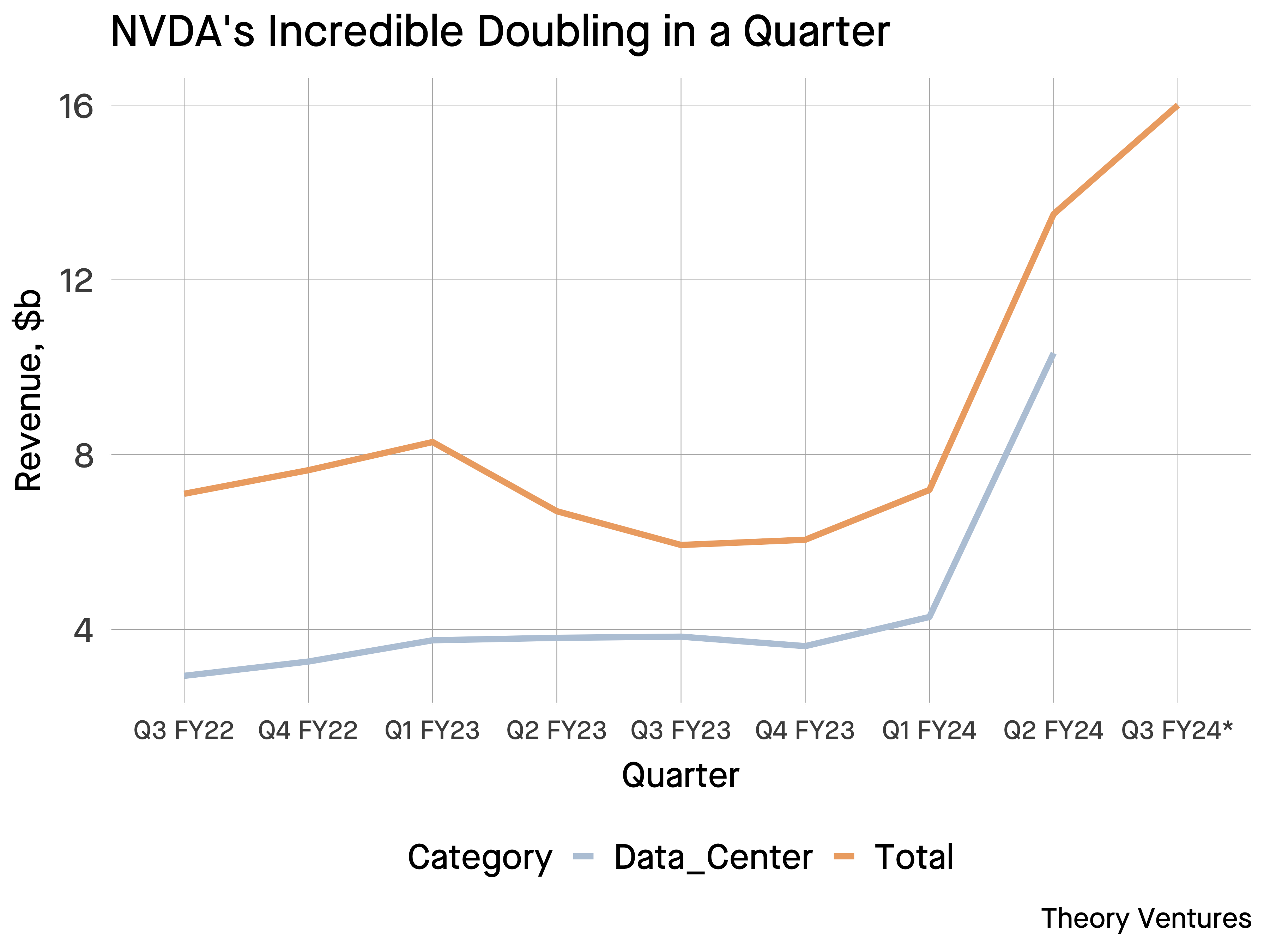

If we needed another exclamation point on the tremendous growth opportunity, NVidia’s earnings punctuated the euphoria with gusto.

Revenue grew 88% in a quarter, nearly doubling. The company had projected $11b & exceeded projections by $2.5b or 26%.

The Data Center business, which sells to clouds & consumer companies drove nearly all of the growth, surging 141% quarter-over-quarter to $10.3b & nearly 3x annually.

