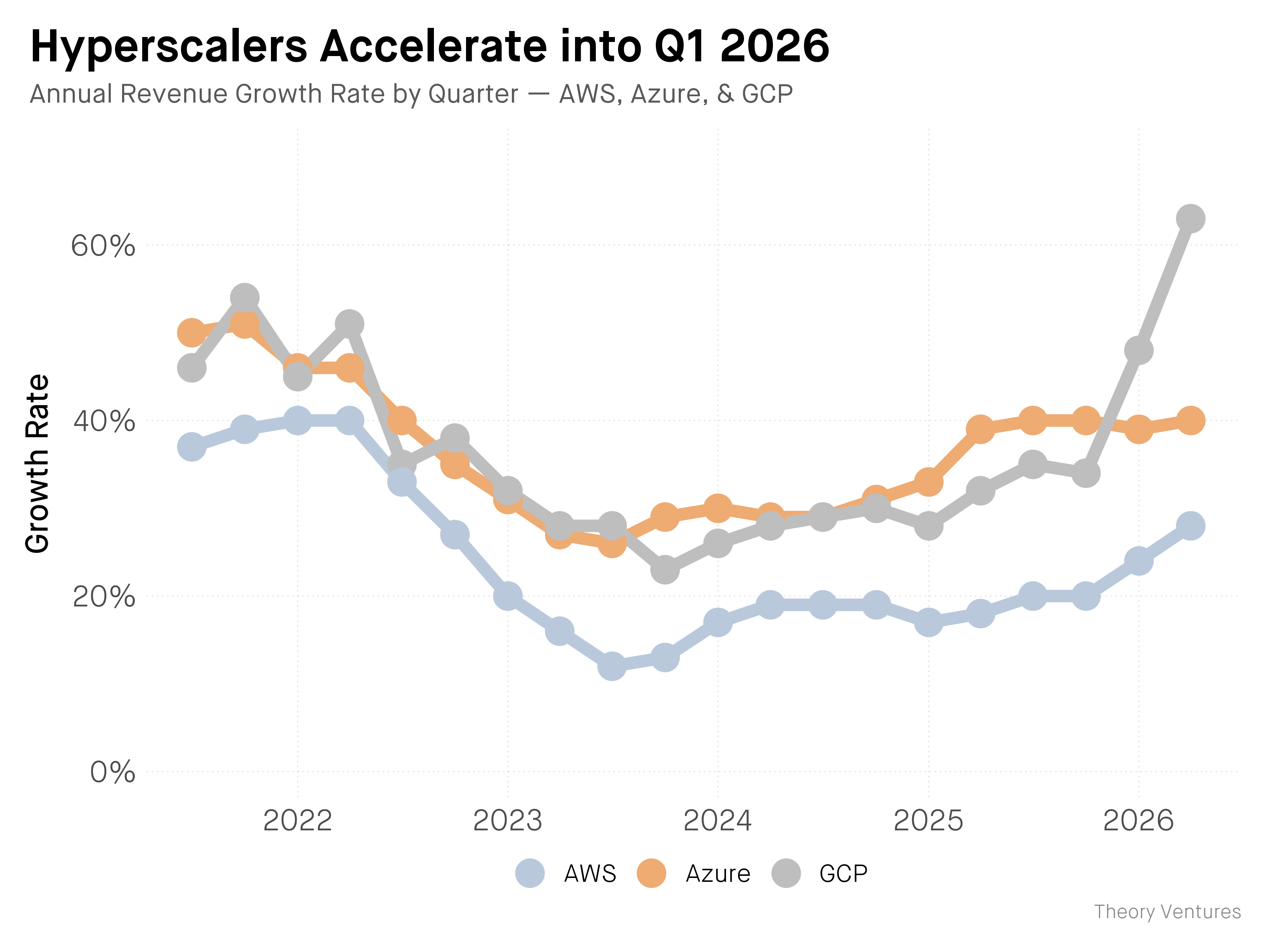

Google Cloud grew 63% year-over-year in Q1 2026. Amazon Web Services posted 28%. Microsoft Azure hit 40%. All three are exceptional. Only one hit 63%.

