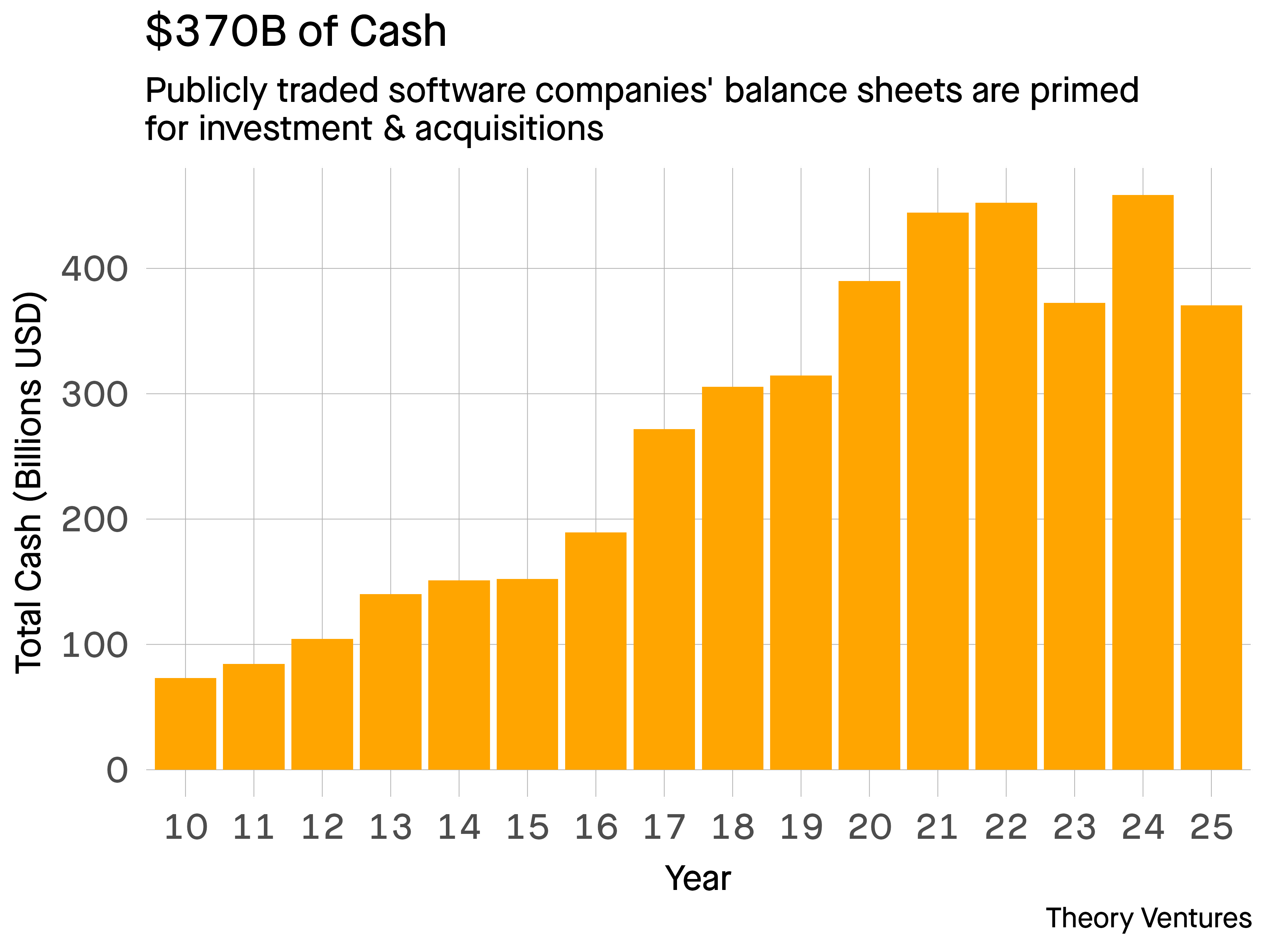

Despite holding a staggering $370b war chest in 2025, tech giants aren’t racing to acquire companies – they’re too busy building their AI empires, one data center at a time.

Microsoft hasn’t acquired a company since January 2023. Two of Google’s reported acquisition overtures, Wiz & Hubspot, were scuttled.

This focus elsewhere creates an opportunity for mid-market players to lead the M&A wave of 2025.

As of January 2nd, these major acquirers hold $370b in cash & short-term equivalents. These levels represent near-historic highs over the past 15 years.1

Notice in 2025 the overall cash balance dropped by $80b. Google, Microsoft, & Meta are collectively on a $200b annual capex runrate on data center expansion.2 Nvidia also spent $11b repurchasing shares.

