2 minute read / May 17, 2024 /

AI Spending Patterns : It's Not What You Think

Ramp published its quarterly spending trends & revealed how businesses are spending on AI. There are many great data points that underscore the growth in AI but there are important nuances in the patterns.

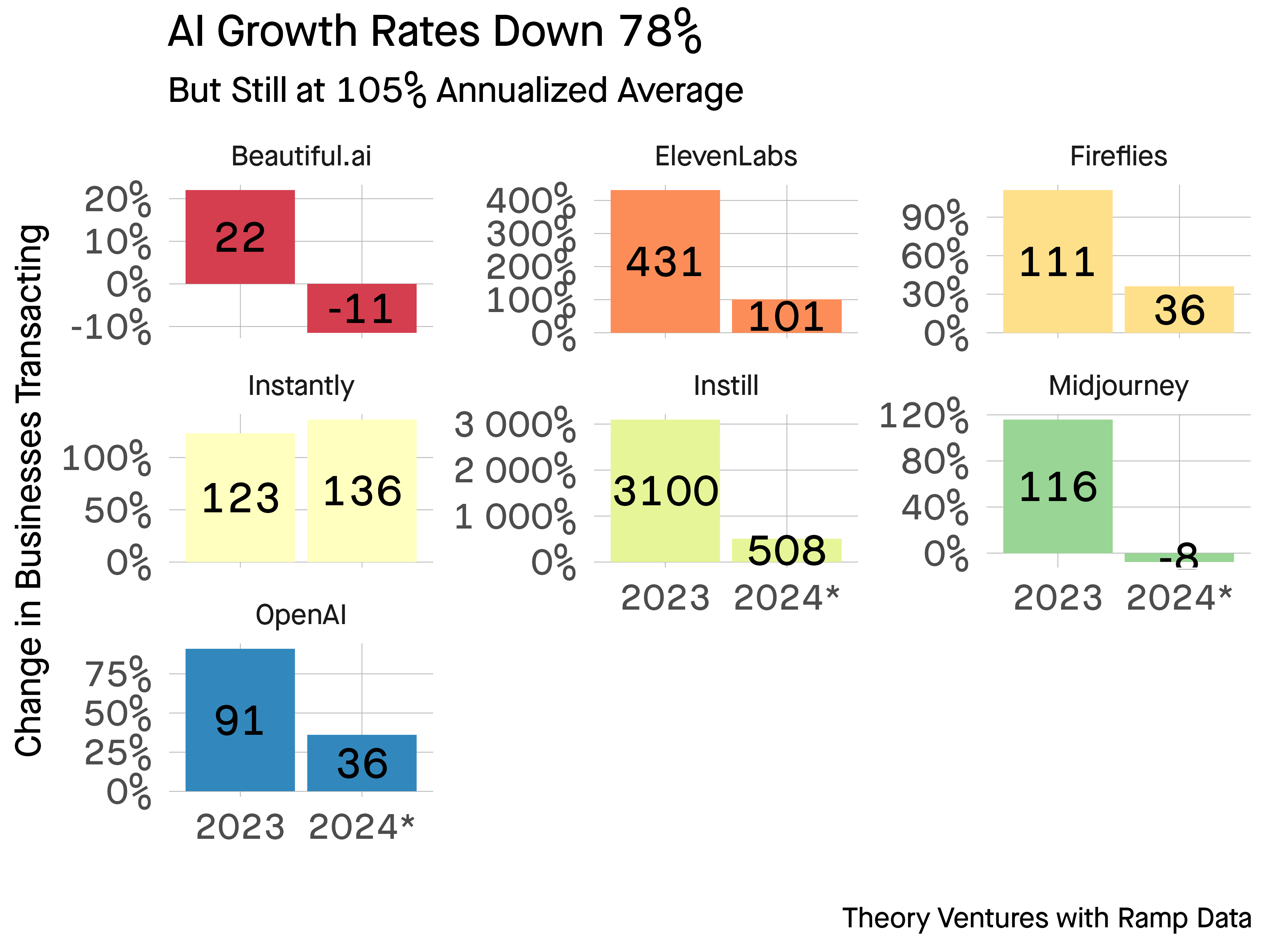

First, AI growth rates across the most popular vendors have fallen 78% annually. On average, these AI businesses are growing customer counts 105% ; the median is 38%.1

However, this isn’t a uniform trend. Some companies have seen contraction in customer counts. Both the companies with negative account retention still see relatively minor account churn : 15-25% account churn at these price points is common.

