Competition is a discovery procedure. — Friedrich Hayek

And developers are discovering the value of open models.

OpenRouter offers a useful view into the model market.1 It is not the whole AI economy. But it is close to the API frontier, where developers can switch models quickly, compare price-performance daily, & route each request to the best available option.

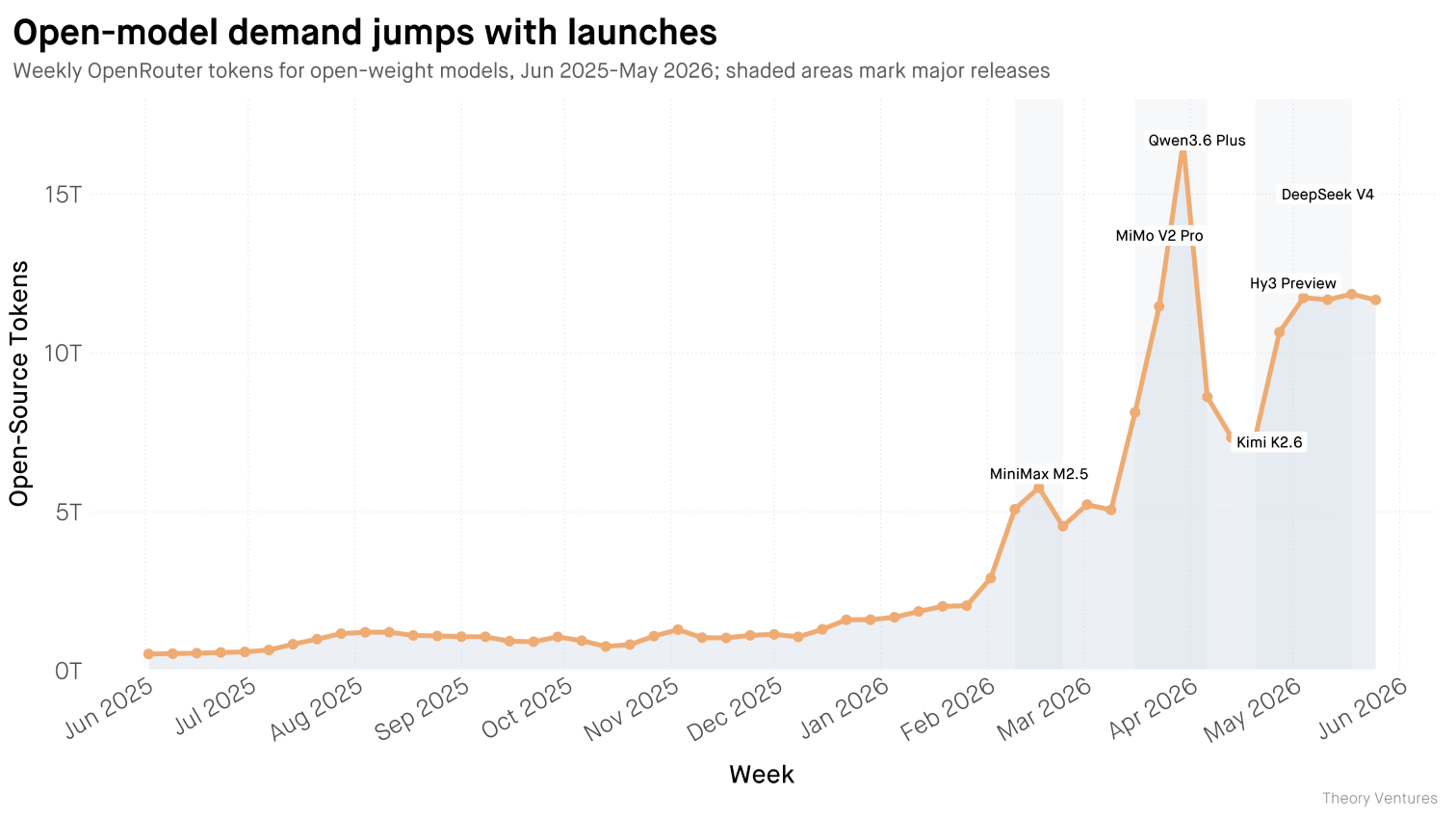

Since 2025, open models have grown sharply on OpenRouter. In the latest model-level snapshot, open-weight models generated 69.1% of named open-versus-closed token volume. Closed models produced 30.9%.

New models attract developer attention & large scale testing, after which token use surges. Each new clustered release of different models sustains a new plateau of token volume.

Just as in the closed-model ecosystem, the competition among open models means rapid innovation & leaderboard changes.

DeepSeek’s early lead gave way to MiniMax & Kimi models in late 2025 & early 2026. Later, launches from MiMo, Qwen, Alibaba’s open-weight model family, Hy3, Tencent’s open-weight model release, & DeepSeek reshuffled share again.

Arcee, a US lab focused, makes a strong appearance recently.

Open models still represent a fraction of overall inference, but the thriving competition, increasing usage, & surge of experimentation suggest developers are increasingly willing to route production traffic to them.

-

Source data: OpenRouter rankings & usage data, analyzed from weekly token-volume snapshots in the OpenRouter analysis dataset. ↩︎