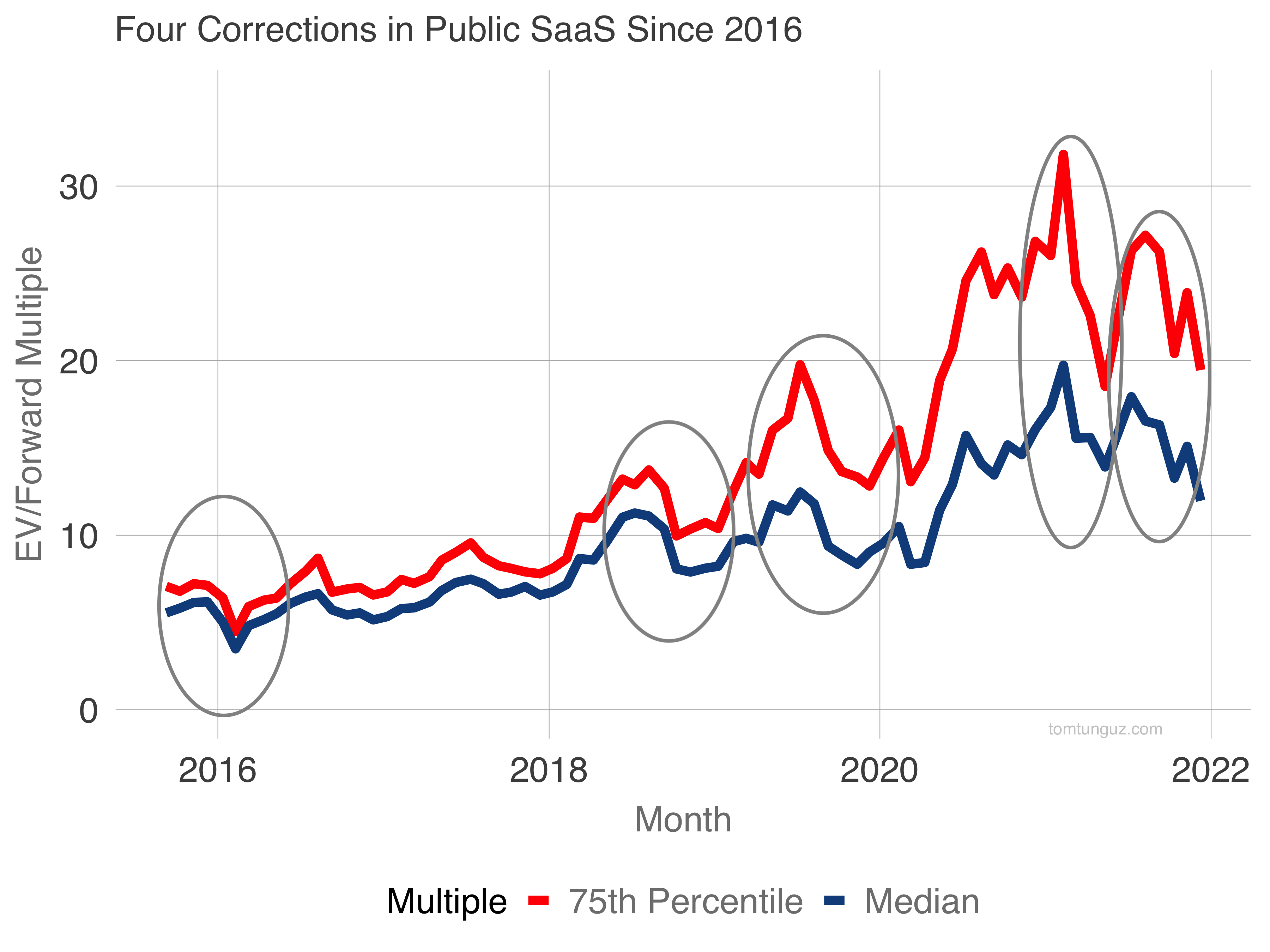

Since 2016, public software has witnessed four corrections. Today, we’re in the midst of the fifth. Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. But let’s look at the most recent five years.

This chart shows the median and the 75th percentile of enterprise value/forward revenue multiple for the basket of public stocks which were public at that moment in time.

| Correction Year | Max | Min | % Change |

|---|---|---|---|

| 2014 | 7.7 | 3.3 | -57% |

| 2016 | 7.2 | 4.5 | -37% |

| 2018 | 13.7 | 10.0 | -27% |

| 2019 | 19.8 | 12.8 | -35% |

| 2020 | 31.8 | 18.5 | -41% |

| 2021 | 27.2 | 19.5 | -28% |

These corrections reduced valuations by between 30% and 60%. These undulations are short-lived. The market recorded new highs often within four to six quarters after the nadir. The net result is multiples have charted a volatile course with a positive slope. What a growth investor ought to expect.

In fact, the 75th percentile multiple has appreciated 25% annually since 2016 and the median has increased by approximately 20%. Cloud companies’ fast growth multiplied by an appreciation in multiples has pushed valuations higher since 2014.

How does this map to the private market? Till 2020, the growth rates of the private market valuations and the public valuation multiples paralleled each other at the highest level. However, the private markets remained steadfast in their valuation methodologies, irrespective of the volatility in the public markets,

How does this map to the private market? Till 2020, the growth rates of the private market valuations and the public valuation multiples paralleled each other at the highest level. However, the private markets remained steadfast in their valuation methodologies, irrespective of the volatility in the public markets,

2021 changed all that - no fancy analysis needed! The hockey stick is a discontinuous event. Perhaps investors have been undervaluing companies for the last two decades. Or perhaps we’ll see some reversion to the mean. When is anyone’s guess.

Reading these data, the natural question is what is an accurate forward multiple for a company? The answer is it depends on an investors’ holding period and the company’s financials and prospects.

Historically, public market valuations haven’t impacted private markets. But perhaps, this time is different. If so, the unique difference has more to do with the recent discontinuous behavior of the private markets than the public markets.