Wing.vc published the Enterprise Tech 30 last week. It’s a coaches poll of the top enterprise startups broken into early, mid and growth stage. Congratulations to all the companies and in particular, the 8 Redpoint companies on the list: Mattermost, Cockroach Labs, LaunchDarkly, Tray.io, AppZen, Snowflake, Hashicorp and Stripe.

Coaches polls are fun because they provide a different perspective on the market. I analyzed the data set and added a few columns to it to see if there are any trends.

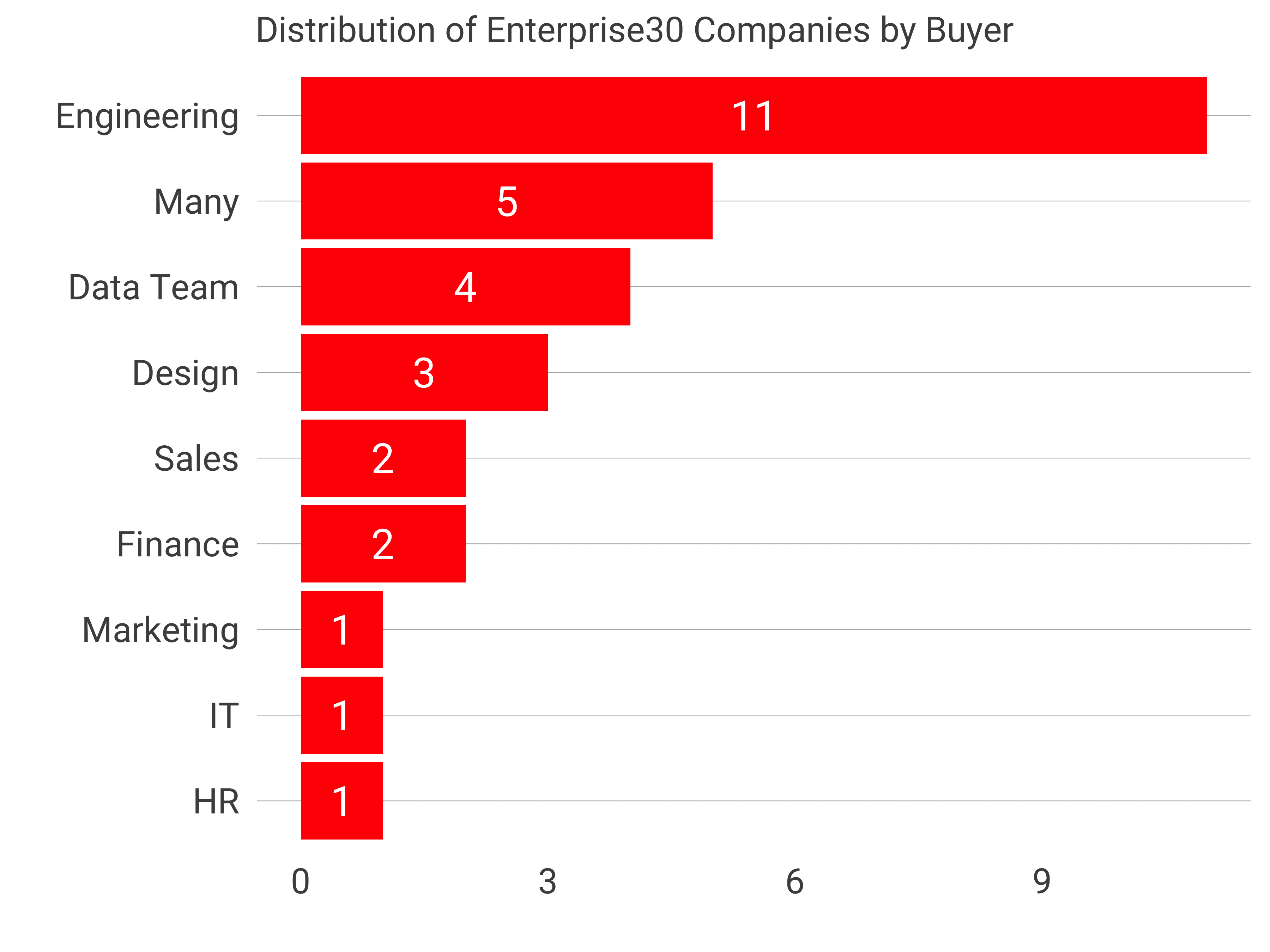

I categorized each company by their primary buyer. Engineering dominates with 37%. Many is the next category. These are products that sell across departments: Mattermost, Notion, Zapier, etc. Design is next, followed by Sales and Finance.

I categorized each company by their primary buyer. Engineering dominates with 37%. Many is the next category. These are products that sell across departments: Mattermost, Notion, Zapier, etc. Design is next, followed by Sales and Finance.