The divergence is striking. AWS & Azure resell compute. Google bundles compute with its own models. Whether that explains the full gap is unclear, but the structural advantage is not : Google owns Gemini & TPUs top to bottom, with no licensing fees to OpenAI or Anthropic. Its growth may be more profitable too.

Sundar Pichai gave the clearest explanation on the earnings call :

“Our enterprise AI solutions have become our primary growth driver for cloud for the first time in Q1.”

Google could not build data centers fast enough to satisfy the AI workloads its customers wanted to run. Pichai confirmed it on the call :

“We are compute constrained in the near term. Our cloud revenue would have been higher if we were able to meet the demand.”

Google Cloud’s backlog nearly doubled quarter-over-quarter to over $460 billion, more than twice its trailing-twelve-month cloud revenue. (By comparison, Microsoft’s commercial RPO of $627 billion includes Office 365, Dynamics & LinkedIn, not just Azure.) Pichai disclosed the scale of enterprise deal flow :

“We are seeing strong deal momentum, doubling the number of $100 million-$1 billion deals year-on-year & signing multiple $1 billion-plus deals.”

These are committed contracts that cannot be fulfilled until new capacity comes online in late 2026 & 2027.

Gemini is now processing 16 billion tokens per minute via direct API use by customers, up 60% from last quarter. Google is not just scaling volume. With vertical integration, it is driving down the marginal cost per token :

“TPU 8i delivers cost-effective, low-latency inference with 80% better performance per dollar than the prior generation.”

The customer scale is staggering :

“330 Google Cloud customers each processed over 1 trillion tokens. 35 reached the 10 trillion token milestone.”

Even at the stated minimums, those 330 customers alone represent a floor of roughly $1.6 billion in annual token consumption. And they are growing into their commitments faster than planned :

“Customers outpaced their initial commitments by 45%, accelerating over last quarter.”

This is consistent with what enterprises like Uber & BlackRock have disclosed : internal AI budgets are eclipsing initial estimates because usage grows exponentially once models are deployed in production.

