2 minute read / Apr 21, 2017 /

Is There a No Man's Land in SaaS ACVs?

A founder asked me recently if a dead zone in ACVs (average contract value) exist around the $10k price point. Yesterday, I listened to a podcast in which an executive asserted that infrastructure software priced lower than $250k in ACV threatens the viability of the company. What does the data show?

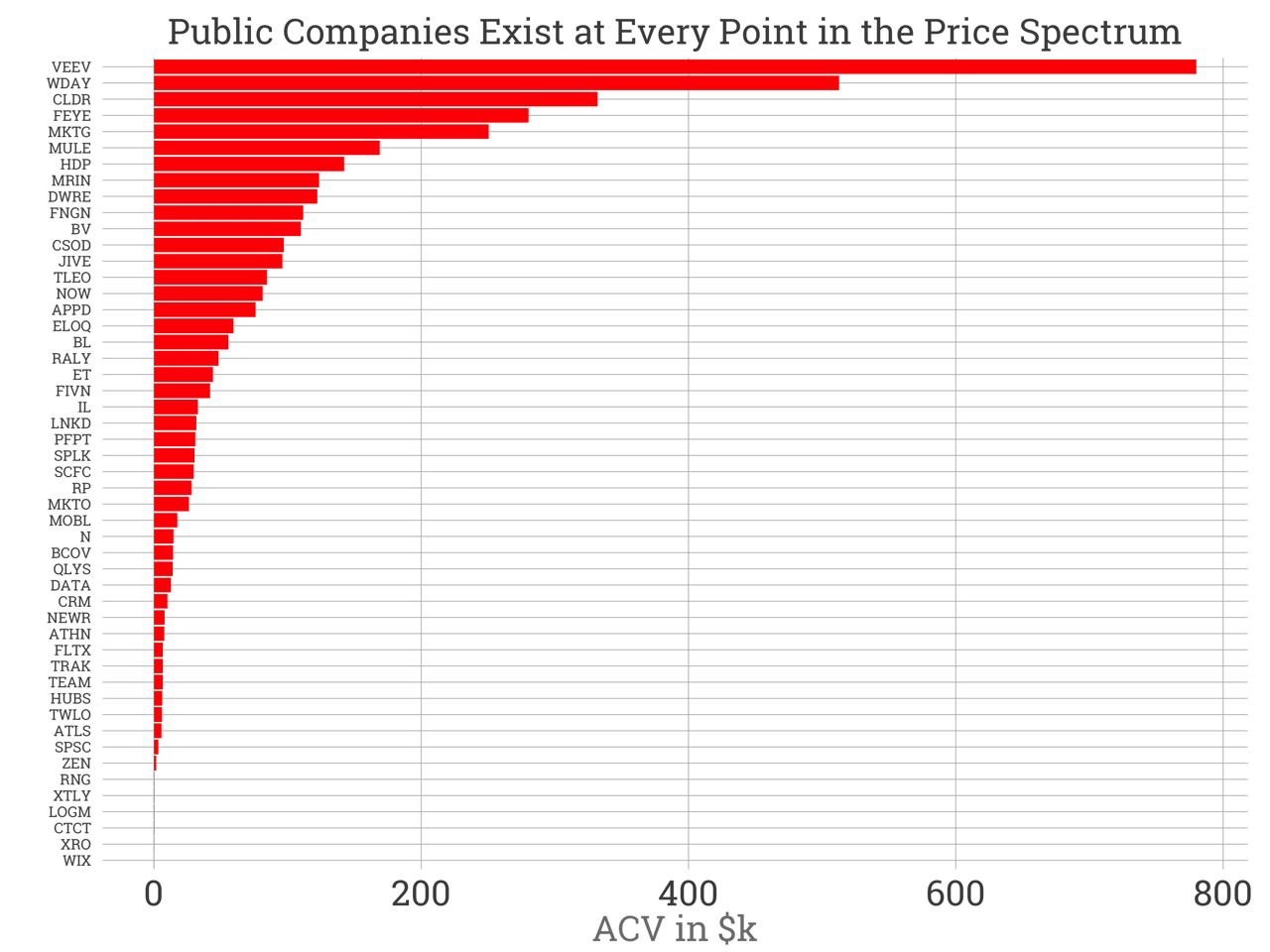

I’ve plotted the distribution of ACV at IPO for all public software companies. There are no yawning gaps but a smooth progression from $87 to $780,000. So there are successful companies at every price point.

