There’s a theory to the idea that winner takes most in Startupland. The startup that grows a bit faster at the beginning demonstrates more momentum. The startup raises capital sooner, hires people, builds the product, markets and sells the product, grows more, and raises capital. Repeat the process for each round of capital. Is it borne out in reality?

This theory suggests that irrespective of the category, the winner should capture most of the market value. Reality is far more complicated than this simple idea. After all, most startups face turbulence in their journey. Venture capitalists finance competitors to pursue a market opportunity. M&A environments ebb and flow. Undisclosed private sales or private valuations aren’t considered. Plus, survivorship bias plagues this analysis.

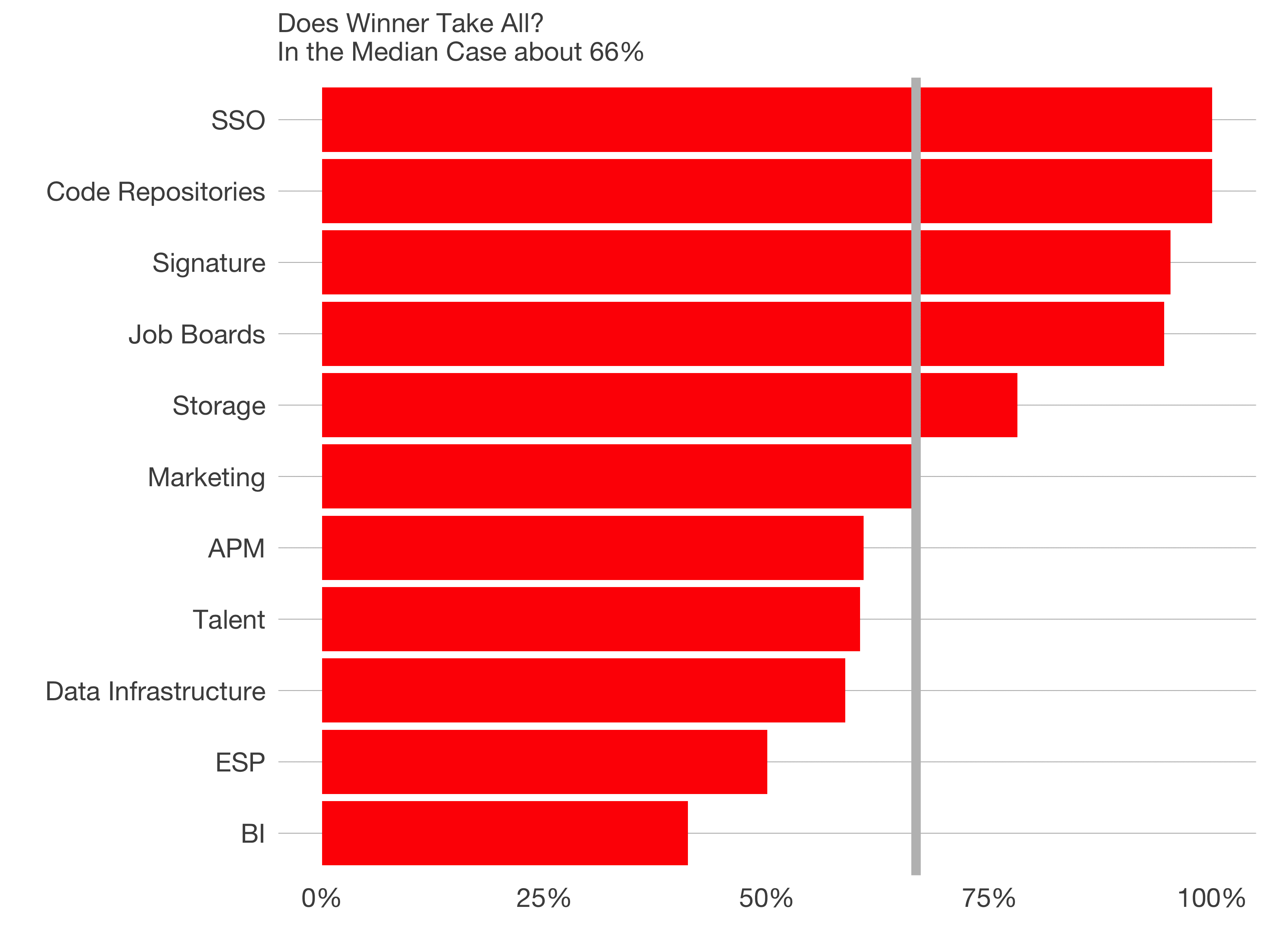

Setting all of that aside, I put together a basic data set across different software sectors. I examined 11 sectors which benefited from meaningful exit activity over the last 15 years. From email service providers (ESP) to application performance management (APM), I catalogued the companies who had sold or were public, and their values at time of exit or today’s market cap. Then I calculated the share of winnings per category. The analysis is far from perfect. It’s meant to be directional.

We can draw a few initial observations. First, there’s quite a bit of variance in the winner’s share by sector. At the top end, Okta and Github have dominated the market for single sign on and code repositories. They define their categories.

One could argue Atlassian belongs in the code repositories bucket. And that’s a good point, but it raises another complication to this type of analysis. How to divide Atlassian’s $15B market capitalization into the Bitbucket market cap and non-Bitbucket market cap? Atlassian’s public disclosures don’t break this out.

At the bottom of the list, the last wave of Business Intelligence (BI) saw 4 companies with an aggregate exit market cap of about $16B. The largest, BusinessObjects, captured 41% of the exit value.

Second, the median winner’s stake across categories is about two thirds. This is “consistent” with the theory, that the winner takes most. Second place takes home around 20-30% of exit market cap.

Third, it’s critical to play to win as a startup, and why being first matters so much. Dominating a market means somewhere between 50-100% of the exit market cap, an exit price 2-3x second place.

This analysis isn’t exhaustive, but as a directional guide, it provides some supporting evidence that even in categories where classic network effects, data network effects or other economies of scale don’t dominate the competitive dynamics, the winner does take most in software.