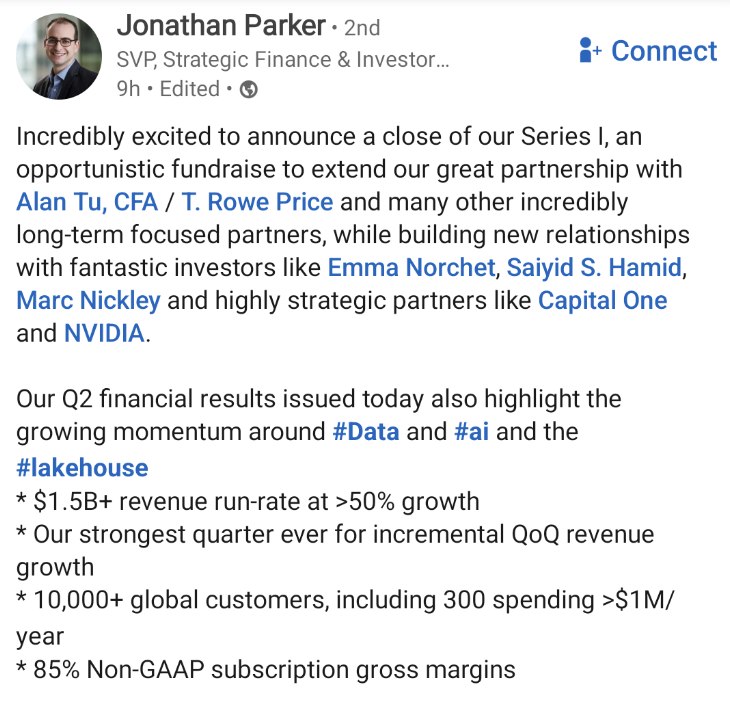

Last week, Databricks announced their Series I financing at $43b. At the same time, they released quarterly figures similar to a public company’s reporting.

Those numbers provide the first public view into one of the most valuable private companies in the world. It’s also an opportunity to compare Databricks to Snowflake.

Two mammoths competing for customers’ workloads offer different architectures. Snowflake’s cloud analytics database thrives on structured data. Databricks’ technology rips through unstructured data in a cloud data lake house.

Choosing Snowflake’s closest historical quarter by revenue provides a side-by-side comparison of their financial profiles.

| Metric | Snowflake | Databricks |

|---|---|---|

| Calendar Quarter | Q2 22 | Q3 23 |

| Revenue, $m | 388 | 375 |

| Revenue Growth, y/y, % | 85% | 51% |

| Product Gross Margin | 72% | 85% |

| Customers | 6,333 | 10,000 |

| $1m+ Customers | 206 | 300 |

| Implied ACV, $k | 61.3 | 37.5 |

In Q2 2022, Snowflake generated roughly the same amount of revenue. Snowflake was growing at 85% y/y compared to 51% for Databricks.

Notably, the macroeconomic environments couldn’t have differed more. The Fed Funds rate in 22 was at 0.33%. Today, it’s 5.5%. So Databricks is sustaining top decile growth despite stiffer headwinds.

Databricks’ product gross margins, which exclude any professional services work, top Snowflake’s by more than 10 points. Both companies run their workloads on the cloud.

Sometimes, Databricks doesn’t incur infrastructure costs when customers run the workloads in their own accounts (called cloud-prem), the business enjoys higher gross margins. If more Databricks customers move to the fully managed services, these figures may converge.

Databricks counts almost 50% more customers than Snowflake at the same time, & nearly 50% more $1m+ customers.

A different distribution characterizes Databricks’ customer base. Databricks tallies more large accounts & more small accounts. This explains Snowflake’s $61k ACVs compared to Databricks’ $37.5k , while Databricks has a greater number of million-dollar-plus contracts.

Soon, we’ll be equipped to compare longitudinal trends & one day relative efficiency.

For now, Databricks’ growth, despite the environment, fueled by the demand for AI is a promising sign for startups. Plenty of demand exists to buy innovative data infrastructure.