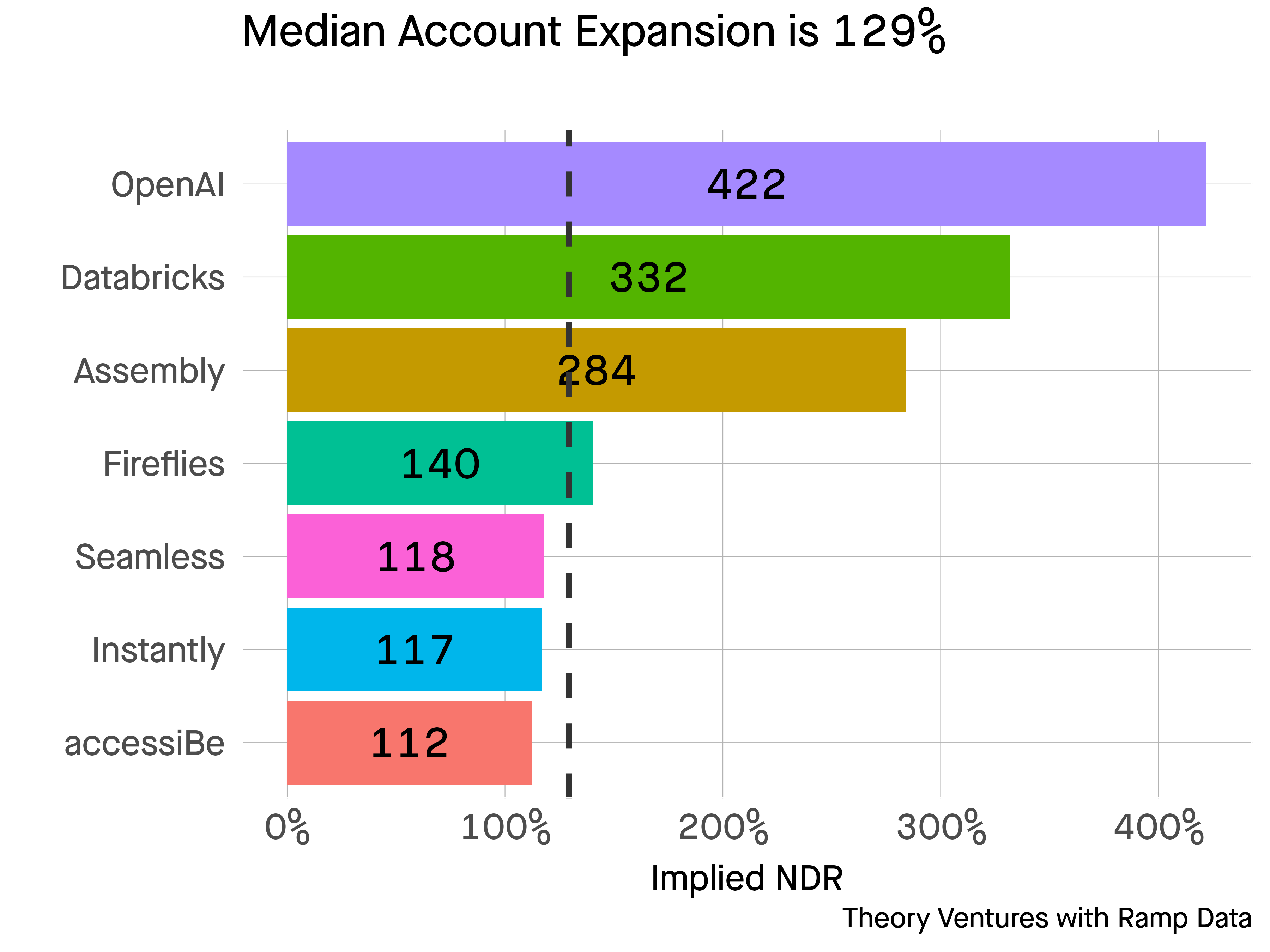

Second, the account expansion remains relatively strong. The top quartile software companies around 125% today & the companies above are very similar with a median of 129% net dollar retention (NDR).

Second, the account expansion remains relatively strong. The top quartile software companies around 125% today & the companies above are very similar with a median of 129% net dollar retention (NDR).

These data points suggest that AI infused software companies’ metrics will asymptote to overall software metrics in time. NDR is almost equal. Growth rates remain very strong, but perhaps are seeing some attenuation.

