Where venture capital flows, innovation follows. And for more than a decade, few faucets have been watched more closely than Y Combinator. An analysis of their investment patterns since 2020 doesn’t just reveal the accelerator’s strategy—it provides a map to the entire startup ecosystem’s next chapter.

With Demo Day approaching this week & inspired by Jamesin Seidel’s YC Series A analysis, I wondered how YC investment patterns have changed since 2020.

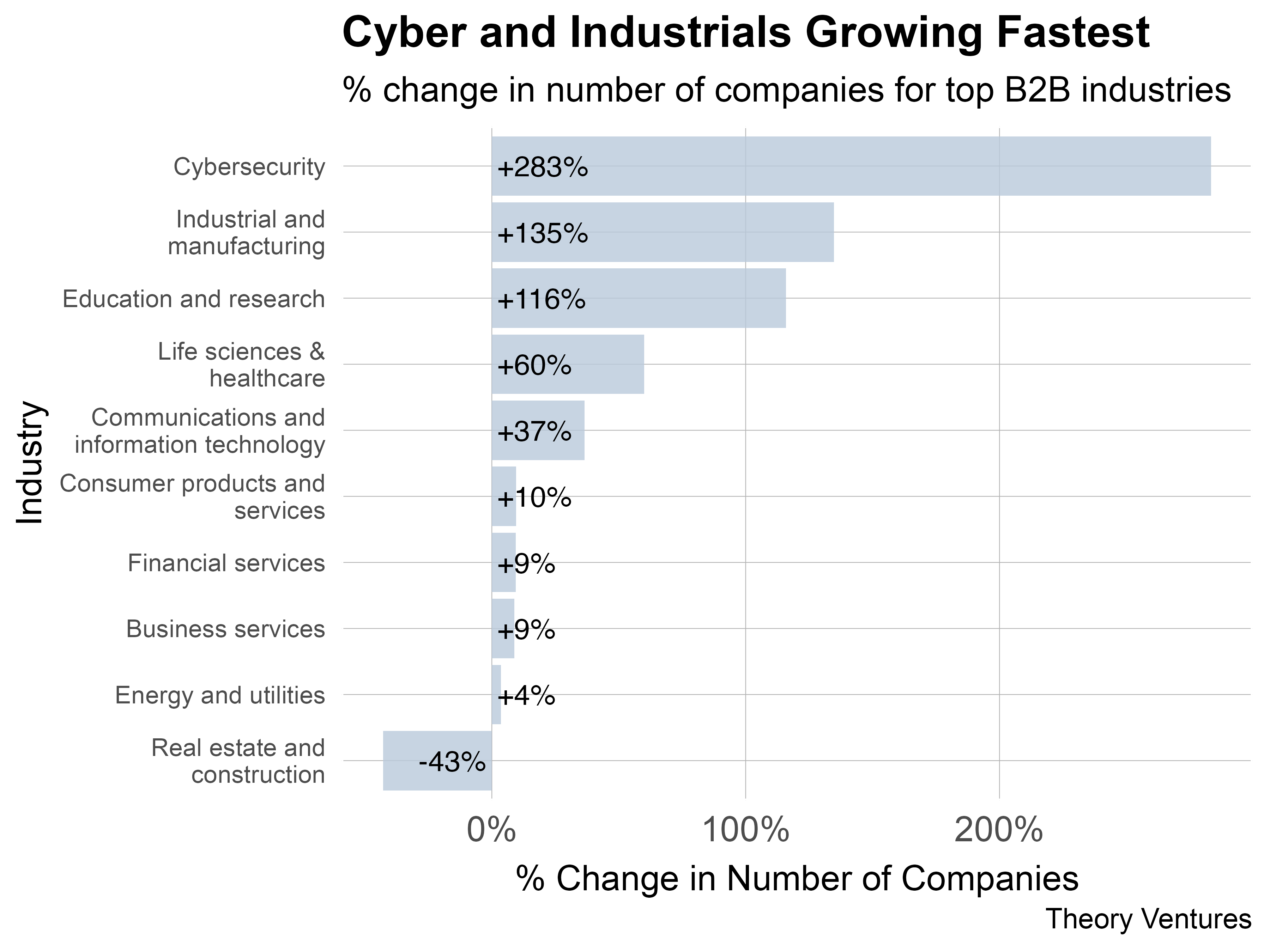

Cybersecurity and industrial/manufacturing are the two fastest growing categories. Education & life sciences are right behind. The Wiz acquisition and the overall growth rates of security companies as a durable budget within software spending has propelled security more broadly. Similarly manufacturing startups have seized on the tariff-induced reshoring opportunity.

