This weekend, Janet Yellen said the US economy would benefit from an increase in interest rates. The Fed has been struggling to combat historically low inflation. The combination of both the 25% increase in the money supply from last year’s stimulus plus the proposed infrastructure spending should trigger inflationary pressures. What does it mean for venture capital and Startupland?

In short, we should expect some cooling.

Let’s examine the relationship between total venture capital investment and the 10 year Treasury in some detail. The x-axis plots yield of the 10 year Treasury (average for the year). The y-axis tracks enture capital investment by year and the year of the data point resides in the reddish circle.

Our story starts in the bottom right of corner in the year 2000 with 6% interest rates and $18.2b of VC. Over time, rates decline and then in the 2012-2014 era, they begin to surge upward culminating 6-8 years later at the top-left of the chart and $200b+ invested.

Do you remember this shape from high school math? It’s a rectangular hyperbola and it suggests a relationship of y = A/x^n, which is exactly the net present value formula’s form.

In other words, the market is acting according to theory. As the interest rate approaches zero, venture capital spend approaches infinity. Given the pace of investment and valuations in Startupland, it sure feels like there’s infinite capital in the market.

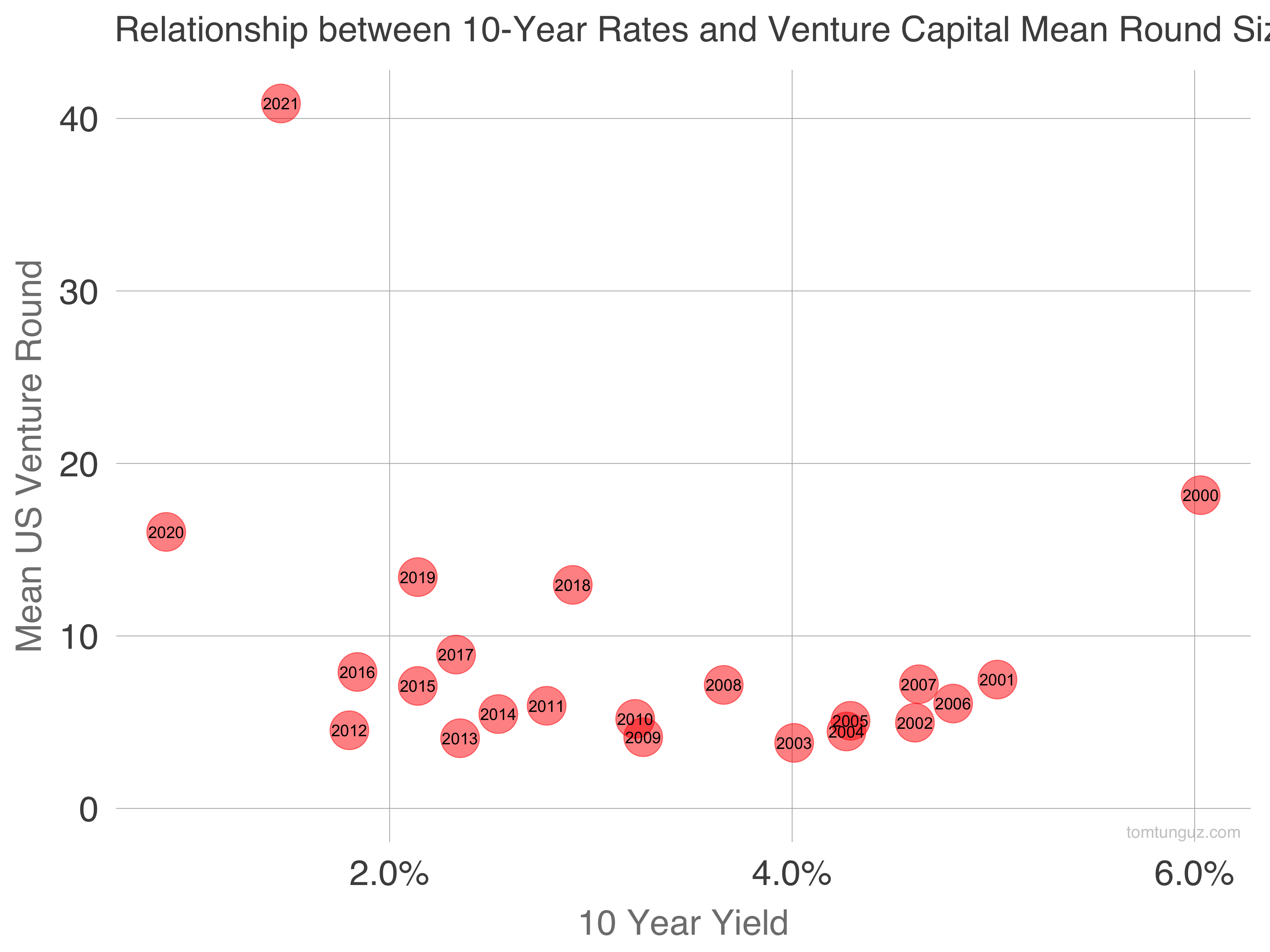

Mean round sizes and deal counts when plotted against the 10 year yield also reveal rectangular hyperbolas.

{kind=link}

{kind=link}

This phenomenon isn’t limited to venture capital; PE demonstrates the same rectangular hyperbola, but the PE chart is smoother, implying the market responds more quickly to changes in rates than venture capital.

Here’s the bottom line: as interest rates increase, we should expect venture capital investment to regress. When the cost of capital is low and yields on cash are small, investors seek greater risk to attain a return. As the risk-free rate on Treasuries increases, market forces should engender enough friction to pull venture investment from the stratosphere into the troposphere or below.

The next question on our lips ought to be: how quickly will the friction appear? There are arguments on both hands. For a speedier correction: the recent volatility of the public technology markets, the presence of public investors in private markets, the fact that relationship between rates/risk is well-known amongst investors.

On the other hand, venture markets have always been slow to respond to public markets, the charts above show quite a few years of latency between a fall in rates and an increase in spend, and venture funds are raised to be invested over years; all of which should mute some of the impact.

If you’re looking for one-handed economist like an exasperated President Truman, I’ll give you my view. I suspect the correction influenced by rates takes a few years to percolate through Startupland. As rates increase, the tide of venture dollars will inexorably ebb.

PE’s relationship with rates seems more straightforward, and this makes sense given the LBO (leveraged buy-out) requires significant debt. Bond yields govern the price of loans, so the impact of higher rates on PE costs/returns is direct and immediate.

This is why all investors’ eyes are trained on inflation and Treasury yields. These numbers move markets.