These are very different buyers than I expected. A few years ago, I analyzed the public market cap of SaaS companies by buyer. HR and Sales dominated, with IT a close third. Engineering barely made the list. I should re-run that analysis. But this data suggests the distribution will be markedly different in a few years.

5 of the 11 companies selling to engineering are open source - about half. Open source remains a viable customer acquisition strategy despite the threat from the cloud vendors; Amazon in particular.

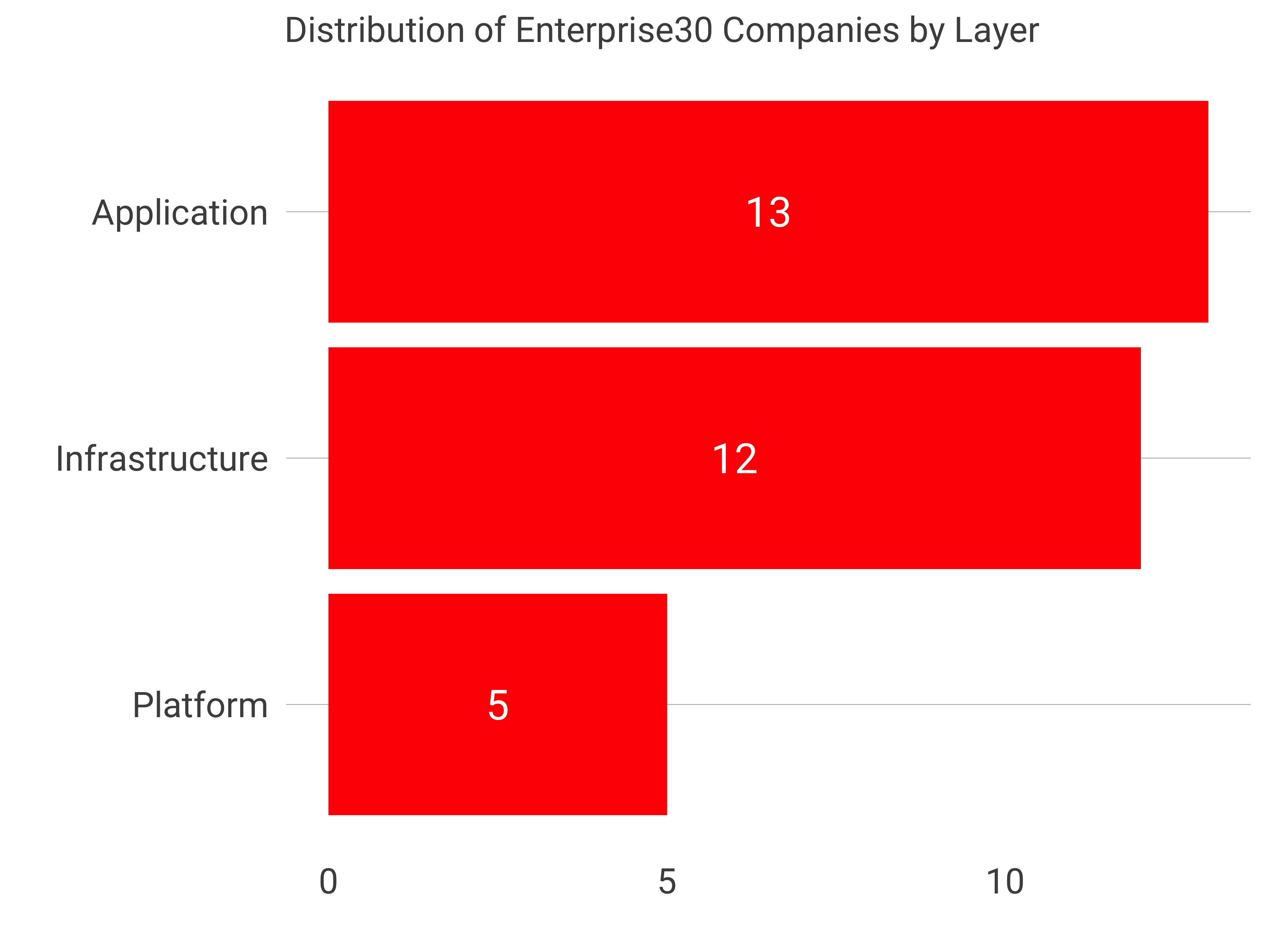

Next, I divided the top 30 companies by their place in the stack. We think of enterprise companies in three layers. Applications are software used by business users. Platform includes products that help developers to build applications: payment gateways and low code platforms. Infrastructure comprises core information technology: databases, monitoring, key management.

Next, I divided the top 30 companies by their place in the stack. We think of enterprise companies in three layers. Applications are software used by business users. Platform includes products that help developers to build applications: payment gateways and low code platforms. Infrastructure comprises core information technology: databases, monitoring, key management.