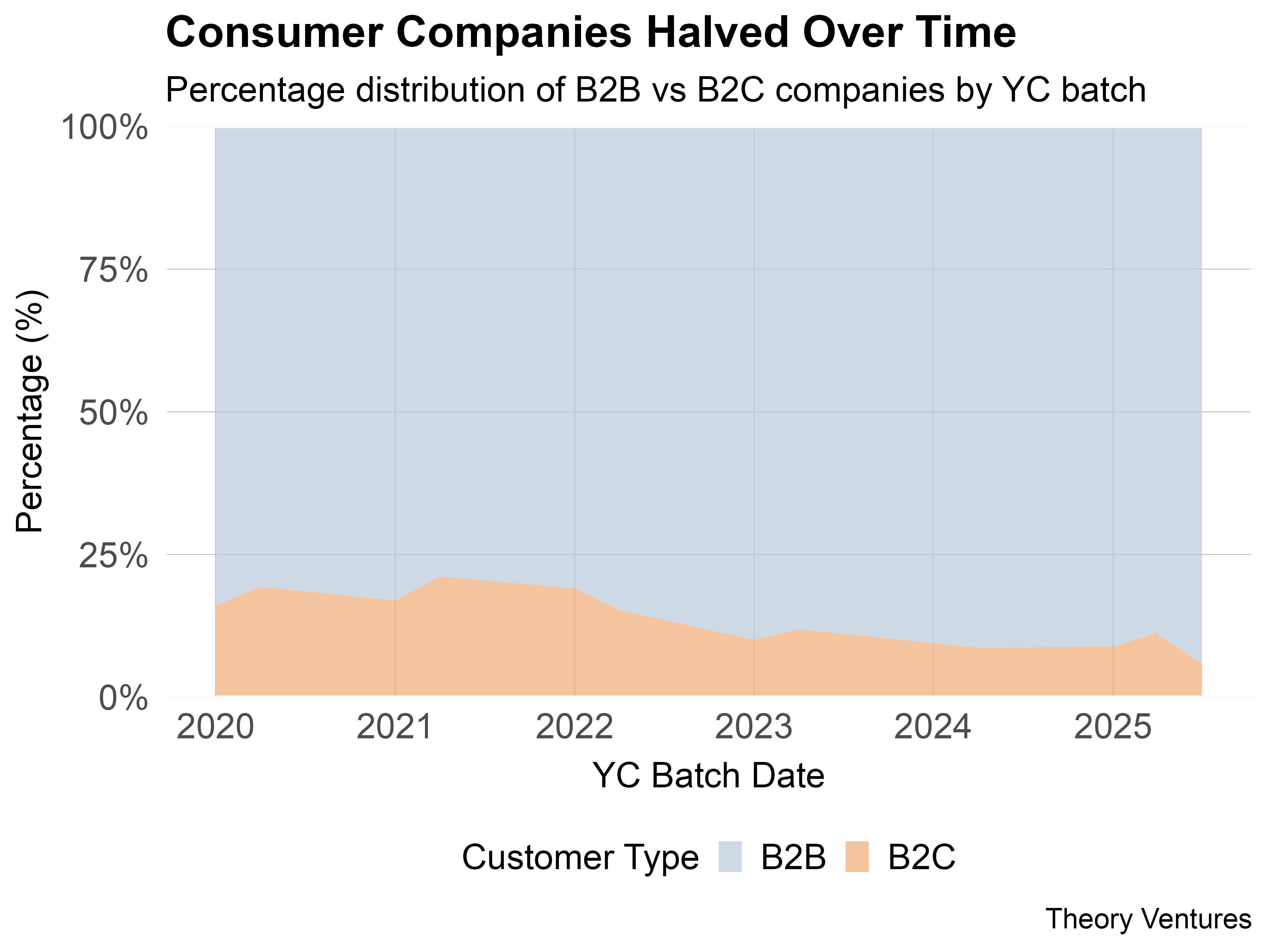

B2B companies have increased their share from roughly 80 to 90% over the last five years, which is a parallel to the broader venture industry.

