2012 was the year of the Seedpocalypse. Also called the Series A Crunch, a fear gripped Startupland : raising a Series A. Two years later, this indigestible excessive bolus of fundraising rounds hit the Series B market & Series Bs became the most challenging round to raise.

Whenever there are “too many” of fundraises of one type, the next round becomes the hardest to raise.

In 2024, the Series A Crunch has returned. Software companies that have achieved the previous era’s milestone, $1m or more in ARR, face a challenging Series A market. Why is this happening again?

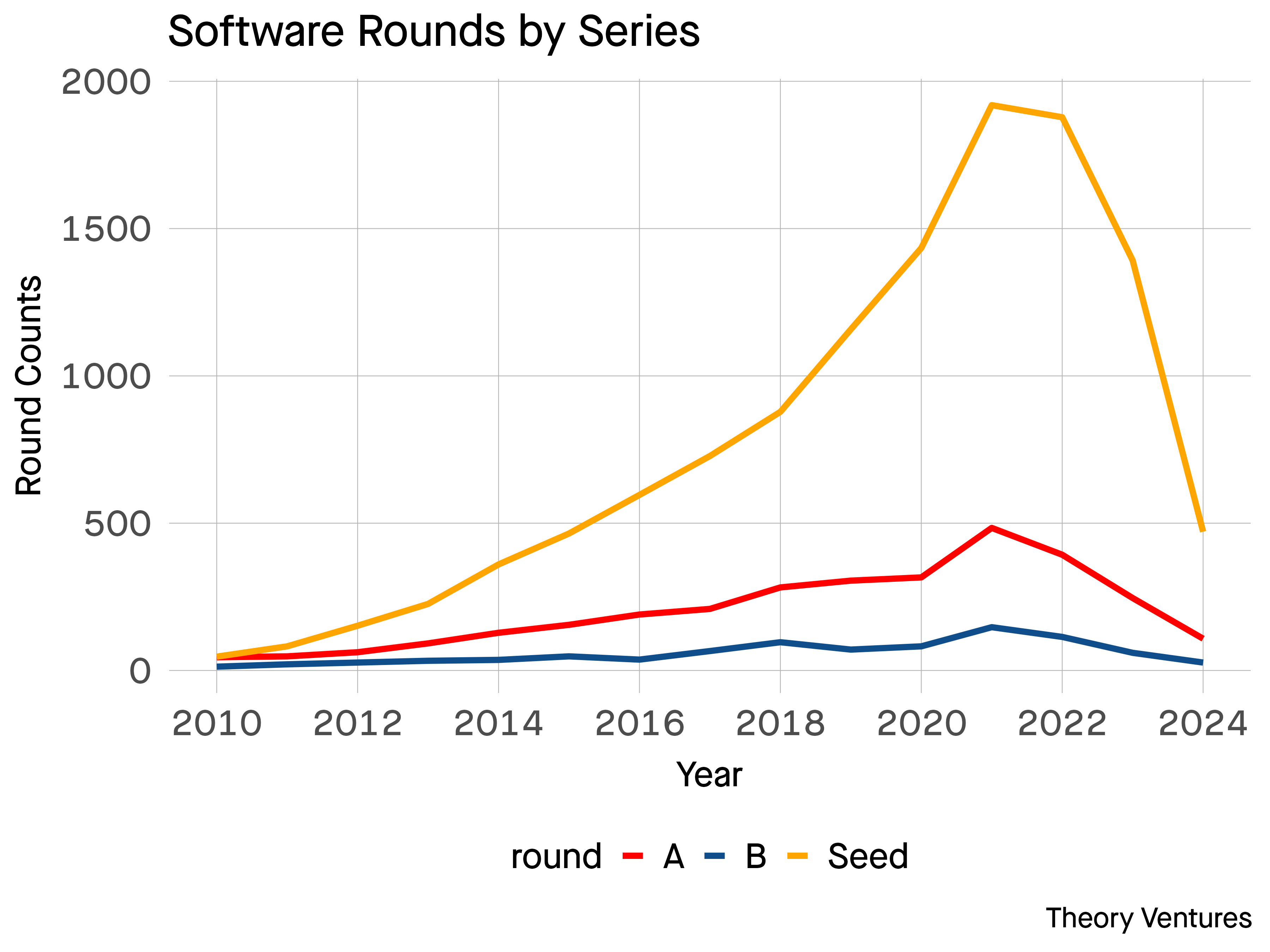

Just as in 2012, a surge in seed investments met a relatively stable Series A market. The supply/demand imbalance creates a funding squeeze.

The orange crush of seed investment has outpaced the growth in Series A & Series B rounds. Many new seed funds started & the rate of company formation surged during the early 2020s driven by an ebullient capital markets.

