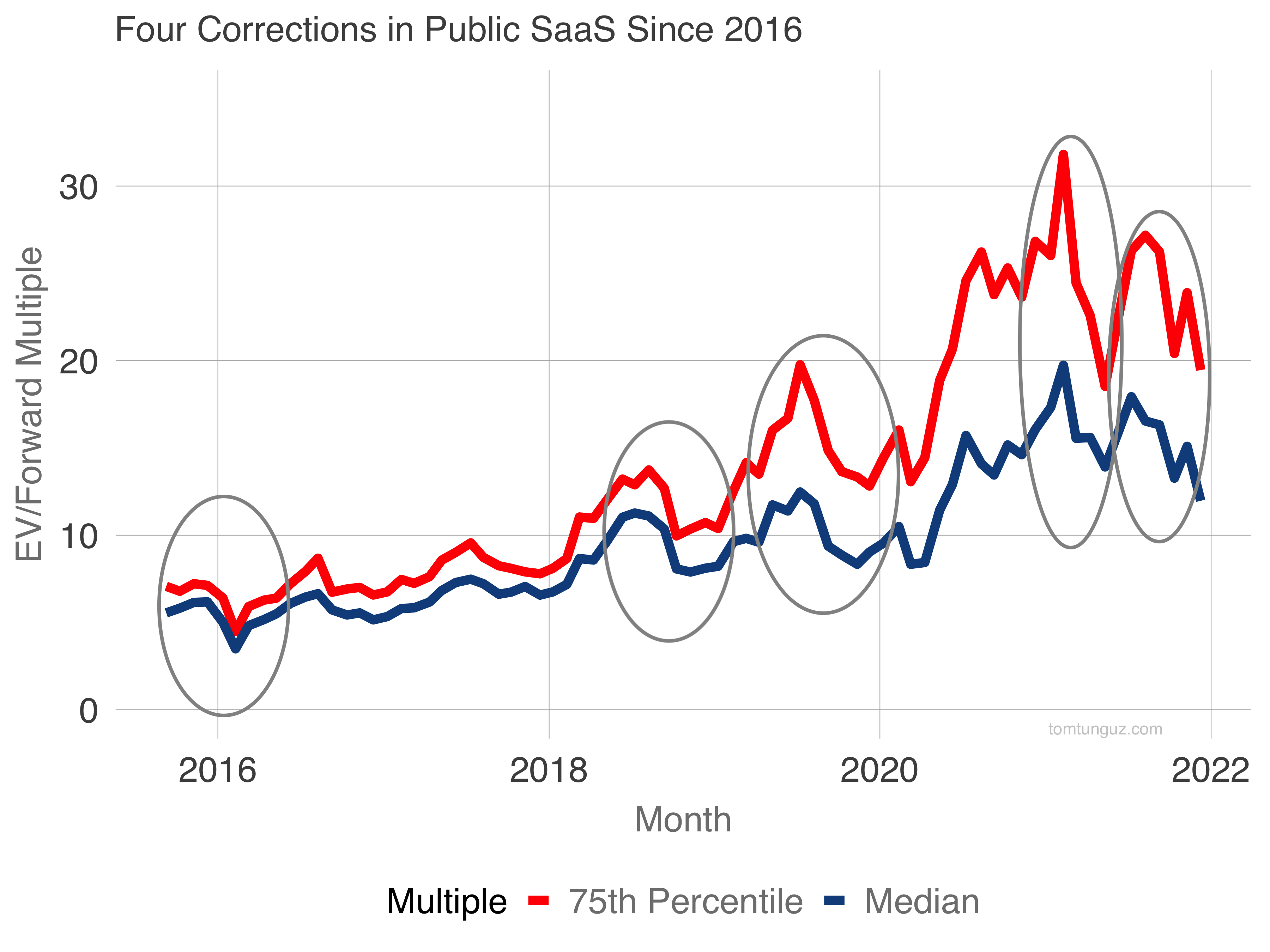

The Fifth SaaS Correction

Since 2016, public software has witnessed four corrections. Today, we’re in the midst of the fifth. Also, 2014 to 2016 saw a 57% reduction in multiples and of course after 2008. But let’s look at the most recent five years.

