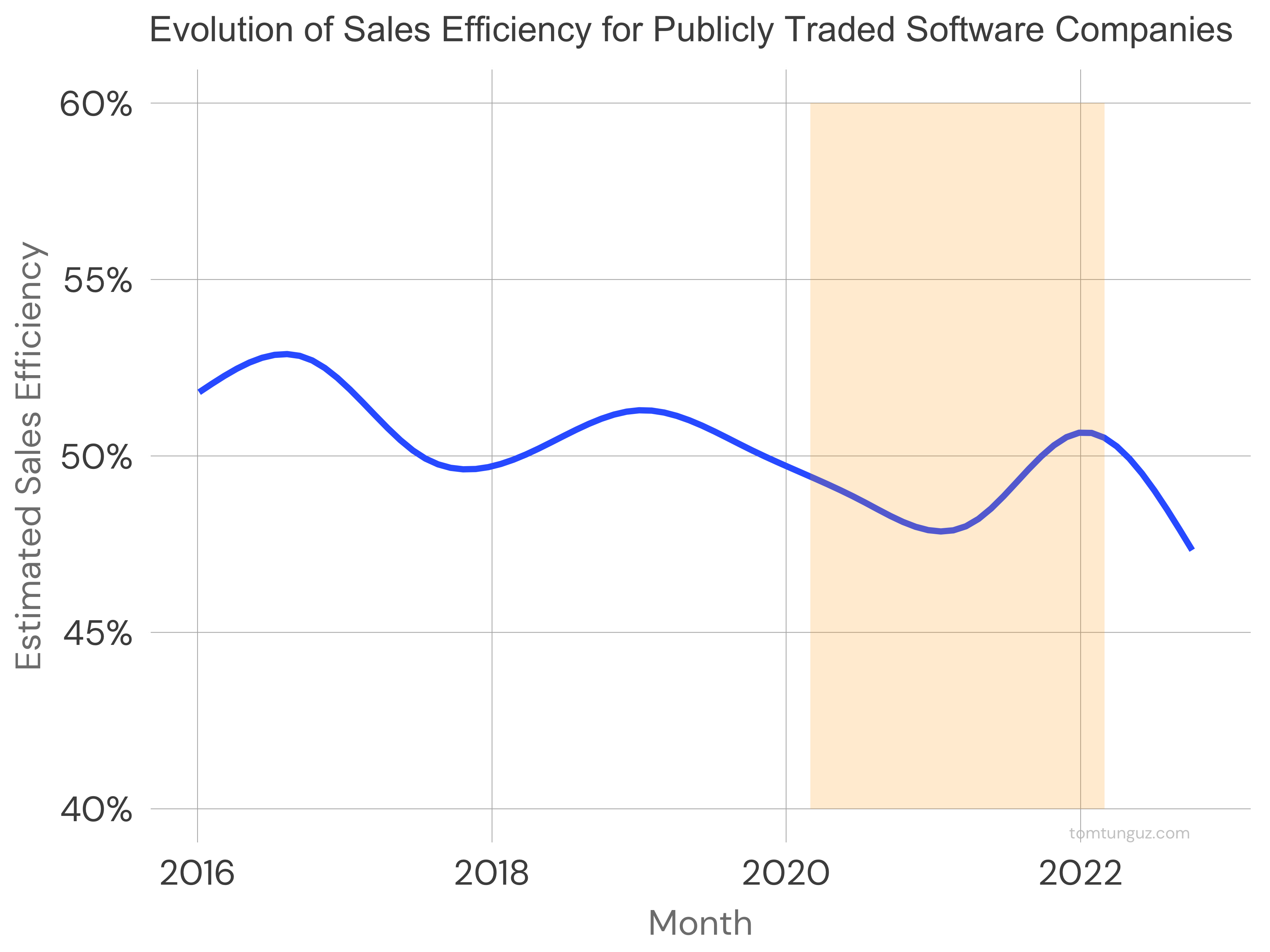

Cutting R&D to Grow GTM Spend : Is it Happening Across Software Companies?

During Office Hours with Lee Kirkpatrick, Lee recalled managing a startup through a downturn. The business cut R&D spend to conserve cash. By prioritizing sales & marketing, the company successfully lengthened runway to increase revenue, which eased the subsequent fundraising.

I wondered if a similar pattern existed in the public software markets. Actually, the opposite is true: software companies spend more on R&D (research & development) & less on Sales & Marketing (S&M) as a percent of revenue today than six years ago.