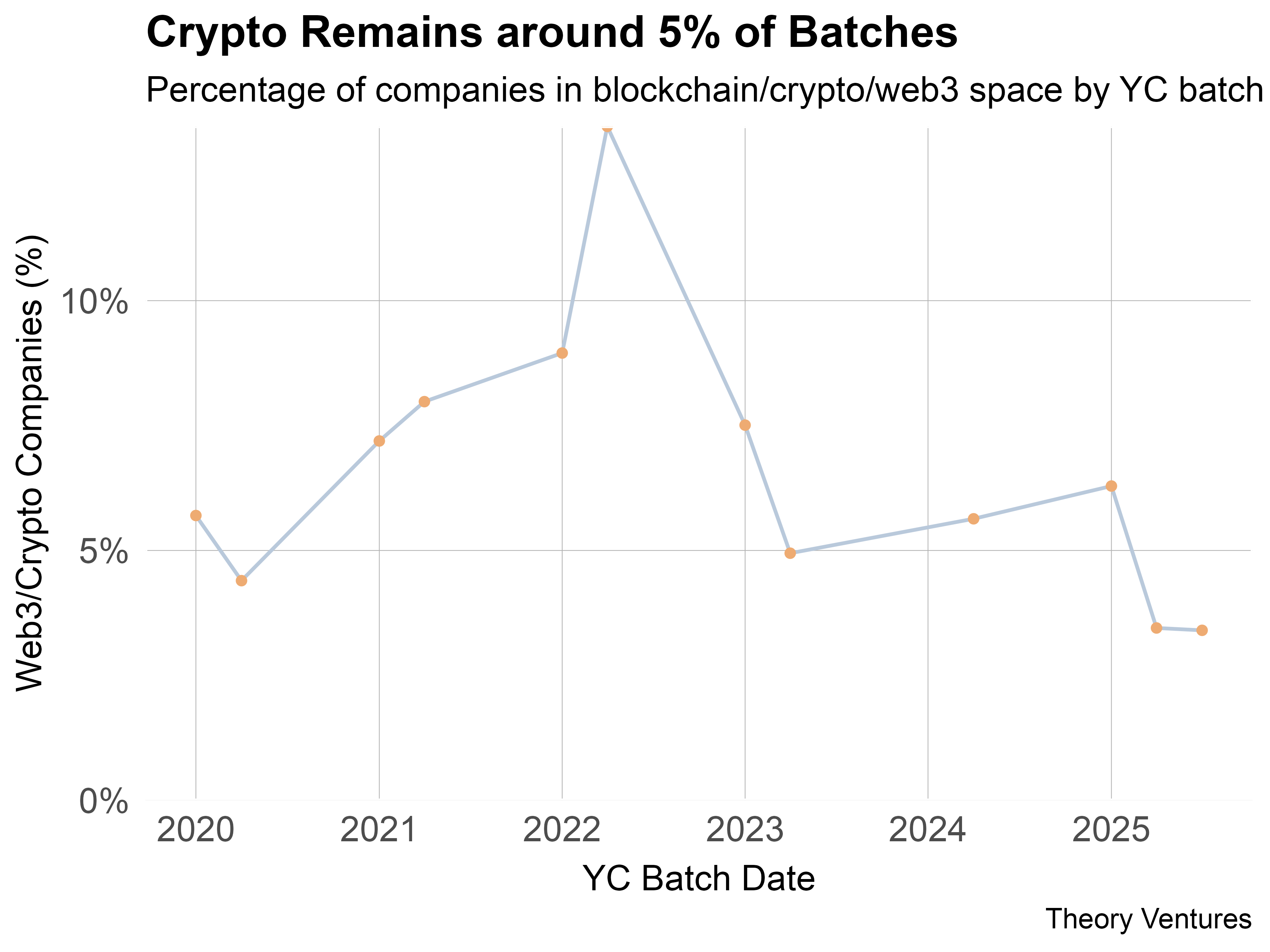

Crypto/web3 remains around 5% of investments. The 2022 spike followed the Coinbase IPO in 2021. It’s a steady but not a very large fraction of companies.

Crypto/web3 remains around 5% of investments. The 2022 spike followed the Coinbase IPO in 2021. It’s a steady but not a very large fraction of companies.

