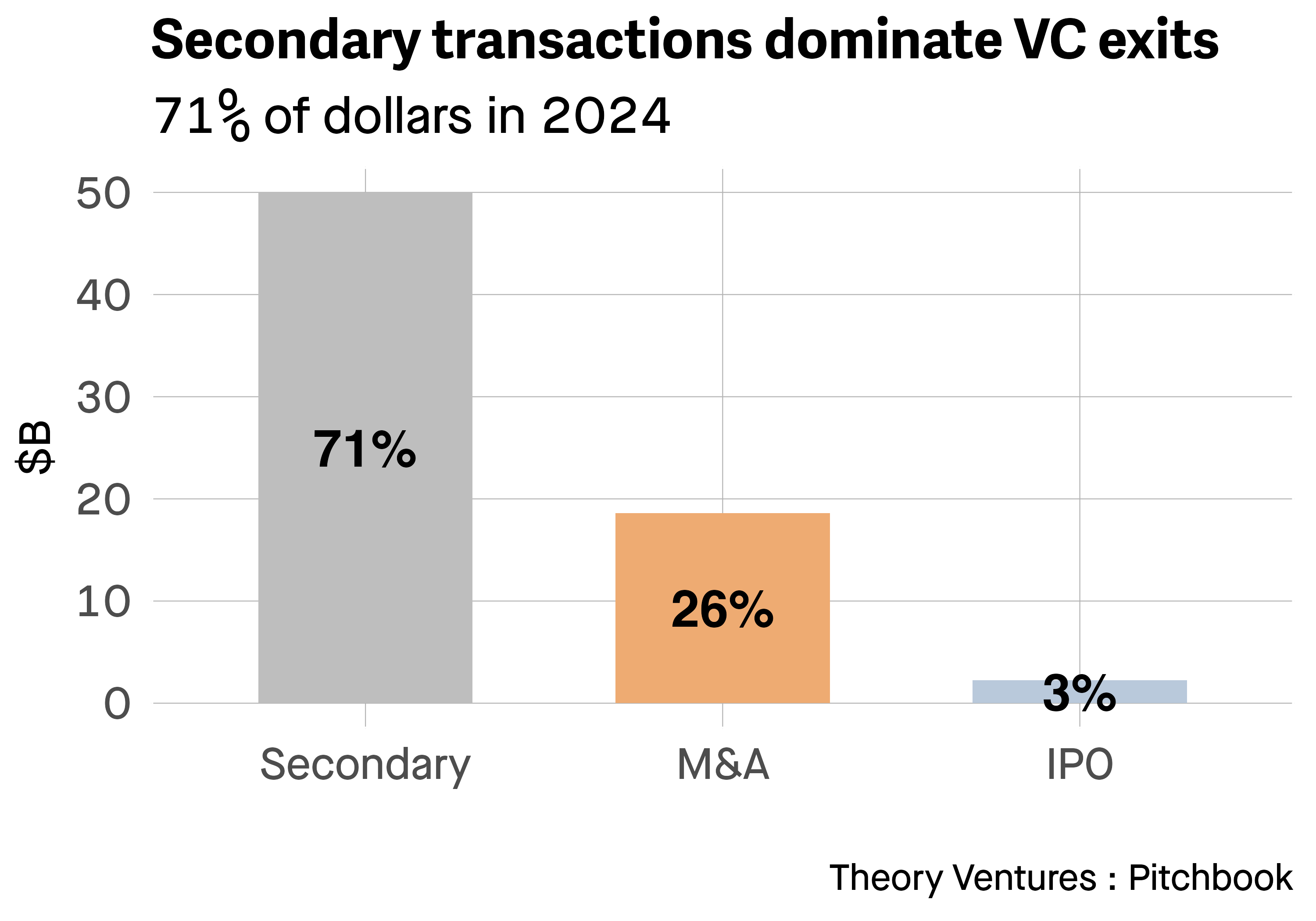

71% of exit dollars in 2024 came from a new avenue : secondaries.

Historically, IPOs and M&A have been the dominant exit paths for venture backed companies. Some years IPOs dominate, other M&A dominates, but in 2024 secondaries captured the super majority.

When a company sells new shares to investors in exchange for dollars, they create new shares in the company - primary shares. When existing shareholders sell their shares to new investors, we call this a secondary sale. An employee tender is a secondary sale offered to employees of the company. But secondary sales can also occur between one venture capitalist and another venture capitalist.

The secondaries market is incredibly opaque. So the figures gathered here are extremely rough estimates but should be directionally correct.

There has been a huge challenge in liquidity since 2022 with the IPO market effectively silent, and M&A also stymied.

In response, capital markets respond in a way they always do. They flood capital where there’s opportunity. And now the primary path to liquidity within venture are secondaries. This is based on a Pitchbook analysis of the overall secondary market released in Q1 of 2025.