Application and Infrastructure companies each represent about 40% with Platform filling out the rest. If we were to weight this by market cap, we would see a different result since Stripe’s most recent round values the company at $22B+.

The data does suggest there are fewer companies in the platform layer, though, which is consistent with our experience.

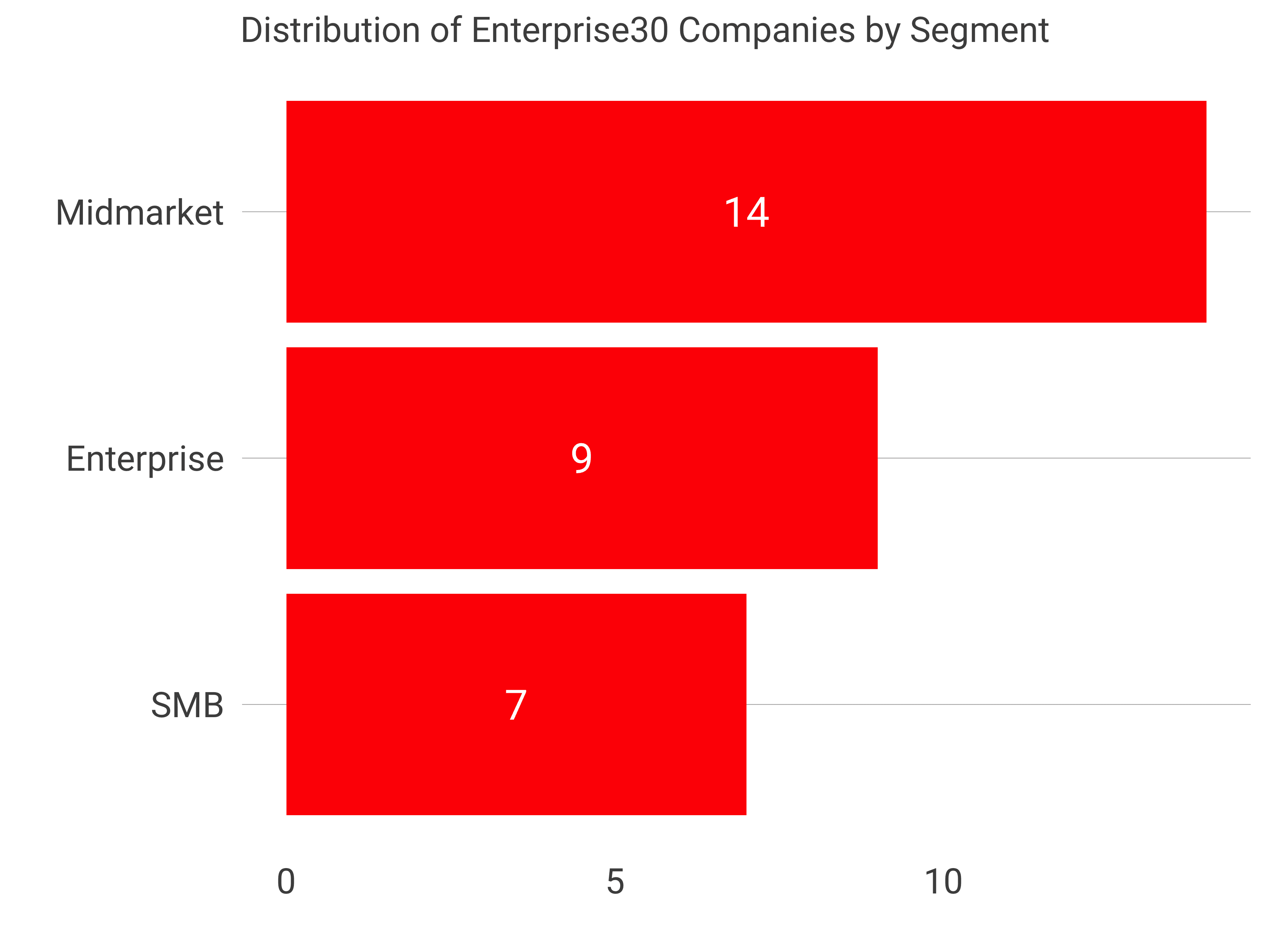

Last, I bucketed the companies into price segments: SMB, Mid-Market and Enterprise, based on my estimates of their ACVs. As I’ve said many times, there are many ways to build a very successful business. And the data shows that. There’s a broad distribution of companies across each price segment.

Last, I bucketed the companies into price segments: SMB, Mid-Market and Enterprise, based on my estimates of their ACVs. As I’ve said many times, there are many ways to build a very successful business. And the data shows that. There’s a broad distribution of companies across each price segment.

It’s always interesting to see how other investors view the enterprise market. Thanks to the team at Wing for pulling together this great survey.