The Impact of Varying Sales Hiring Strategies on SaaS Startups

What are the tradeoffs when considering different sales hiring plans and which is the right one for your startup? There are many different considerations in creating a sales hiring plan. Balancing them all can be tricky, but thinking through the trade-offs is important to scaling the business well.

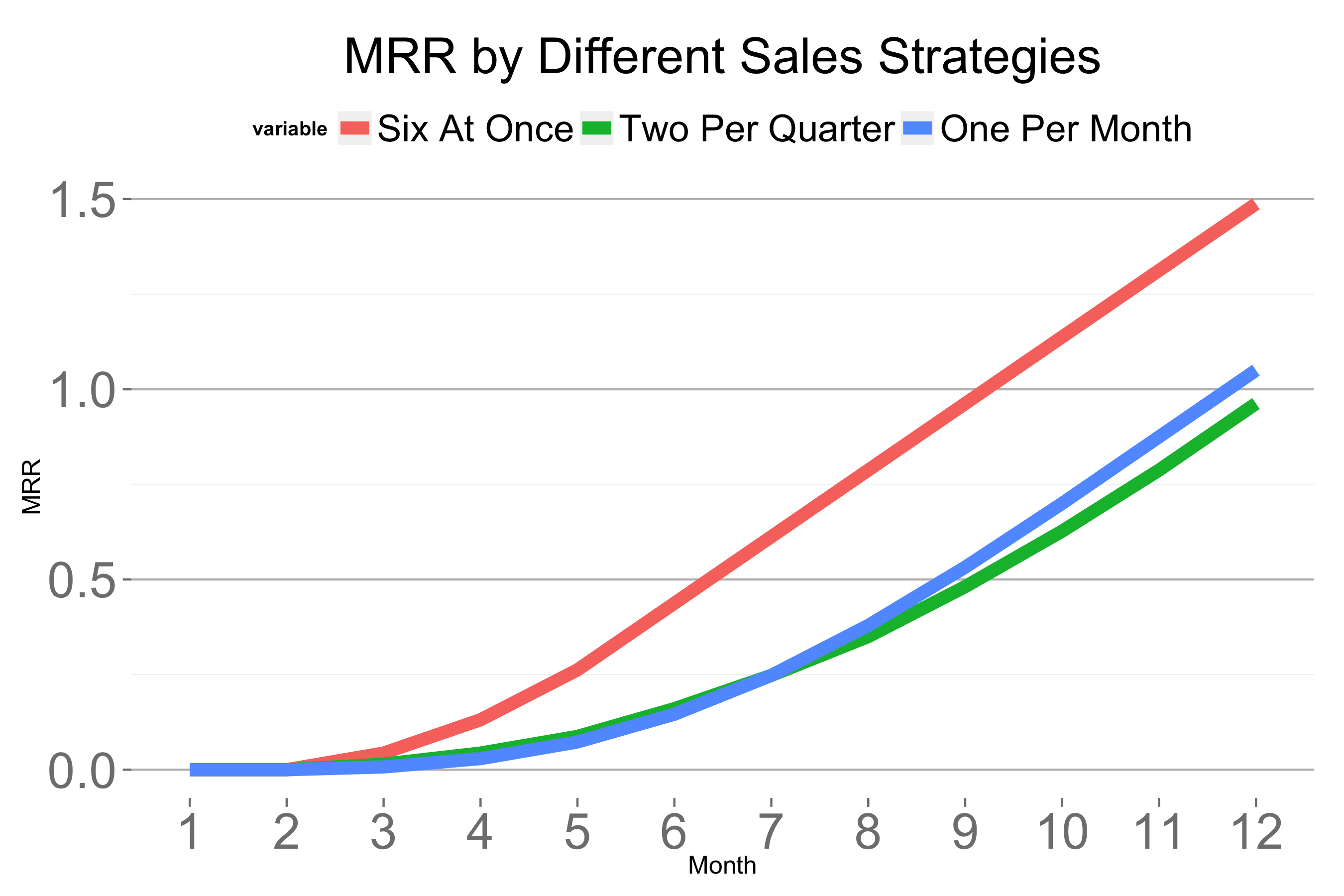

First, let’s compare the financial impact of three different sales hiring strategies: six sales people hired at once, two sales people hired for each of three quarters and one sales person hired each month. In this hypothetical example, the sales people have a $350k annual quota, cost the startup $100k annually, and achieve their quota over six months with the following attainment percentages by month: 0%, 0%, 25%, 50%, 75%, 100%.

Last week, Redpoint held our annual Founder Day gathering. At the event, I listened to the stories of Felix Baumgartner’s record breaking jump from 120,000 feet, heard about the astonishing comeback of the US America’s Cup team and took part in a creativity workshop led by a Stanford Design School professor. In short, the event revolved around doubt.

Last week, Redpoint held our annual Founder Day gathering. At the event, I listened to the stories of Felix Baumgartner’s record breaking jump from 120,000 feet, heard about the astonishing comeback of the US America’s Cup team and took part in a creativity workshop led by a Stanford Design School professor. In short, the event revolved around doubt.

Yesterday, I spoke on a panel at the Gainsight Pulse conference with Aaron Ross, the author of

Yesterday, I spoke on a panel at the Gainsight Pulse conference with Aaron Ross, the author of