A funny thing happened along the way to Sand Hill Road in the last decade : startups stopped talking about how much runway a Series A would buy them.

In the 2000s, when capital was scarcer, founders & VCs would derive round size by debating the quantum of money required to achieve Series B milestones.

When capital is scarce, it’s rationed.

In the 2010s, US venture capital grew 40x in 10 years. More capital meant the constraints of yester-decade no longer applied. Founders declared a maximum acceptable dilution instead.

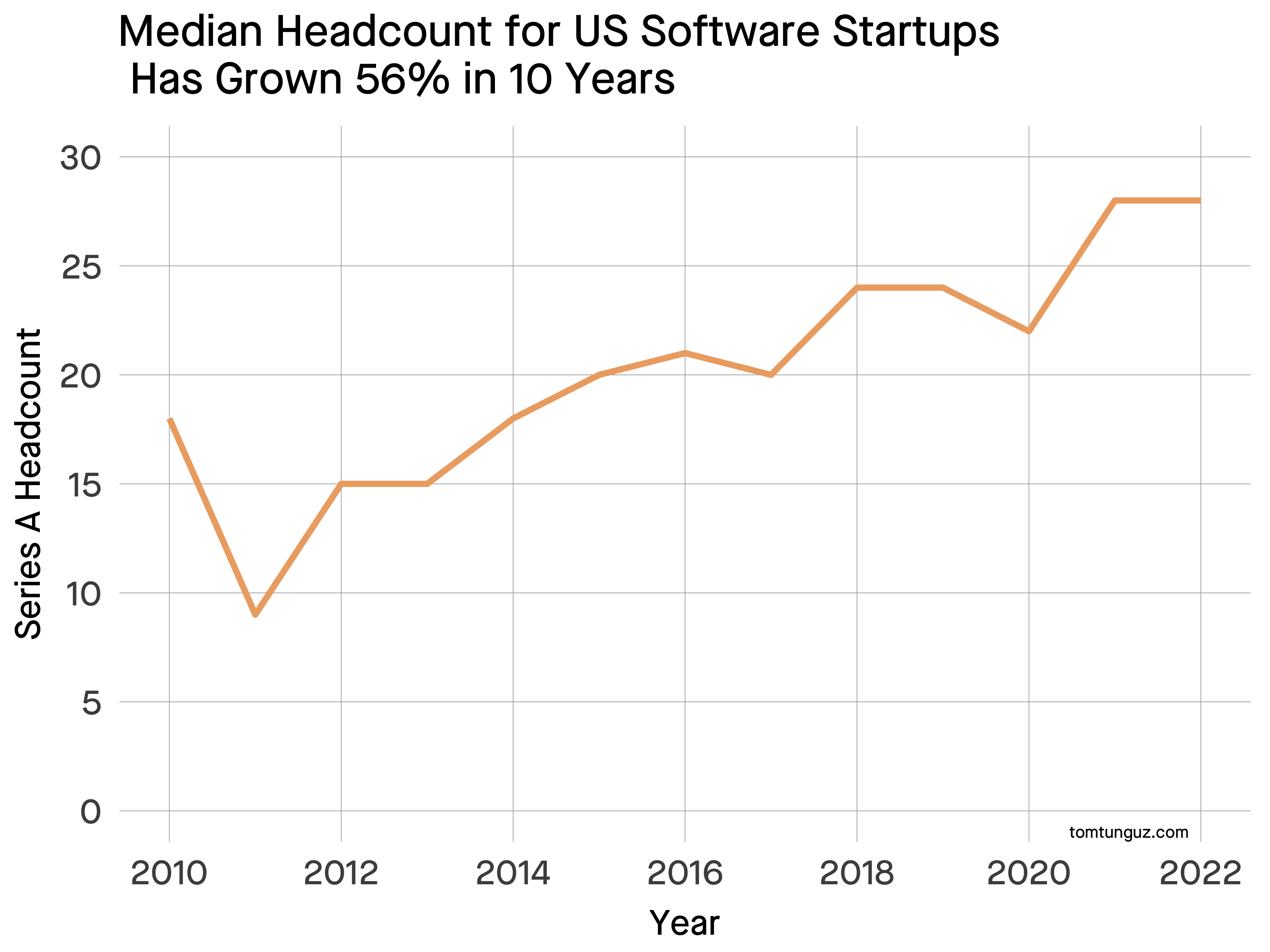

Round sizes ballooned. So, did headcount at the Series A. In 11 years, the median headcount at Series A swelled from 15 to 28. [1]

As the pendulum swings to a higher-cost-of-capital-environment, milestone-based financing may return. Let me explain :

| Era | Median Employees at A | Median Salary | Median Round | Runway in Months |

|---|---|---|---|---|

| 2010 | 15 | 150k | 3.2 | 17 |

| 2021 | 28 | 200k | 16.1 | 35 |

| 2021 | 28 | 200k | 7.8 | 17 |

In 2010, the median software Series A startup raised $3.2m & employed 15 people at about $150k average cost. Series A dollars provided the business 17 months’ of runway at constant burn assuming no revenue.

In 2021, employment costs per capital increased to roughly $200k. At 28 employees, a $16m Series A fueled the company for 35 months. That’s a lot of buffer to achieve Series B metrics [1].

But we’re no longer in 2021. Today, the public markets value companies like it’s 2017.

If the Series A market follows suit, the median series A will fall to $7.8m, which means a 28 person company will have 17 months’ of runway - effectively identical to 2010 runway.

Capital scarcity curtails startup operation. Team sizes will winnow to lengthen runway. Fewer person hours means less marketing, sales pitches, & bookings. Founders & VCs would debate how much capital is required to attain Series B milestones at higher salaries than a decade ago.

I doubt the pendulum will reach the touch the capital scarcity of 2010, if only because VCs have more than $200b in dry powder.

But, I wouldn’t be surprised if milestone-based financings re-emerge to justify round sizes again.

[1] Thank you to the Pitchbook team for running the headcount analysis data. [2] Tangentially, this is why the burn multiple (total burned / total ARR) has become an important investor metric.