2 minute read / Jun 27, 2014 /

The Insularity of Silicon Valley

Earlier this week, the Commerce Department announced US GDP in Q1 2014 fell by 3%, the most in a quarter since the recession. I’ve linked to the WSJ’s chart depicting the trend above. The decline was 3x greater than forecasted. Silicon Valley seems unfazed.

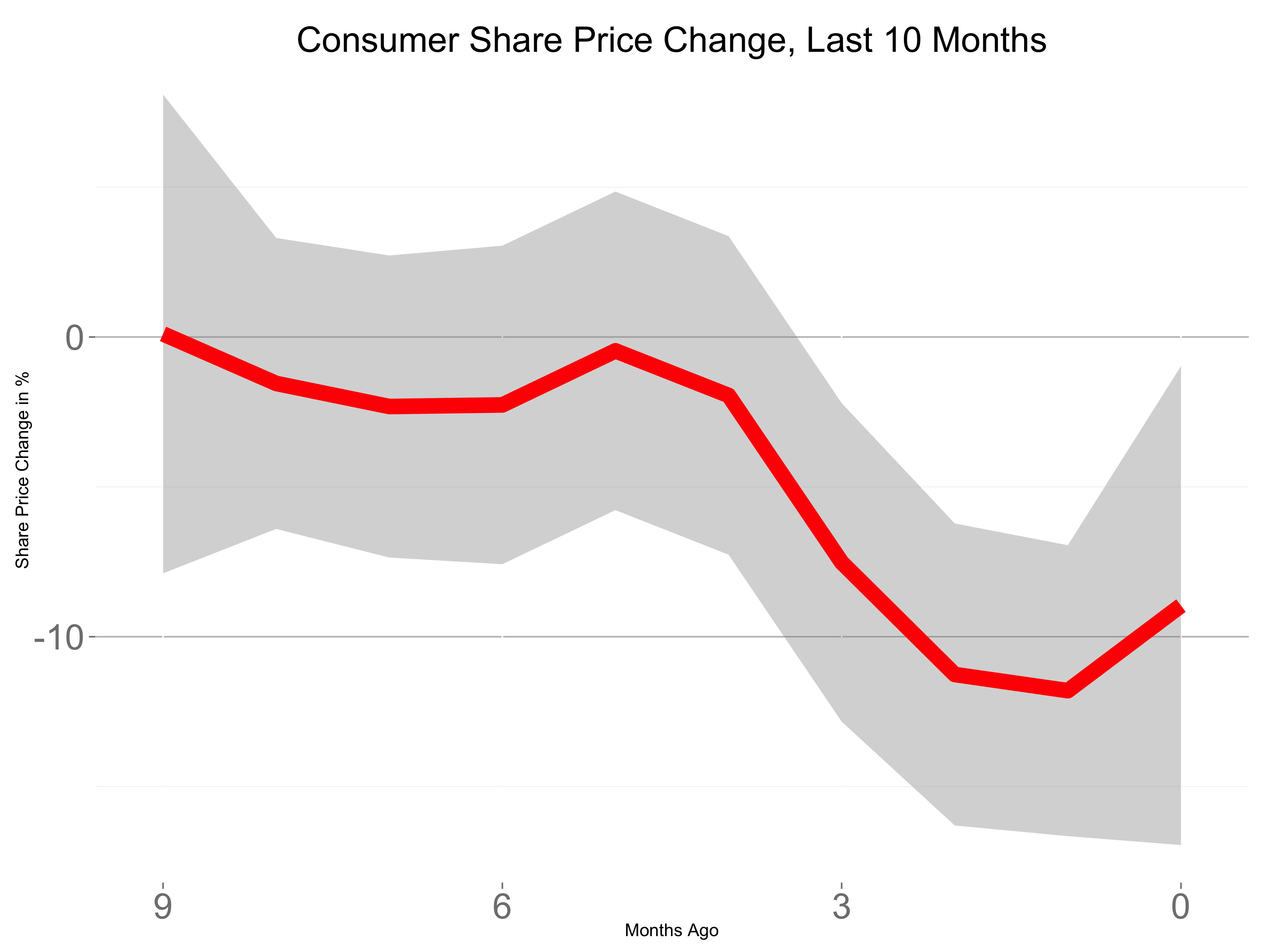

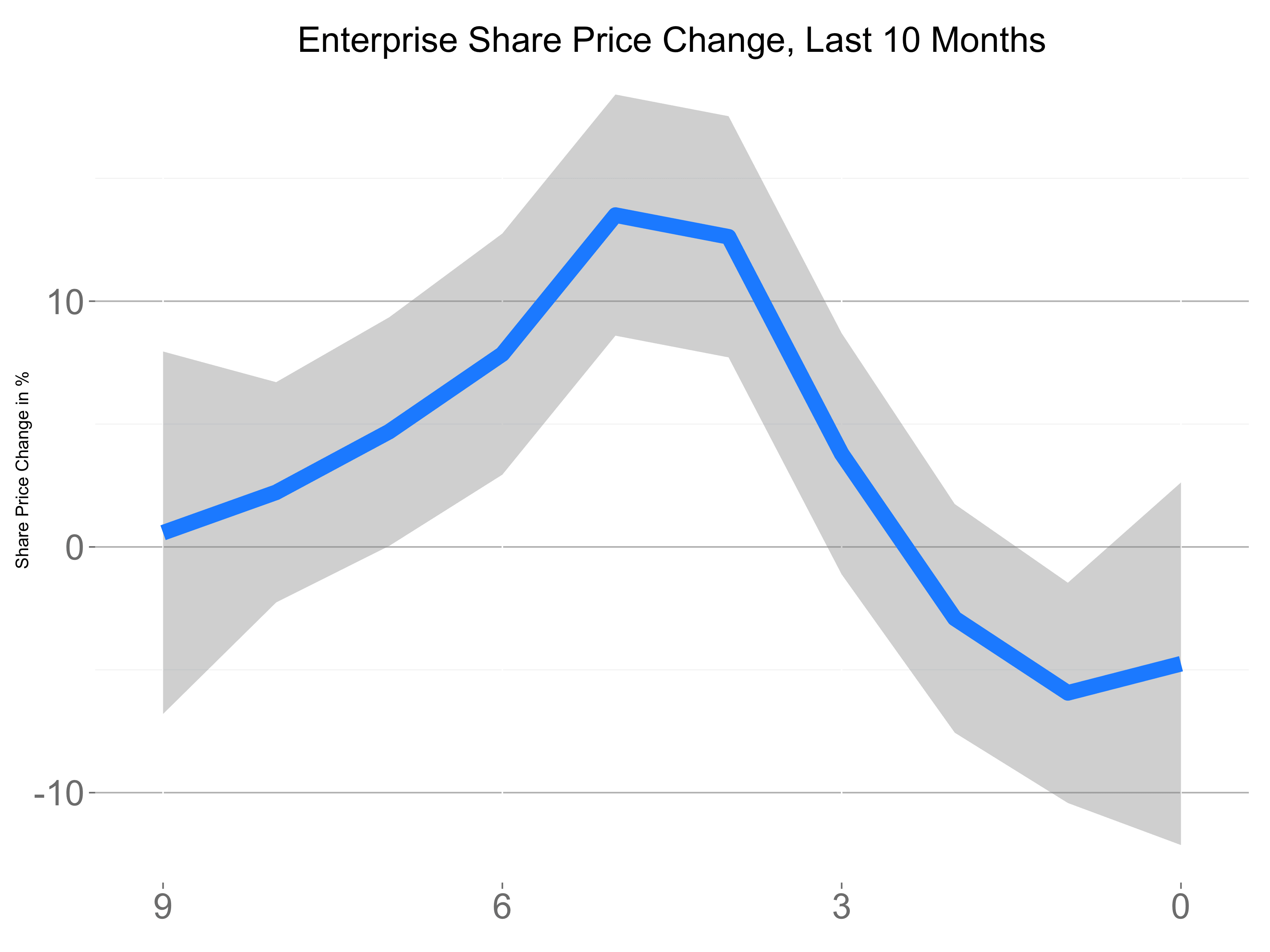

As I wrote about earlier this year, we’ve seen a decline in the public markets of about 25% in consumer stocks and 45% in enterprise stocks. But since that time, public tech companies have witnessed a small recovery. Both enterprise and consumer companies are up 18% from their 10 month lows.

Below are two charts showing the “average” consumer and enterprise tech company’s share price progressing over time, compared to their share price 10 months ago. A value of zero means the stock is at the same price as ten months ago. A value of 10 means the stock is 10% higher than 10 months ago.