In some categories, revenue growth is more challenged which highlights a challenge in very fast growing markets : quality of revenue.

The underlying technology shifting rapidly - the announcements from Google & OpenAI this week underscore the point; buyer preferences are evolving rapidly as they start to understand the relevant applications of the technology, the costs of deployment & the value gained from different applications ; vendor pricing dynamics also play a role. OpenAI reduced prices by 50% this week driving deflation in the market.

The additional data within the report underscores AI’s growth in the last year.

“Card transaction volume for AI software services jumped 293% year-over-year compared to an increase of just 6% in overall software transaction volume during the same period.”

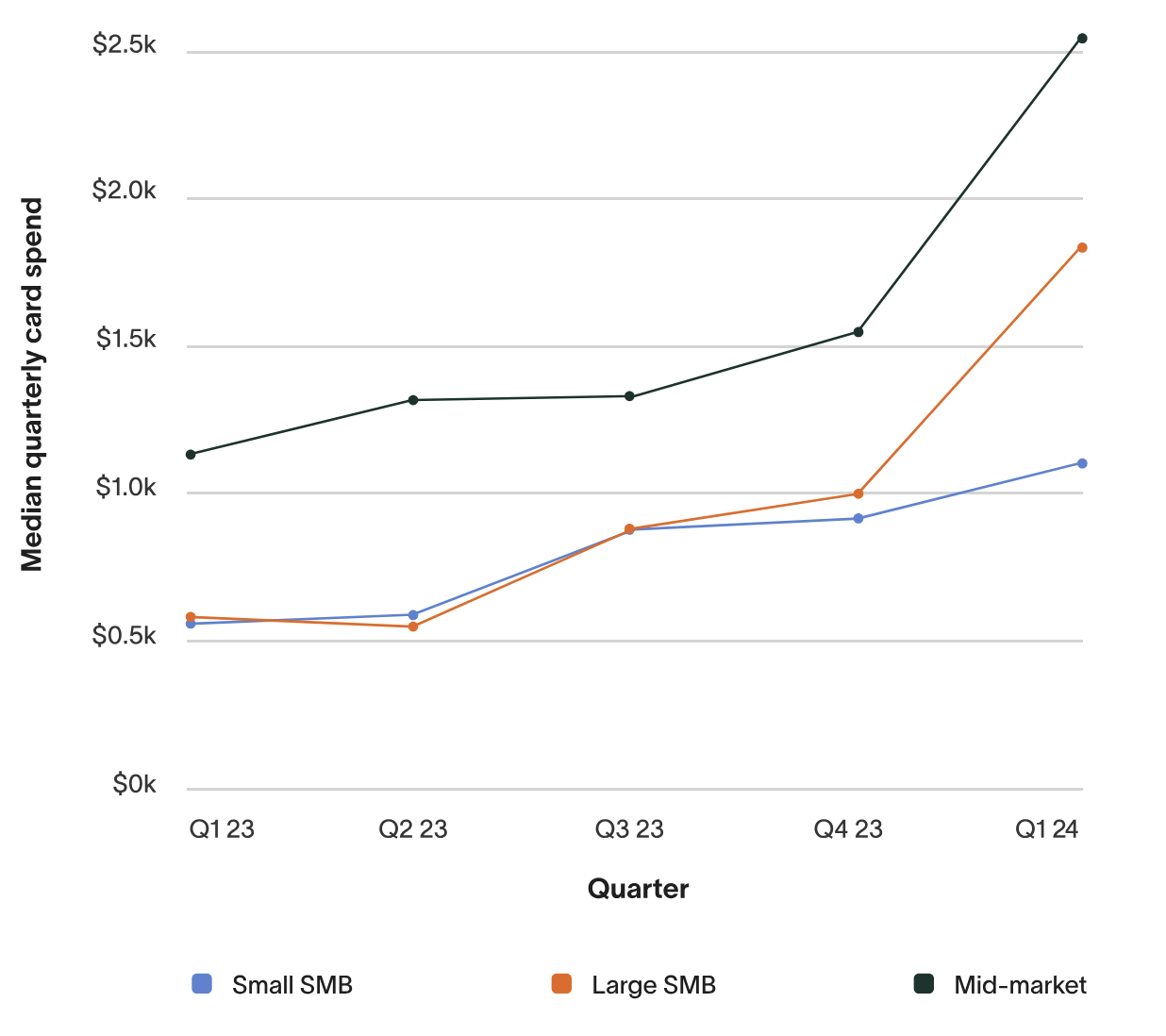

This growth is true across company size.