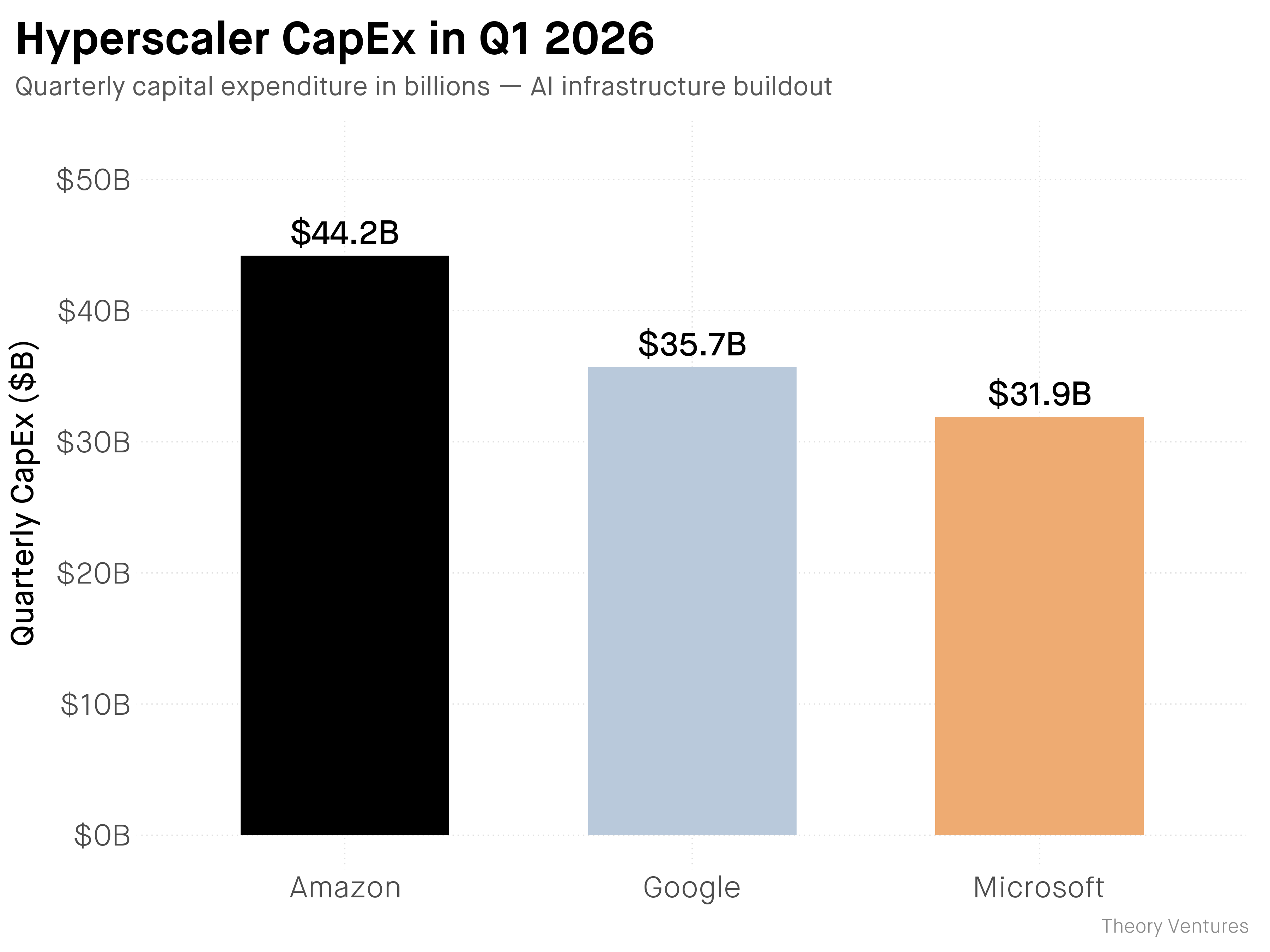

All three hyperscalers reported extraordinary capital expenditure in Q1, a combined $112 billion in quarterly infrastructure spending.

Google is now outspending Microsoft on capex, despite running a cloud business about 37% the size. That gap will widen. Google raised full-year 2026 capex guidance to $180-190 billion, while Microsoft is tracking toward roughly $120 billion. The smaller player is spending more to catch up.

Amazon’s free cash flow collapsed to $1.2 billion as a $59.3 billion year-over-year surge in infrastructure spending consumed nearly all of its $148.5 billion in operating cash flow. Google still generated $64.4 billion in TTM free cash flow. Microsoft produced roughly $15 billion quarterly.

How they’re financing the gap is revealing. Alphabet sold a rare 100-year “century bond,” the first by a tech company since Motorola in 1997, as part of a $32 billion debt offering. Amazon raised roughly $54 billion in March. Bank of America forecasts hyperscaler debt issuance will hit $175 billion in 2026, more than six times the $28 billion annual average of the prior five years.

Microsoft, by contrast, is funding its buildout from operating cash flow. Google & Amazon are levering up to close a gap. Microsoft is already ahead.

But debt isn’t the only way to catch up. Amazon is betting on vertical integration. It landed 2.1 million AI chips over the past twelve months & its chips business has crossed a $20 billion annual revenue run rate, growing triple-digit percentages year-over-year. OpenAI committed to consume approximately 2 gigawatts of Trainium capacity through AWS starting in 2027. Anthropic secured up to 5 gigawatts.

But Amazon doesn’t own the model layer. Google does.

The hyperscaler that owns the model layer is growing the fastest.