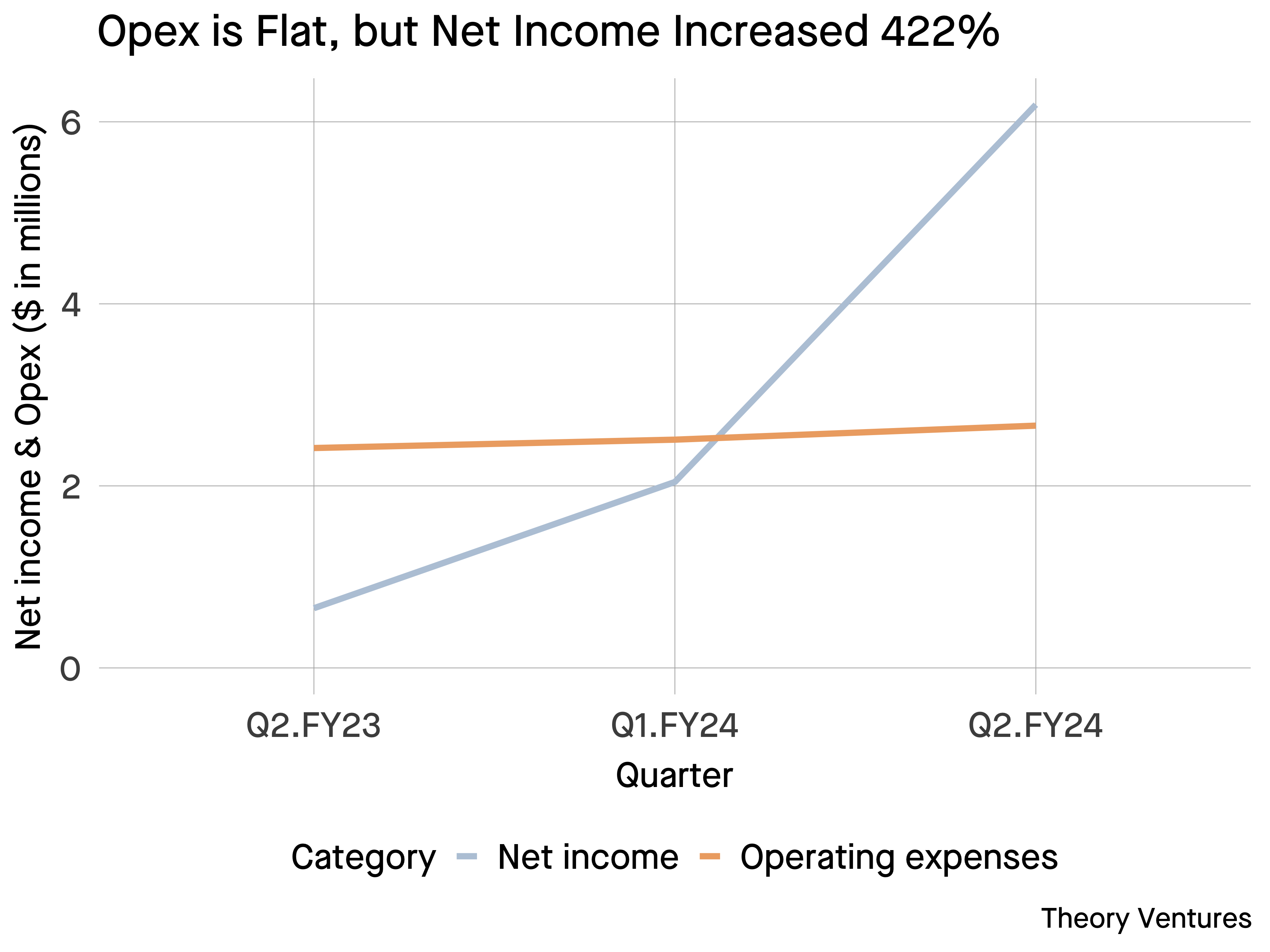

NVDA’s profitability is remarkable. Over the last year, the company’s operating costs haven’t increased more than 15% yet, net income (profit) has quadrupled. The company’s pricing power at work : limited supply & increased demand pushes prices higher.

China demand remained within the historical range of 20%-25% of Data Center revenue, implying the export regulations imposed on chips doesn’t seem to have impacted the company.

Looking at some of the inventory metrics (this isn’t a software company!), inventory is relatively flat, but DSI (Days Sales Inventory - the number of days required to sell all existing inventory) has fallen 41% ; another sign of unmet demand.

Long term supply obligations (pre-purchasing of materials/inventory) has increased 53%, another sign of customers yelling for more GPUs. Accounts receivable - which is the amount customers owe NVidia for purchased goods but yet haven’t paid - increased more than 70%.

| Metric | Q1 | Q2 |

|---|---|---|

| Inventory, $b | 4.6 | 4.3 |

| DSI | 165 | 97 |

| Long term supply obligations, $b | 7.3 | 11.2 |

| Accounts receivable, $b | 4.1 | 7.1 |

Jensen Huang, the company’s CEO, estimated worldwide data centers are worth $1t with $250b spent on new chips each year. At the current run rate, that implies NVidia is capturing about 22% of that market.

AI has become the engine pushing the technology markets forward - both at the infrastructure & software levels.