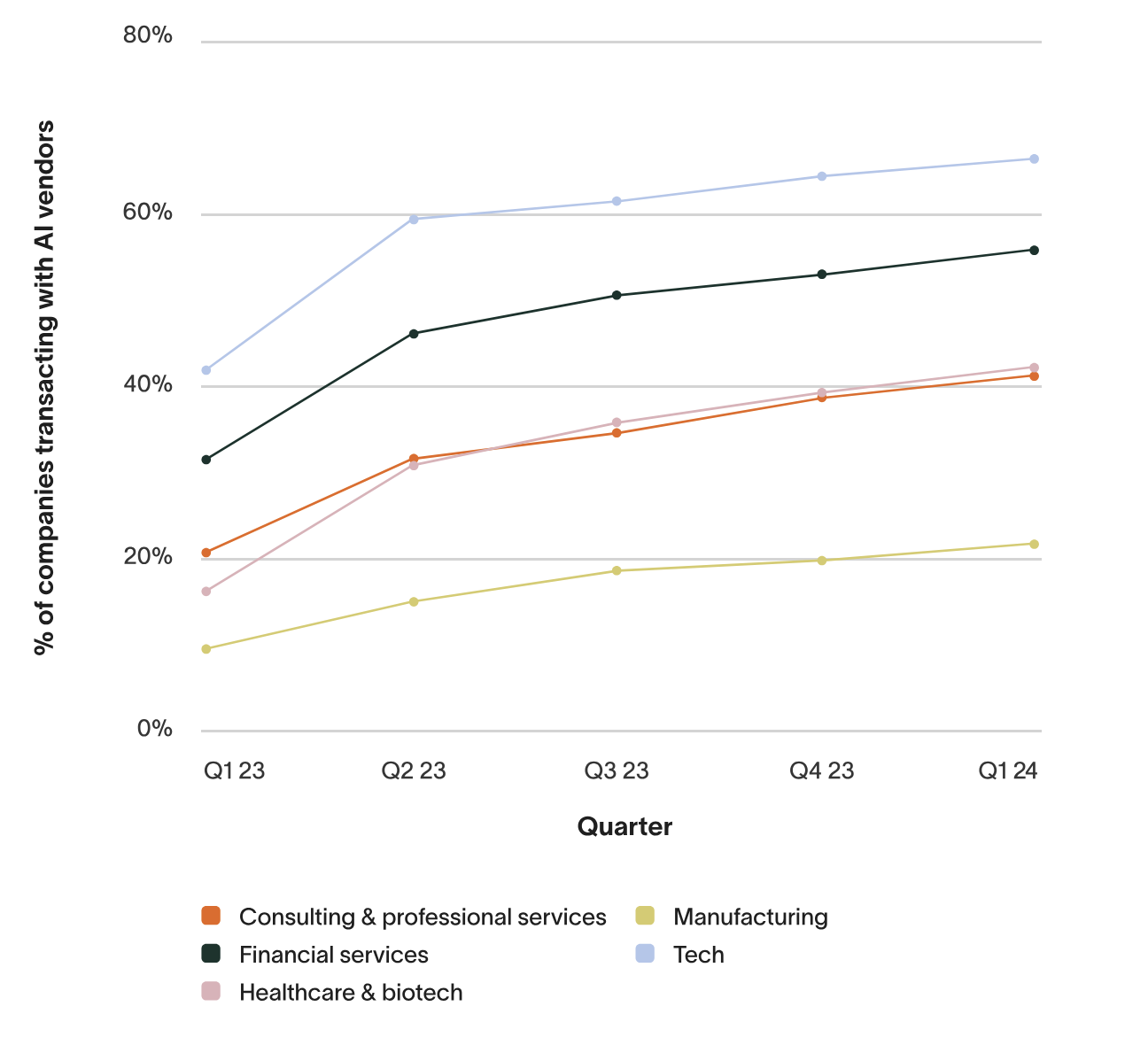

& across most industries.

There’s still quite a lot to be excited about. & there are signs to be more sanguine about long-term growth rates & valuations approaching those of overall high-growth software companies.

It’s also important to note that this spending data is just credit cards. For many of these companies whose larger accounts pay via purchase order, the patterns may be quite different.

1 I’m annualizing the Q1 changes to impute the 2024 estimated change.