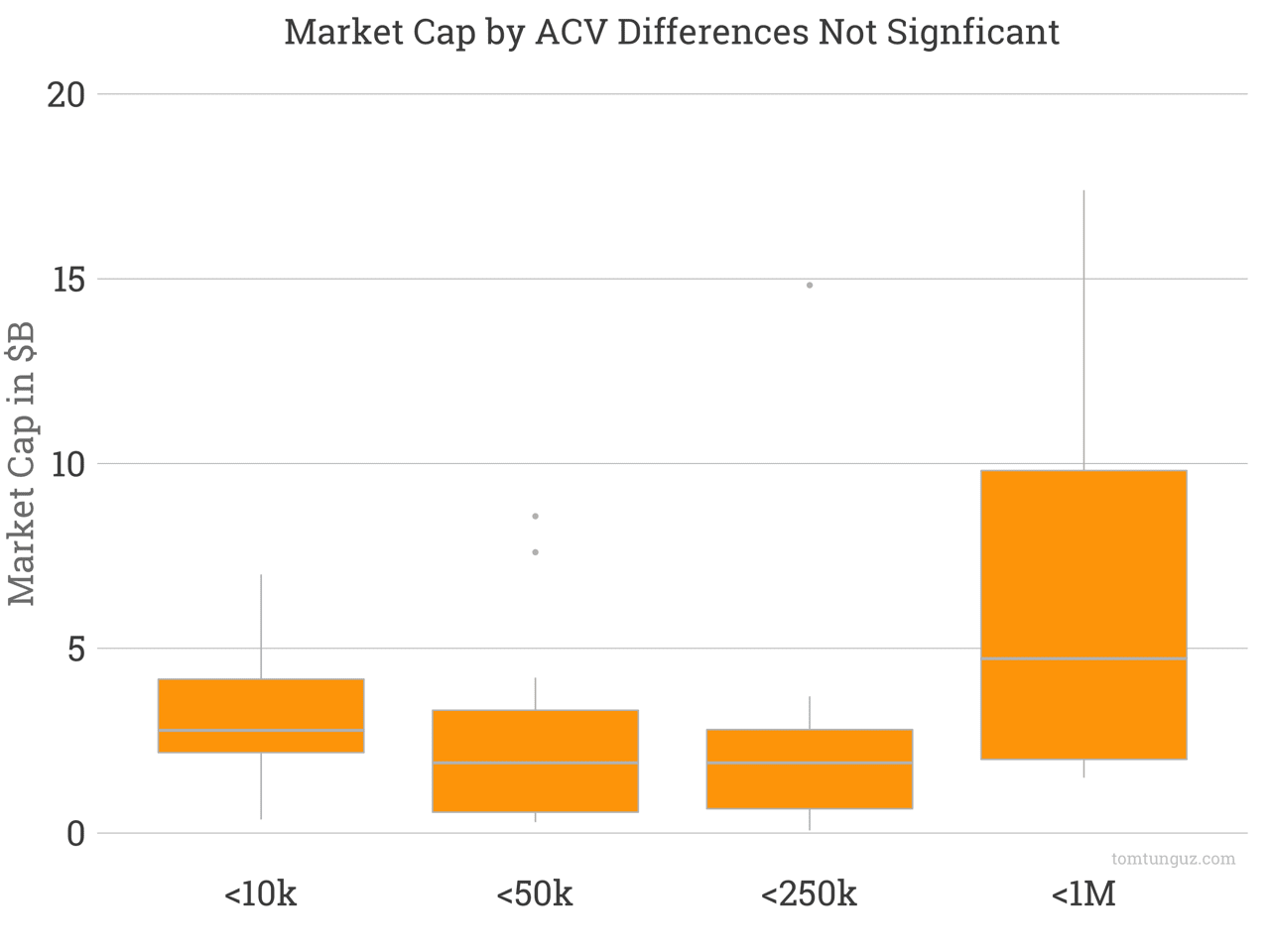

What about the typical market capitalization by price point? Do higher priced companies build bigger companies? The box plot above shows the market cap distribution in four roughly equally sized buckets. But the differences aren’t statistically significant. P values are 0.37 for the most extreme pair (<10 and 250k-1M). Note I’ve removed two outliers from the 50k bucket to make the chart easier to read.