Notice in 2025 the overall cash balance dropped by $80b. Google, Microsoft, & Meta are collectively on a $200b annual capex runrate on data center expansion.2 Nvidia also spent $11b repurchasing shares.

These record-breaking infrastructure investments dominate quarterly earnings calls. With their focus on securing competitive advantages through GPUs & power plants, major acquirers may modulate their M&A activity. For hyperscalers, today’s competitive dynamics revolves around compute capacity.

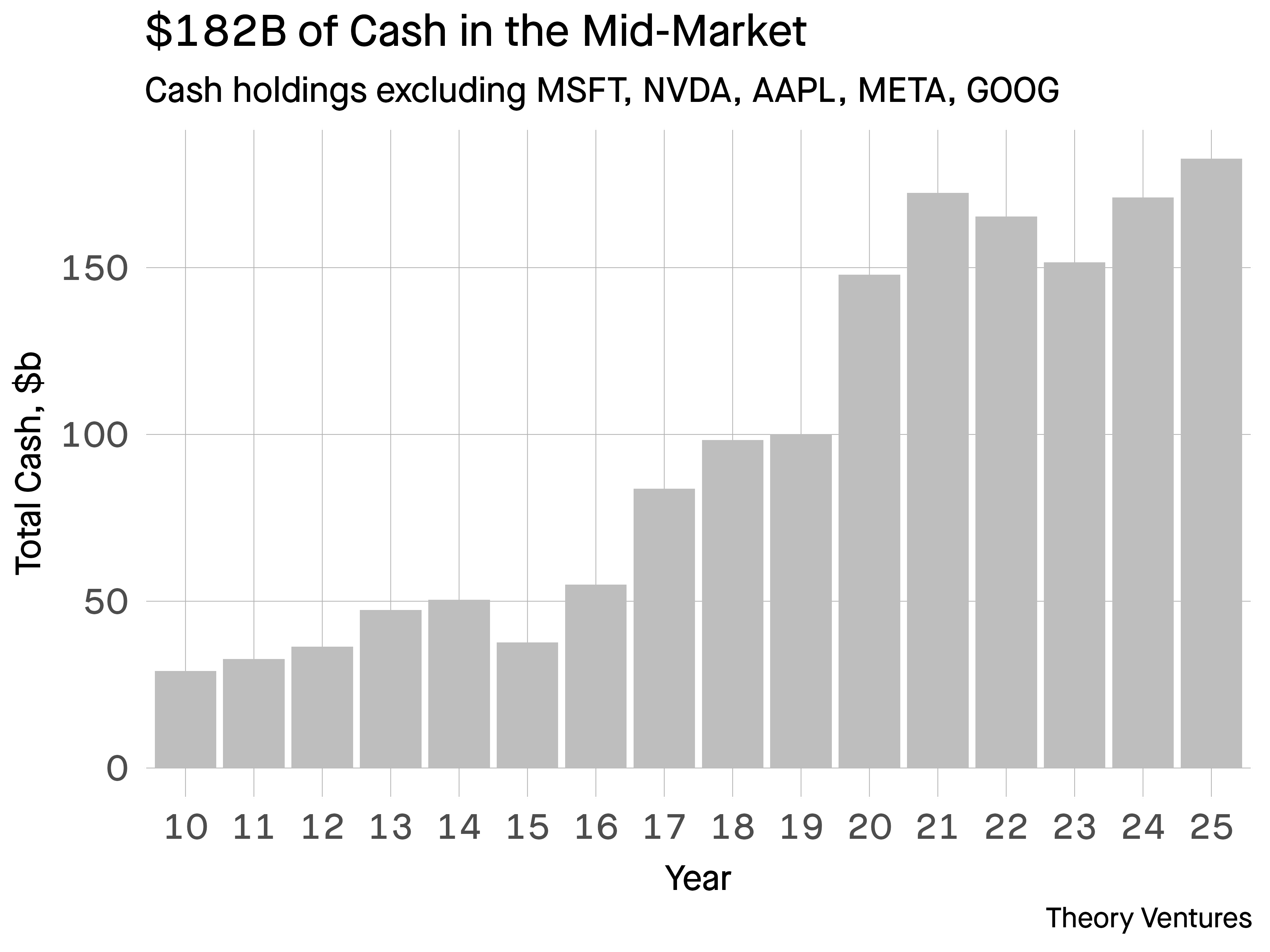

Yet substantial purchasing power remains across the sector totalling $182b.

Yet substantial purchasing power remains across the sector totalling $182b.