Also, the definition of a Seed round has changed. The Seeds of the 2010 era are the pre-Seeds of today, making the comparison impure.

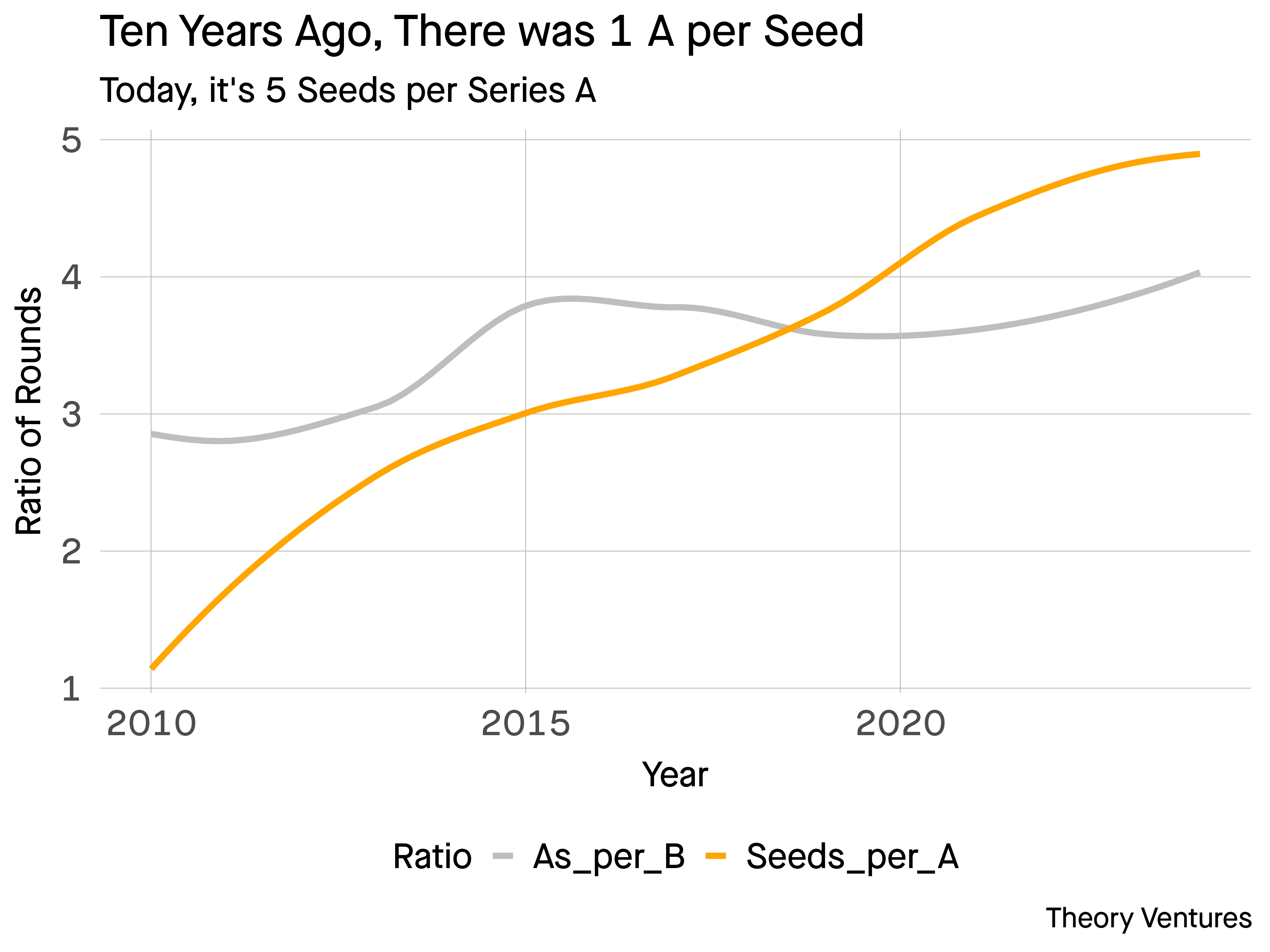

Regardless, Series As haven’t grown to nearly the extent of Seeds. During the last 14 years, the ratio of Seeds to Series As has grown from about 1.1 to 1, to 5 to 1. Meanwhile, the ratio of As to Bs is relatively constant : between 3 & 4 to 1.

With excess seed supply & in an era where forward public software multiples have reverted to the mean from their stratospheric levels, Series A rounds are harder to raise. AI startups, the darlings of the current era, are a notable exception. In this category, the heady multiples of 2021 & 2022 still apply.

But for classic SaaS companies, the Series A Crunch is real. In 18 months, the Series B will again become the hardest round to raise.