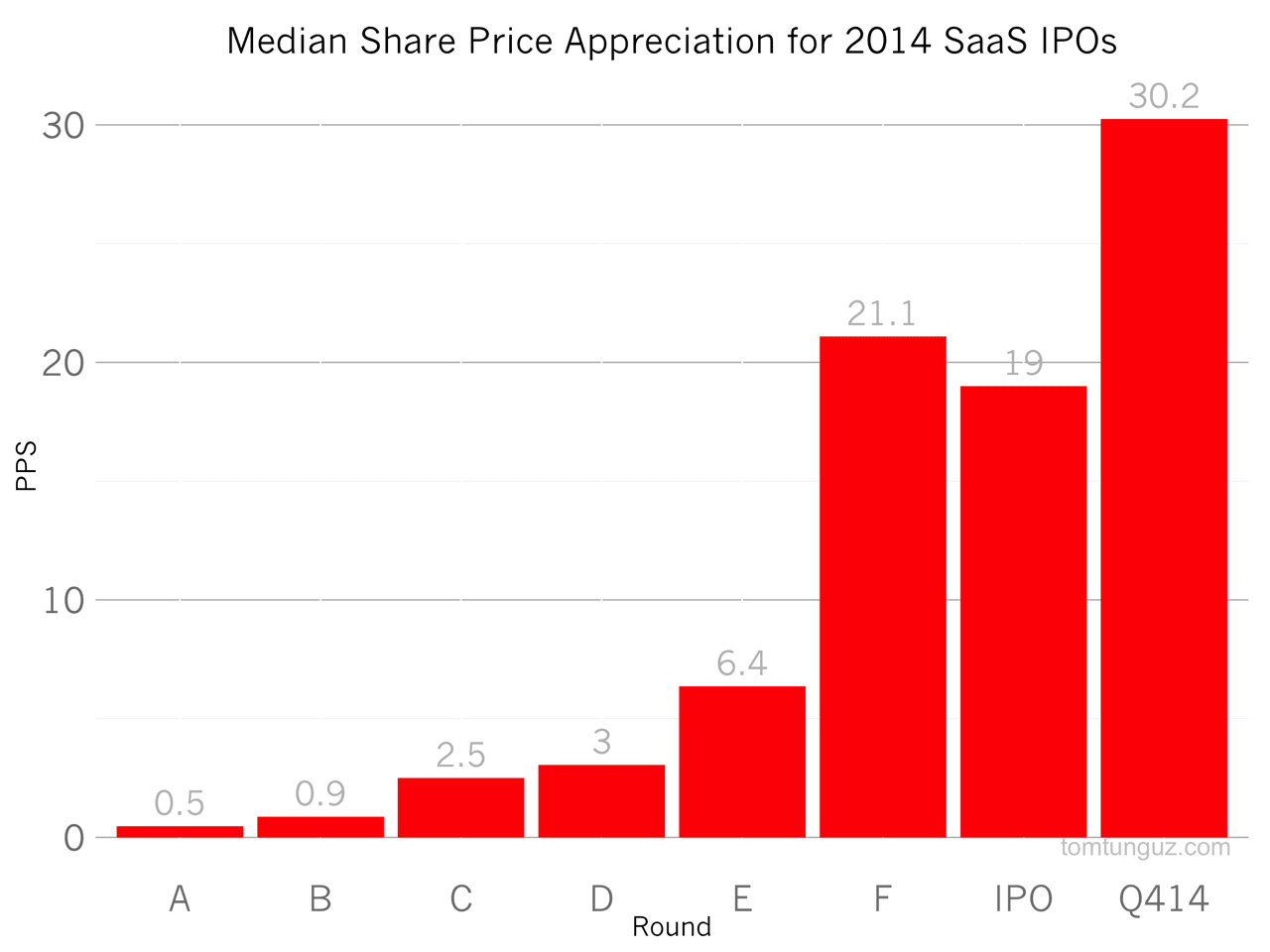

Second, once these SaaS companies trade in the public markets, they pop. The median appreciation in share price from IPO to today is 52%. The average is 95%. In other words, the shares of these companies are worth 50-100% more than at IPO. I’ve plotted the median share price by round below:

If the same patterns hold true for New Relic and Hortonworks, then the last investors in those businesses should see positive returns from their investments. I wonder if Hortonworks will see the same pop given the gross margins (35%) are substantially below SaaS norms of 65-70%, but we’ll know very soon.

Third, the average SaaS IPO in 2014 raised 4 rounds of capital. Two companies, Tableau and Veeva, raised only 2. On the other side of the spectrum, New Relic and Workday raised 6.

The 2014 Class of SaaS IPOs show there are many different ways of building a business. New Relic and Zendesk are pure product-driven sales companies. Workday and Hortonworks deliver their products with large amounts of professional services revenue. Veeva and Tableau have demonstrated exceptional capital efficiency. If this data is any indication, and of course setting aside the survivorship bias of this type of analysis, SaaS should remain a very compelling place for founders to build companies and for investors to invest.