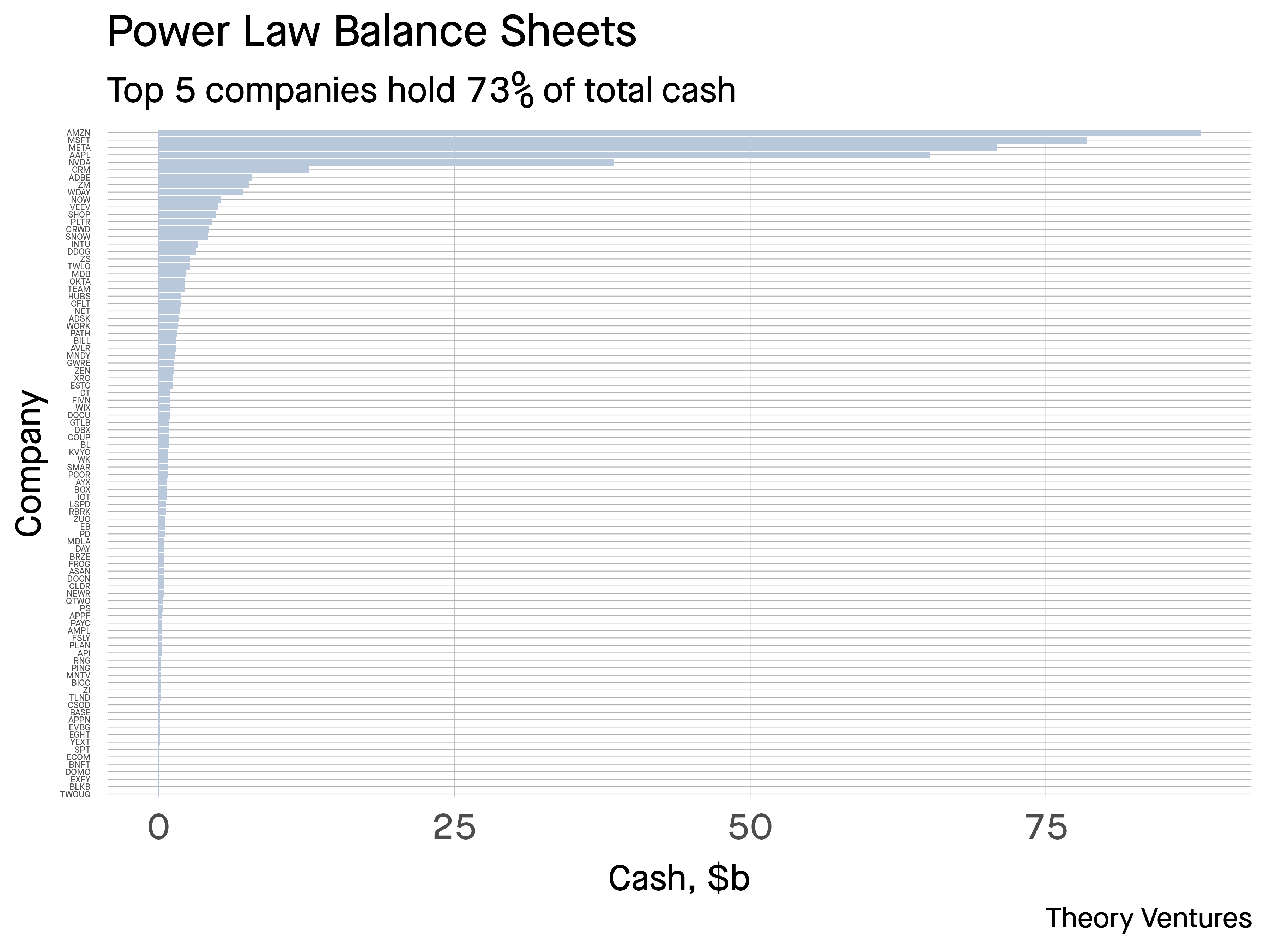

While the average publicly traded software company holds $5.2b, the median of $769m better reflects the market’s structure due to power law distribution. Plenty of capital for a $1b+ acquisition, if stock is used.

In addition, this doesn’t include any of the private unicorns.

The one counterargument : the Magnificent 5’s stocks have appreciated 33% in 2024, worth $475b, & stock-based acquisitions could be attractive & the regulatory regime which has hampered their activities may be slackening.

However, $250b in 2025 in approximate capex in data centers projected is a significant investment already.

With hyperscalers cutting record-breaking checks on AI infrastructure, 2025 sets the stage for mid-market companies to emerge as the primary drivers of software M&A.

1This figure excludes their stock purchasing power (some transactions use stock entirely or combine stock & cash) & potential debt financing.

2These companies are net producers of cash. Microsoft produced $118b of cash from operations in FY 2024 for example.