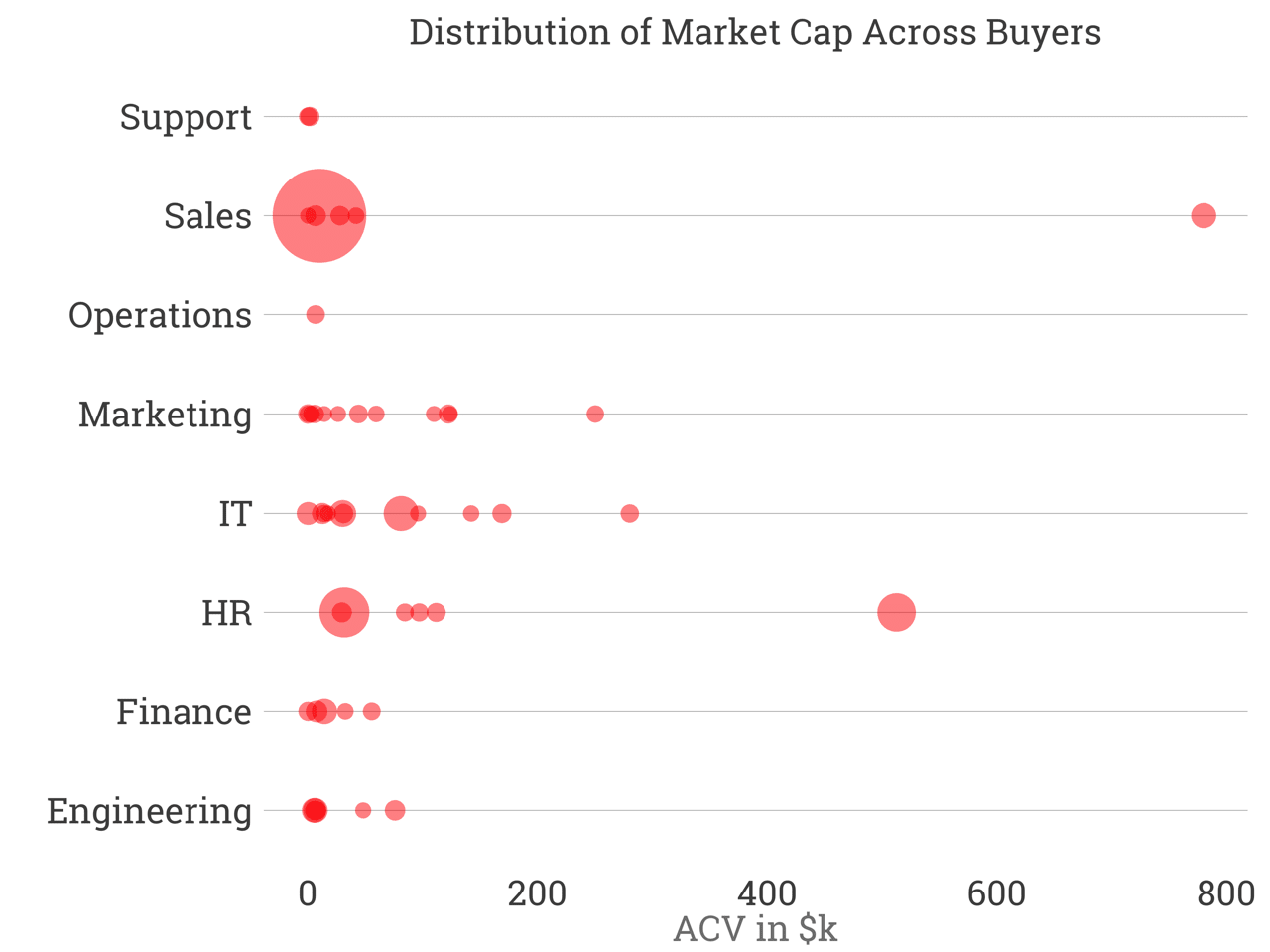

Perhaps looking at price point and buyer type might shed some light.

Not really. Not much of a pattern in the point chart above.

Looking at the success cases, we can conclude there’s existence proof of successful software companies at every price point.

This analysis suffers from survivorship bias. We are analyzing only the companies who have succeeded. To answer the question fully, we would need to calculate the startup bankruptcy rate by ACV. Unfortunately, I don’t have that data set.

Is there a dead zone in ACV? Large public companies have been built at every price point from $100 to $1M. It can be done and has been. Of course, a startup’s customer acquisition tactics, financing strategy, team and product must change to match the customer segment.

So the better question that we can’t answer is: Which is the most risky price point to pursue as a SaaS company? That all hinges on the business’s unit economics.