How Much Should You Expect Your Startup to Slow in 2022? About 21%.

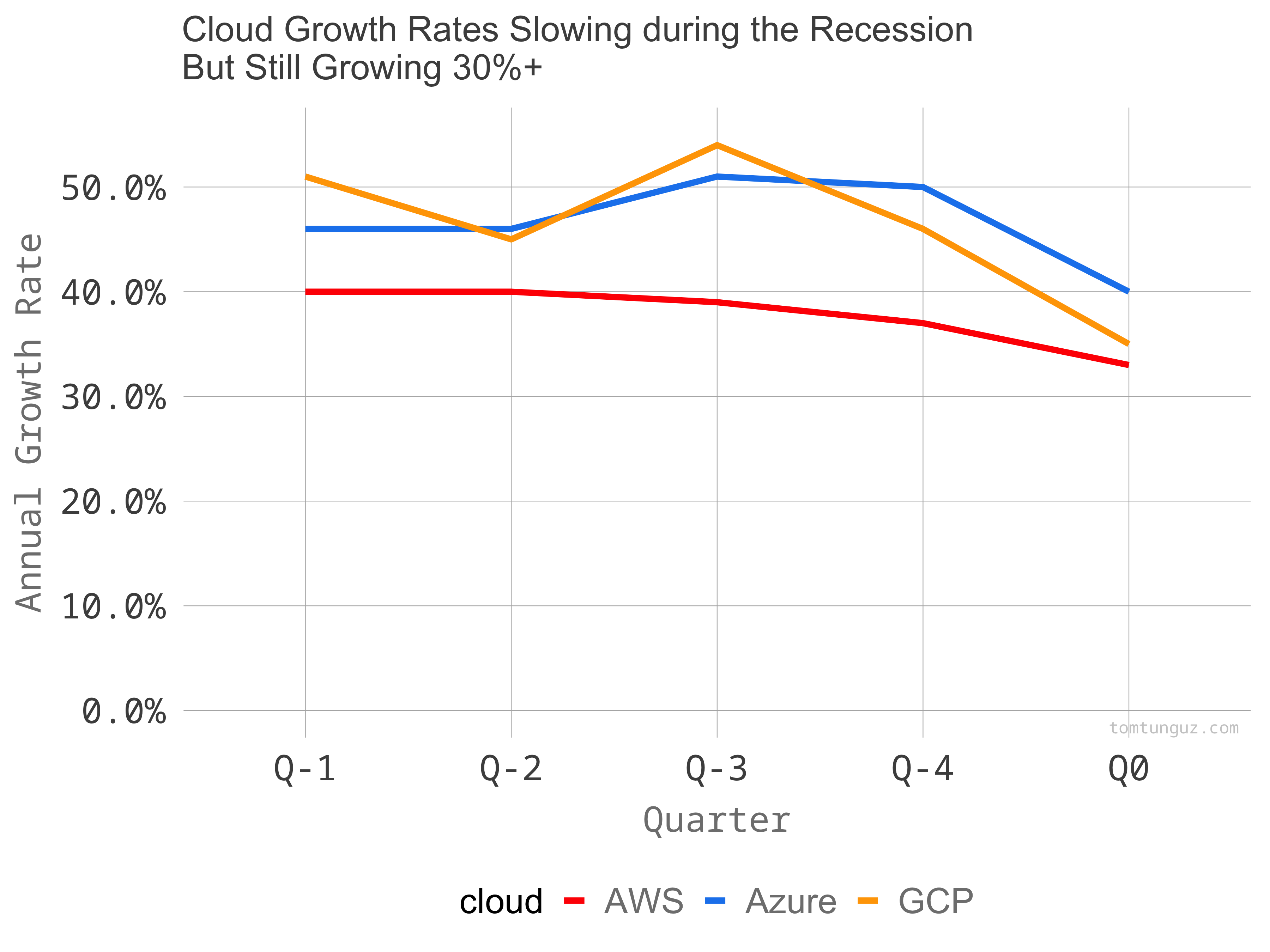

AWS announced earnings earlier today and reported 33% growth. That concludes this quarter’s IaaS earnings scorecard reports & provides us a complete picture of the infrastructure buyer’s index.

AWS’s growth rate is the slowest of the three largest public infrastructure clouds. With about 39% market share, AWS reigns supreme as the largest provider. Larger businesses face more daunting challenges sustaining higher growth rates, so AWS numbers are expected.

On August 11 at 9:30 AM Pacific time, Office Hours will host legendary sales leader

On August 11 at 9:30 AM Pacific time, Office Hours will host legendary sales leader