Consumer has been impacted a bit more than enterprise but on the whole, both categories of companies are increasing in value again, despite the broader economic challenges in Q1. And forward revenue to enterprise value multiples are on the rise again. As of today, the mean next-twelve months to enterprise value multiple is 7.5, up from 5.5 in May.

The businesses created in Startupland are real companies, generating meaningful revenue, growing quickly and changing industries. Despite large institutional investors cycling out of growth stocks and into value stocks, which caused the April decline in many names, tech is booming and as a result, seems to be insulated from the broader economy.

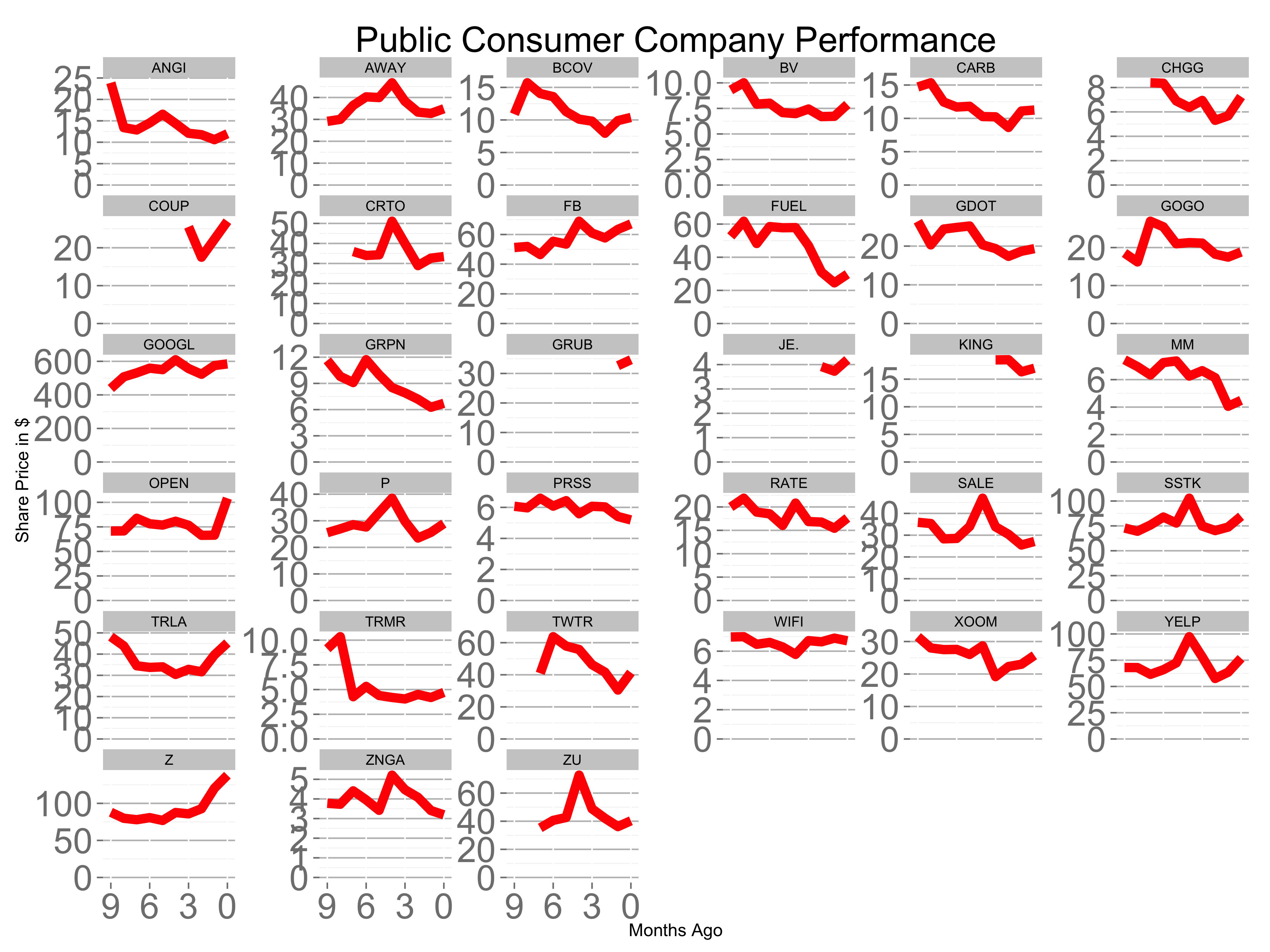

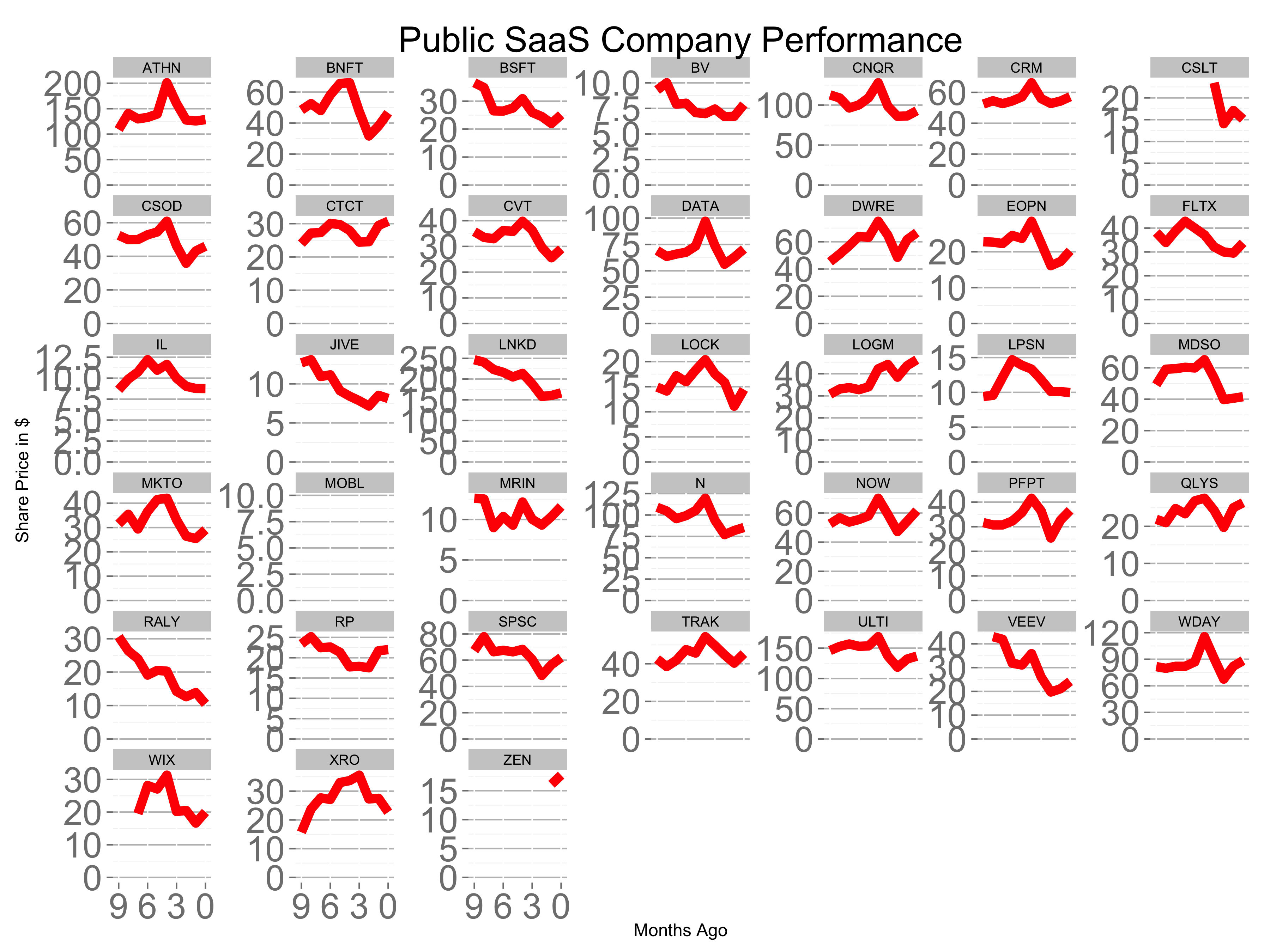

If you’re curious about the movements of individual names over the past tens months, the share prices for the roughly 50 companies across both baskets are below.