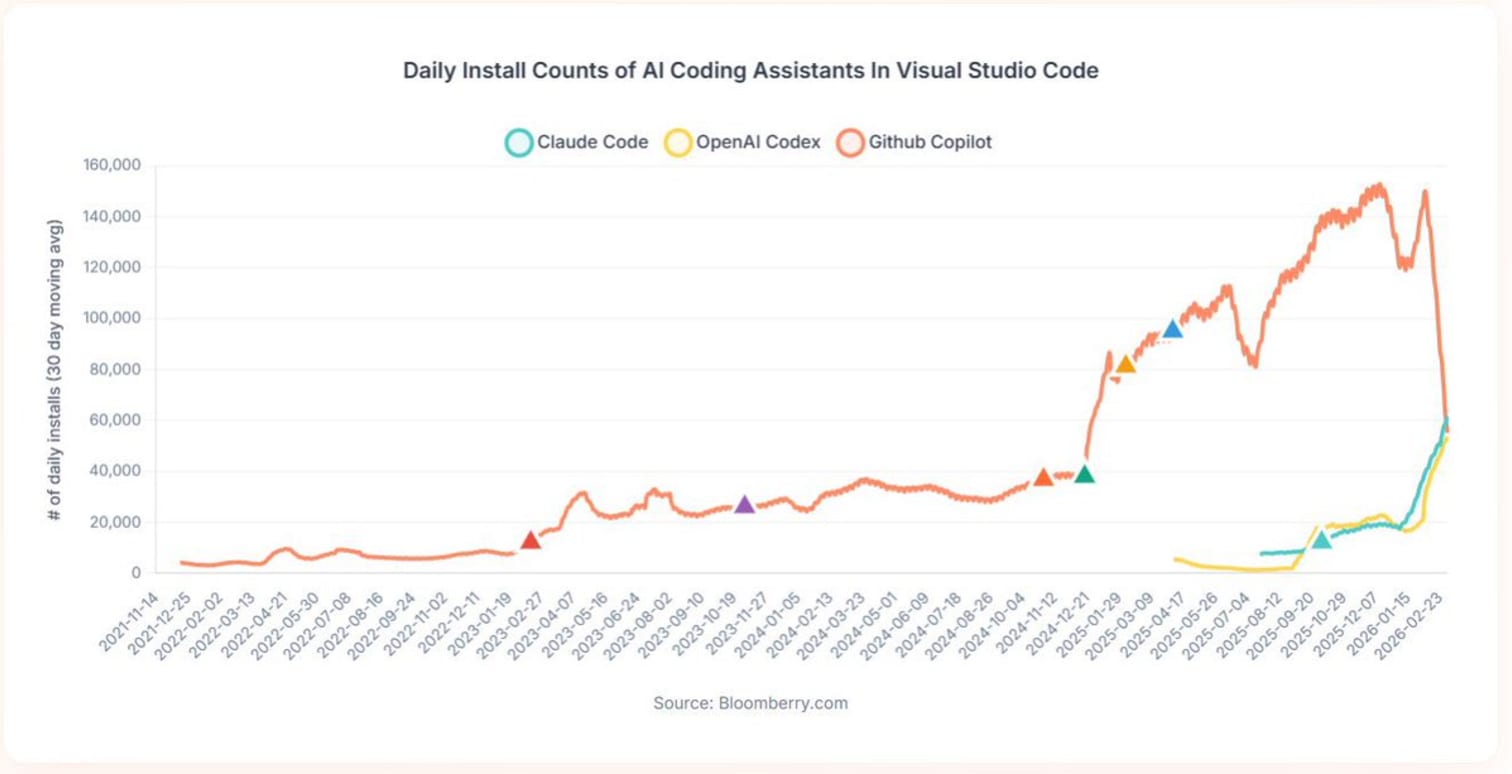

GitHub Copilot pioneered AI coding assistance. First to market. 20 million users. Then Claude Code & OpenAI Codex launched in mid-2025. Within six months, Copilot’s daily installs peaked & declined while competitors surged past 100,000 combined.1

The sword didn’t fall on a laggard. It cut the early leader. If Microsoft can lose share in six months, no one is safe.

