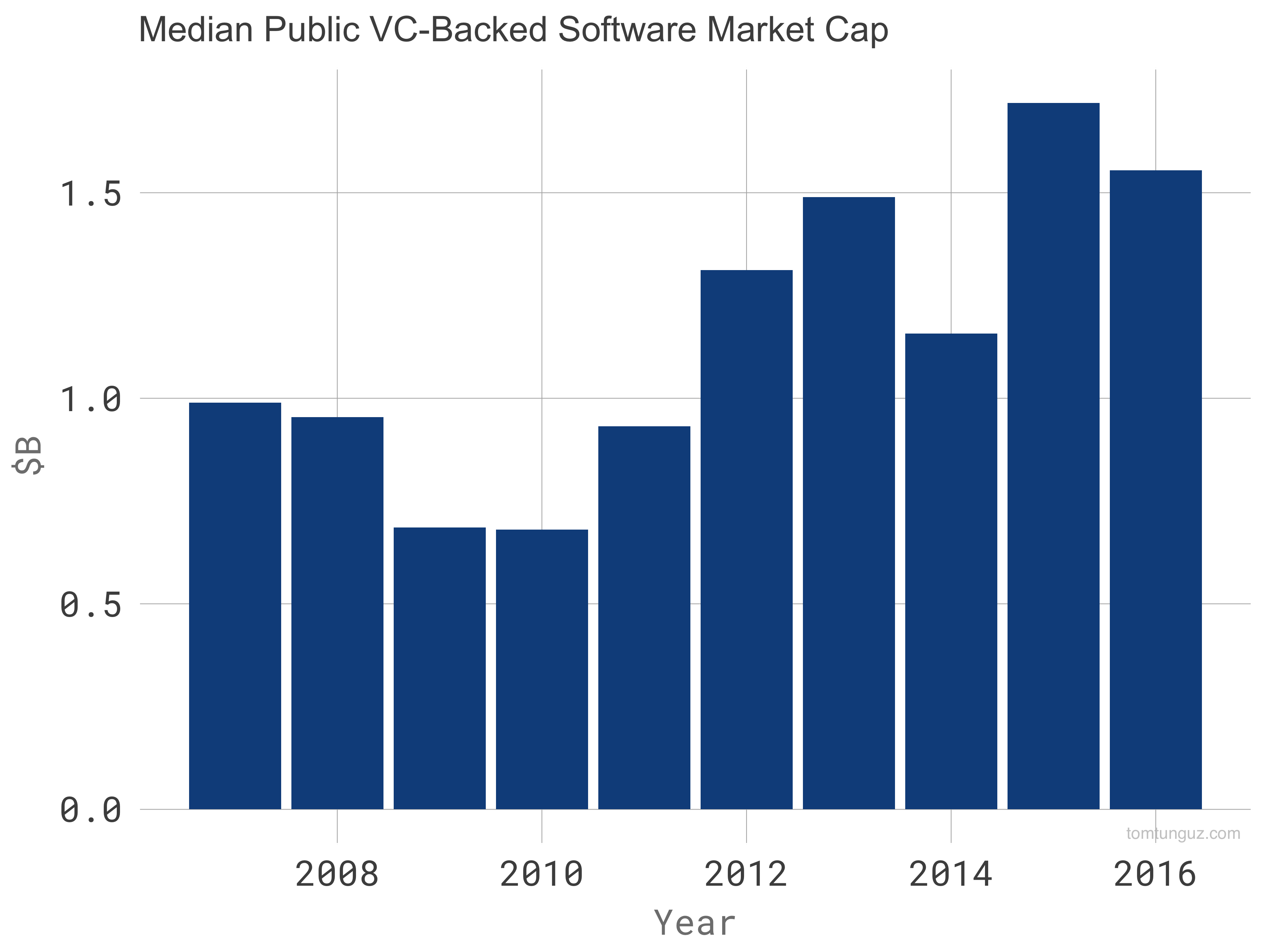

When Aileen Lee published “Welcome to the Unicorn Club” - the article that coined the word unicorn for a $1b startup - the average public SaaS company commanded a market cap of $1.5b.

{kind=link}

I remember thinking a $1b M&A or IPO was so rare an investor might hope to achieve it once or twice in a career. Fewer than 15 SaaS companies traded on public exchanges then. With at least 20 firms and several partners per firm chasing unicorns, upstarts faced stiff odds.

From 2007 to 2016, $1.5b marked the upside case for most VC software and infrastructure investment memos.

2015 Return Multiple by Round

| Round | Post, $m | Return Multiple at $1.5b |

|---|---|---|

| Seed | 8.7 | 172x |

| Series A | 28.4 | 53x |

| Series B | 74.8 | 20x |

| Series C | 139 | 11x |

| Series D | 269 | 5.6x |

If you were to read a memo from that era, you might have seen a table resembling the one above. It shows the potential return multiple from Seed to Series D at the median post-money of the era spanning 172x to 5.6x depending on the round.

Within five years, the median public SaaS market cap exploded from $1.5b to $9.8b in 2021. The return potential 10xed. The largest startups kissed $100b in market cap and higher.

Return projections skyrocketed. Competition fueled a surge in valuations.

Then the stock market’s fall reversed the effect. Mean market cap halved to about $4.5b.

2022 Return Multiple by Round

| Round | Post, $m | Return Multiple at $4.5b | RM at $1.5b (2015) |

|---|---|---|---|

| Seed | 35.2 | 128x | 172x |

| Series A | 101 | 45x | 53x |

| Series B | 352 | 12.8x | 20x |

| Series C | 857 | 5.3x | 11x |

| Series D | 2,226 | 1.9x | 5.6x |

Re-running the multiples math for today, return projections for the typical growth round collapsed. Series Cs dropped from 11x to 5.3x. Series Ds cratered from 5.6x to 1.9x by 66% - which is inline with the public market drop.

The more market caps on unicorns compress, the greater the downward pressure on rainbow foals’ valuations.

The silver lining: the median public software company in 2022 is three times as valuable as in 2015, which suggests valuations should settle higher than that era.