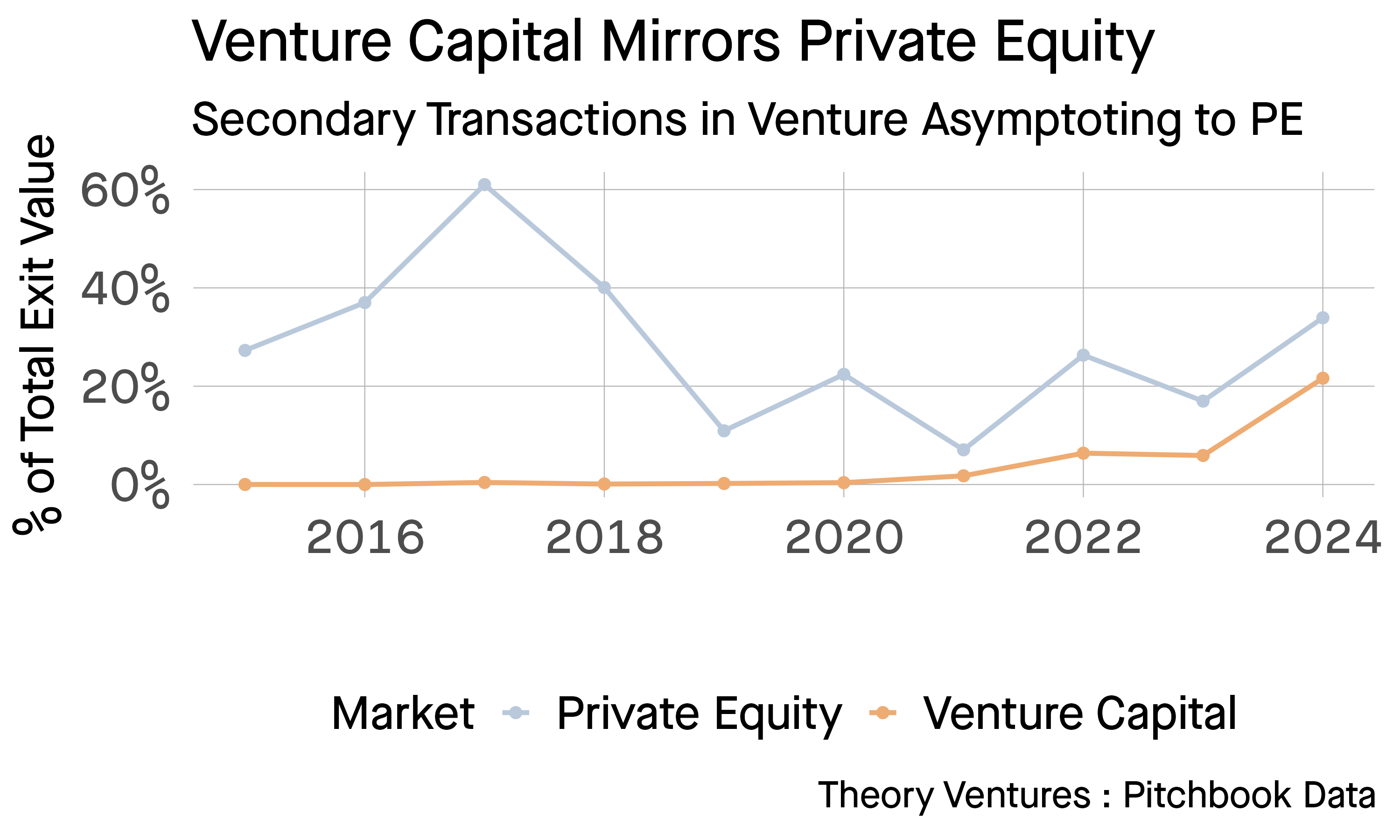

This mirrors the private equity industry. I’ve written previously about how venture capital and private equity have parallel paths.

Here I’m using a slightly different and narrower dataset, but you can see the announced transactions that have been reported that are outside the scope of private exchanges are roughly 20 to 30% within both private equity and venture capital. Over the last 10 years private equity has averaged about 28% secondaries as a form of liquidity.

Here I’m using a slightly different and narrower dataset, but you can see the announced transactions that have been reported that are outside the scope of private exchanges are roughly 20 to 30% within both private equity and venture capital. Over the last 10 years private equity has averaged about 28% secondaries as a form of liquidity.

As in private equity, we should start to expect secondaries to become a permanent and significant part of venture capital liquidity for both employees of companies and also investors.

With the target ARR required to achieve an IPO growing from $80m in 2008 to approximately $250m today, secondaries will become a permanent fixture in venture capital markets.

It’s not just a temporary anomaly, but a structural evolution in how venture capital will function and ultimately evolve to look a bit more like private equity.