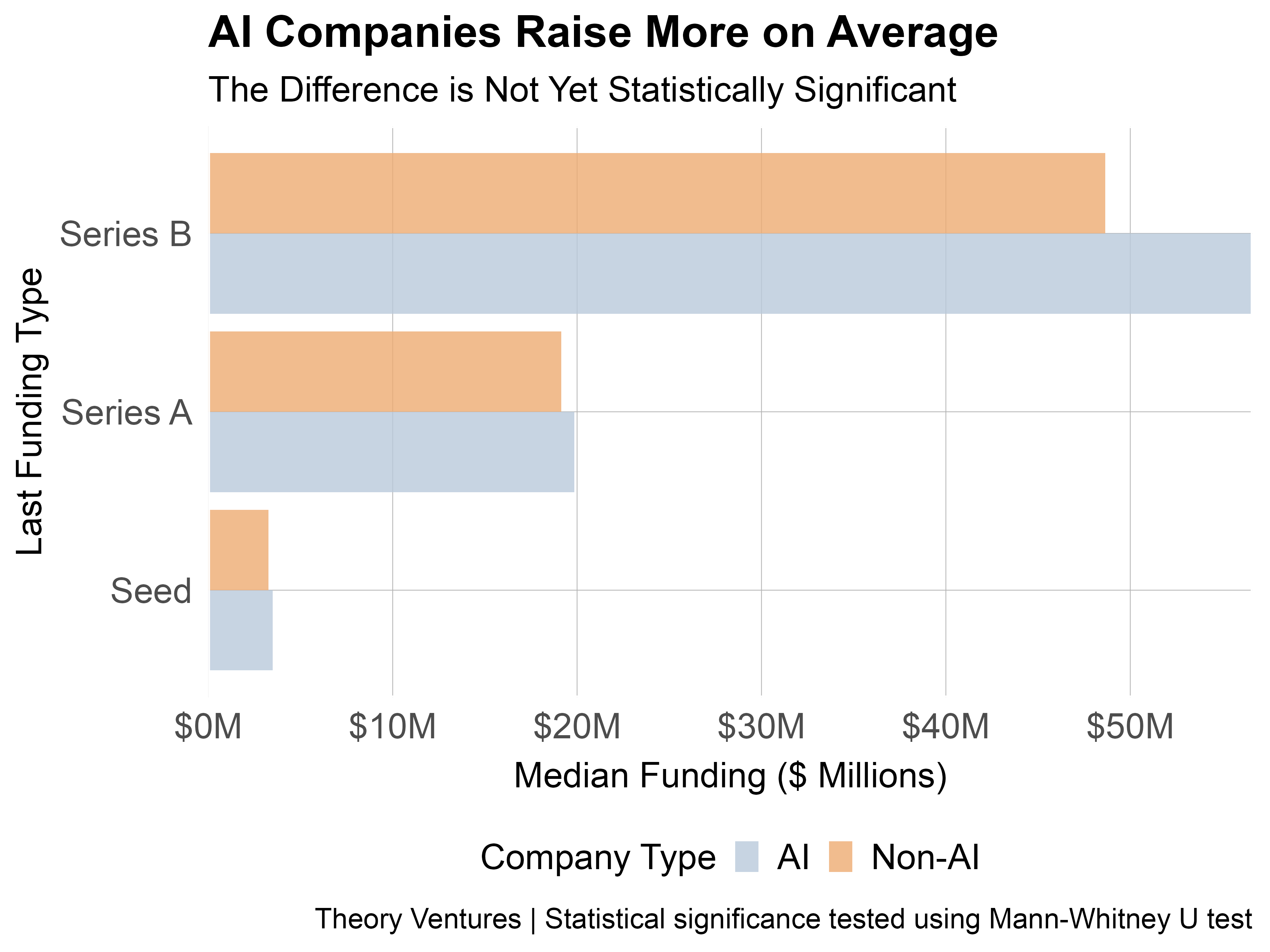

AI companies on average raise a little bit more, but the delta is not yet statistically significant - even though AI companies broadly do raise a premium.

Ultimately, YC’s portfolio mirrors the broader industry’s shift toward pragmatism. The significant growth isn’t in speculative tech, but in essential tools for manufacturing, security, and B2B. The takeaway is clear: the surest path to funding runs straight through solving a customer’s most expensive problems.