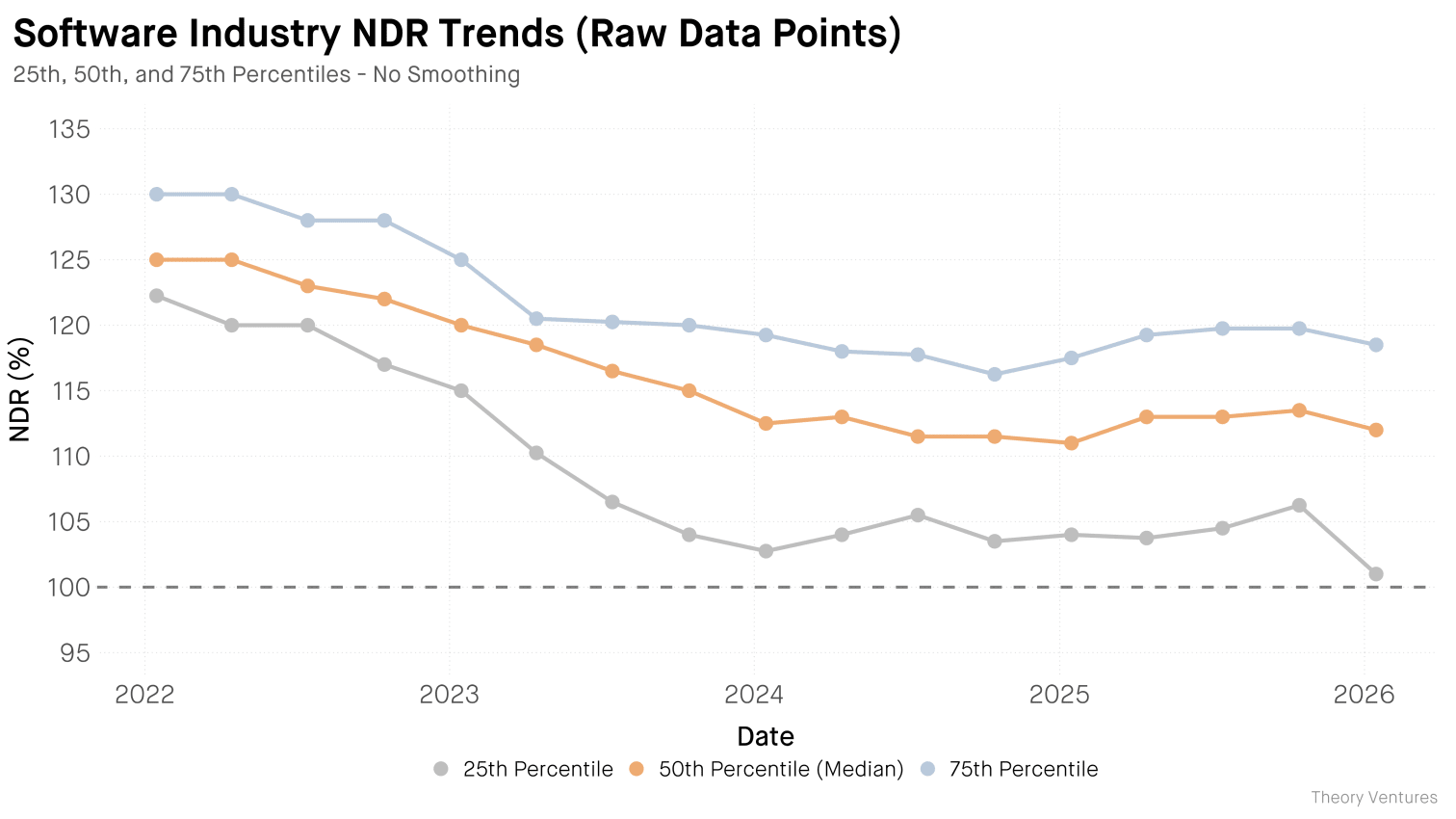

I analyzed 374 quarterly NDR observations from 25 public software companies. For years, the decline looked gradual. Net dollar retention fell from 125% in 2022 to 112% in 2025. Quarter by quarter. No cliff when ChatGPT launched. No acceleration when enterprises adopted Copilot.

Then came 2026.

The 25th percentile fell from 106% to 101% in a single quarter, now touching the breakeven line.2 The weakest companies are bleeding first. Zoom sits at 98%. Asana at 96%. The bottom quartile is now contracting.

The companies in the bottom quartile face different threats, but they share one trait : products simple enough to replace. Bill.com (94% NDR) serves SMBs depressed by macro conditions.3 Zoom (98%) faces near-free alternatives in Teams & Google Meet. Asana (96%) offers task workflows that competitors & AI agents can replicate. With 96% NDR, they lose 4% of existing revenue annually. Growing 9% requires 13%+ new customer acquisition just to tread water.4

Macro pressure. Commoditization. Competition. AI. Each blade cuts differently. The bottom quartile will see accelerating losses. Some may tip into outright contraction. The sword of Damocles hangs by a single horsehair. For simpler products in competitive categories, that horsehair is fraying.

-

Source : Bloomberry.com, VS Code extension install data tracked by AznHisoka. ↩︎

-

The decline is statistically significant (p < 0.0001, R² = 0.74). ↩︎

-

SMB bankruptcies hit a 15-year high in 2025, driven by tariffs and high interest rates. Sources : PYMNTS, Bloomberg. ↩︎

-

Asana Q4 FY2026 Results : 9% revenue growth, 96% NDR. ↩︎