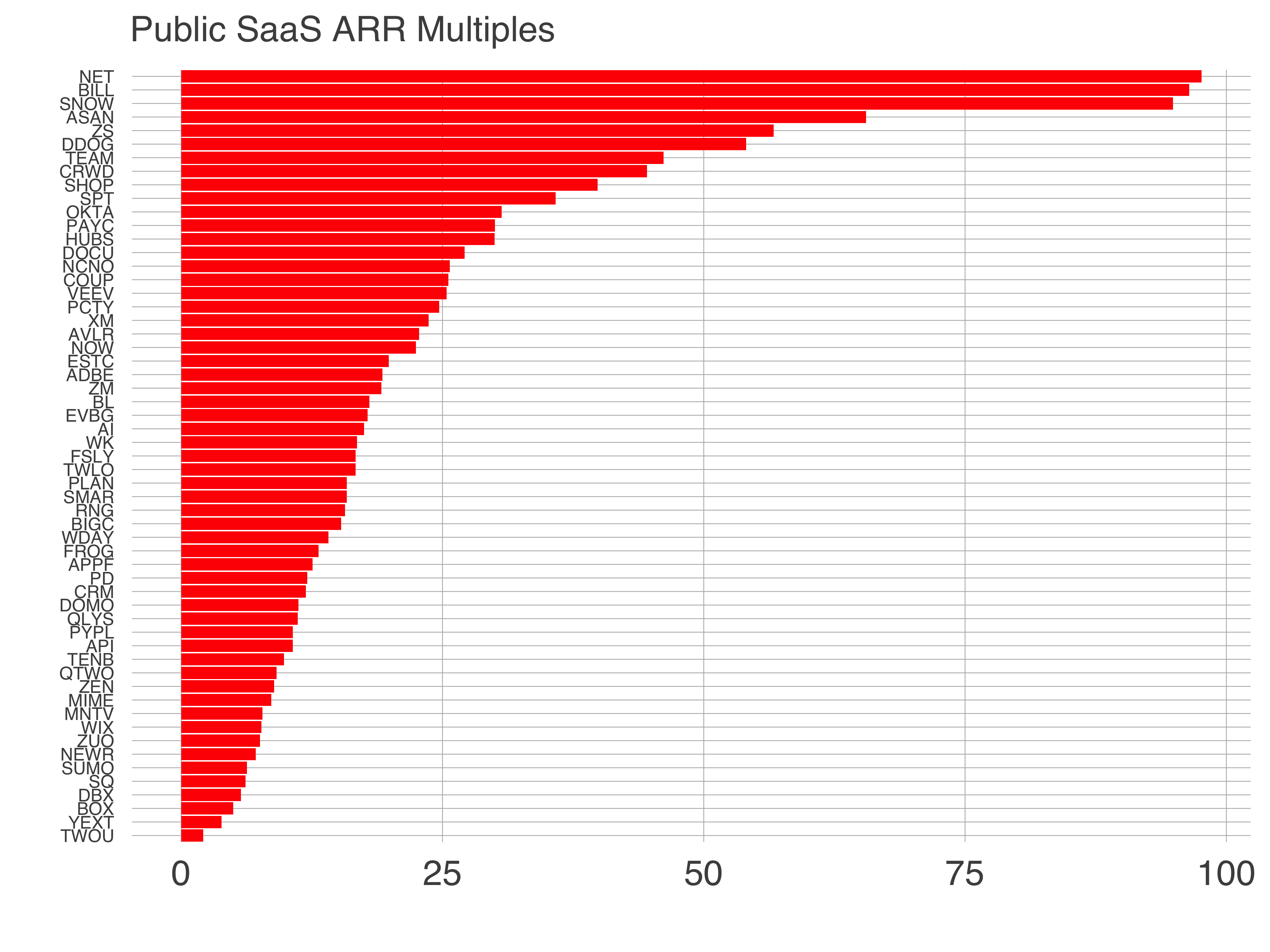

This chart shows the median and the 75th percentile of enterprise value/forward revenue multiple for the basket of public stocks which were public at that moment in time.

We believe the 2020s are the decade of data. The trends are ubiquitous and plain. The number of data teams is growing as more companies rely on data for daily operations. In addition, the sophistication of these teams has progressed meaningfully in the last five years.

We believe the 2020s are the decade of data. The trends are ubiquitous and plain. The number of data teams is growing as more companies rely on data for daily operations. In addition, the sophistication of these teams has progressed meaningfully in the last five years.