At Redpoint’s annual investor meeting earlier this year, I quipped, “The day-trading taxi drivers of the dotcom era have been replaced by crypto-trading Uber drivers.” But over the weekend, a grizzled Uber driver with a mane of grey hair and wind-and-sunburnt cheeks asked me about crypto. “Can you explain to me why public key/private key technology is important on the Blockchain?” He pointed out the Bitcoin ATM that charges 10% from his cigarette-infused Prius. “That’s for suckers; Coinbase charges only 2%,” he said as we whizzed past.

A former yacht broker and pilot, he likened crypto to Powerball. “I can put in a few bucks, buy some Dogecoin or Jesuscoin, and maybe it goes up 100x overnight and I’ve changed my life. I like Monero, too.”

A few hours later, as I boarded the plane home, I read Fred Wilson’s post on Buffett and Munger’s critique of cryptocurrency investing. Buffett and Munger argue that buying crypto isn’t investing but speculating.

You aren’t investing when you do [buy crypto]. You’re speculating. There’s nothing wrong with it. If you wanna gamble somebody else will come along and pay more money tomorrow, that’s one kind of game. That is not investing.

Buffett and Munger aren’t technology investors. They said as much on page 6 of Berkshire’s 2007 shareholder letter. They look to invest in “enduring businesses.”

Our criterion of “enduring” causes us to rule out companies in industries prone to rapid and continuous change. Though capitalism’s “creative destruction” is highly beneficial for society, it precludes investment certainty…A truly great business must have an enduring “moat” that protects excellent returns on invested capital

The letter highlights See’s Candy, a West Coast chocolate maker Buffett bought decades ago for $25M. Since its purchase, See’s generated $1.4B in cash for Berkshire, and required only $32M in incremental investment. A 24x return in 30 years. The company has built a moat with its strong brand.

As the plane reached 10,000 feet and I pulled out my laptop, I read about last week’s Tesla earning call. An analyst asked Musk a question about Buffett’s view on moats.

I think moats are lame. They are like nice in a sort of quaint, vestigial way. If your only defense against invading armies is a moat, you will not last long. What matters is the pace of innovation, that is the fundamental determinant of competitiveness.

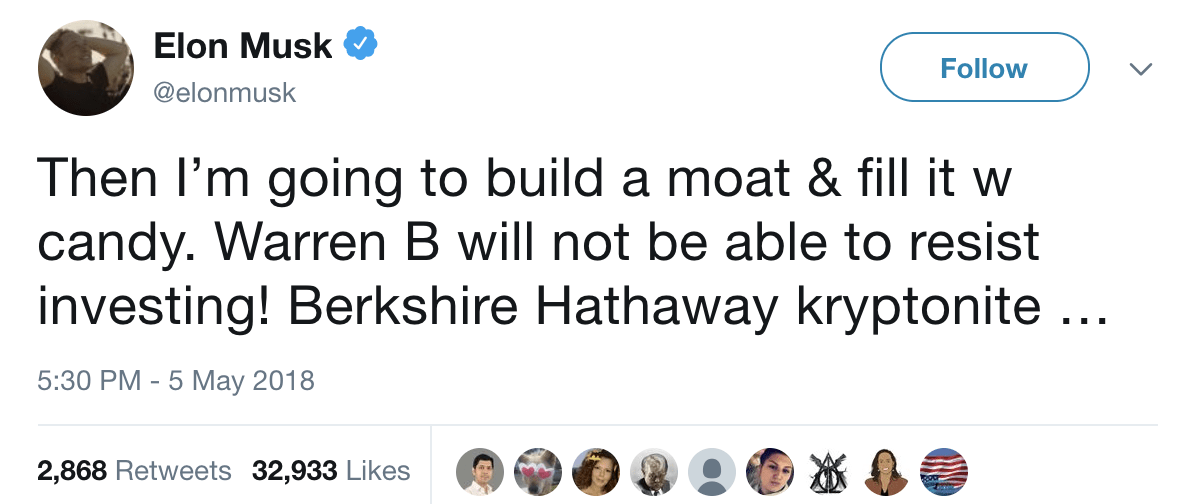

Buffett and Munger got wind of Musk’s critiques. The three bounced barbs through the press over the next few days, with Musk finally retorting:

Loeb, Musk and Wilson share one world view. Buffett and Munger hold the opposite point of view. The speculators believe great investments develop competitive advantage through innovation, disruption and displacement. The investors advocate competitive advantage prevents disruption and displacement. Both camps have proven their theories correct and generated billions of returns for their investors.

Of course, I favor the speculator’s point of view. In the Zurich Axioms, a book written by an American journalist educated at Princeton named Max Gunther. He quoted Gerald Loeb, author of one of my favorite investment books called The Battle for Investment Survival.

“All investment is speculation. The only difference is that some people admit it and some don’t.”

Irrespective of your point of view, the crucial lesson in all this - whether you’re a venture capitalist, crypto-buying Uber driver, or billionaire private equity buyer - stick to your strategy. The VCs and founders play an offense-only game. They speculate and bet on disruption to win. On the other side of the coin, Munger and Buffett play defense; maintain the status quo and milk the profits. To mix them would result in defeat - and a lot of soggy candy.