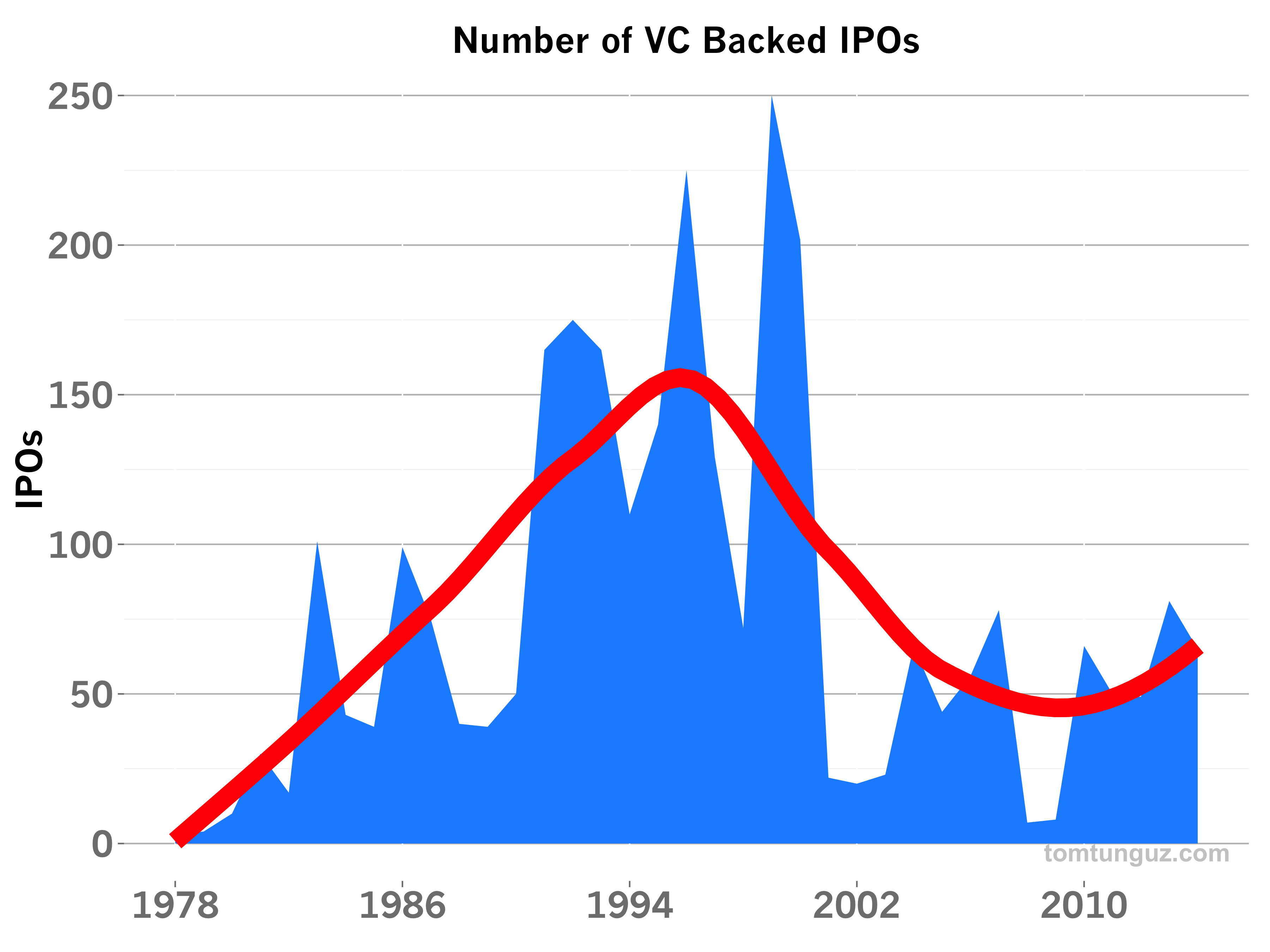

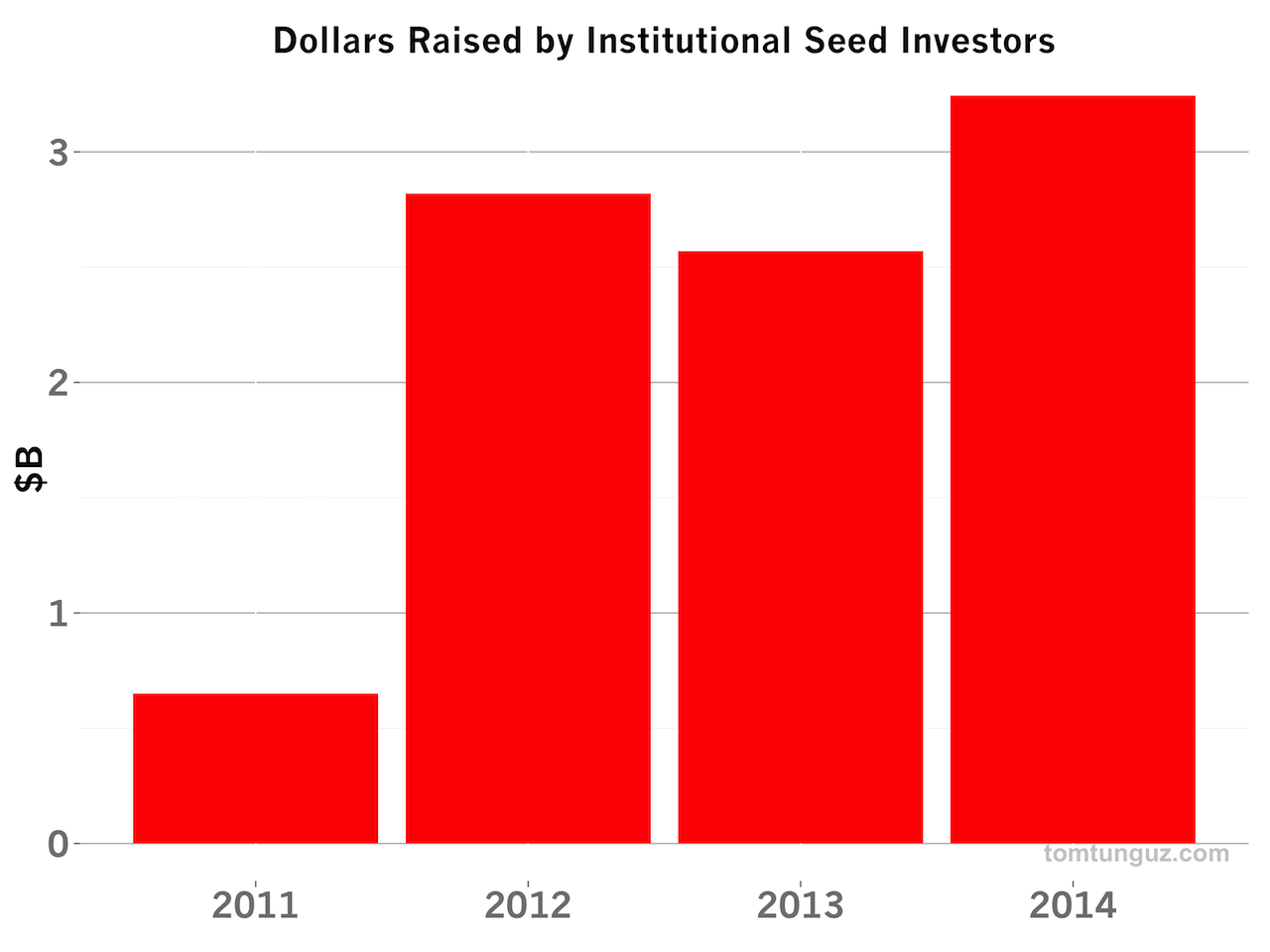

The Three Most Important Trends in the Seed Fund Raising Market

If you’re a founder or potential founder and looking to raise seed capital, you’re entering possibly the most attractive period in a decade to start a business. A few weeks ago,we analyzed the impact of Series A and later stage VCs in the seed market. In the past four years, traditional VCs began to invest in seed-stage companies, which led to a rise in the number and size of seeds. But there’s another, more important force within the seed market: institutional seed investors.