OCTOBER 10, 2025

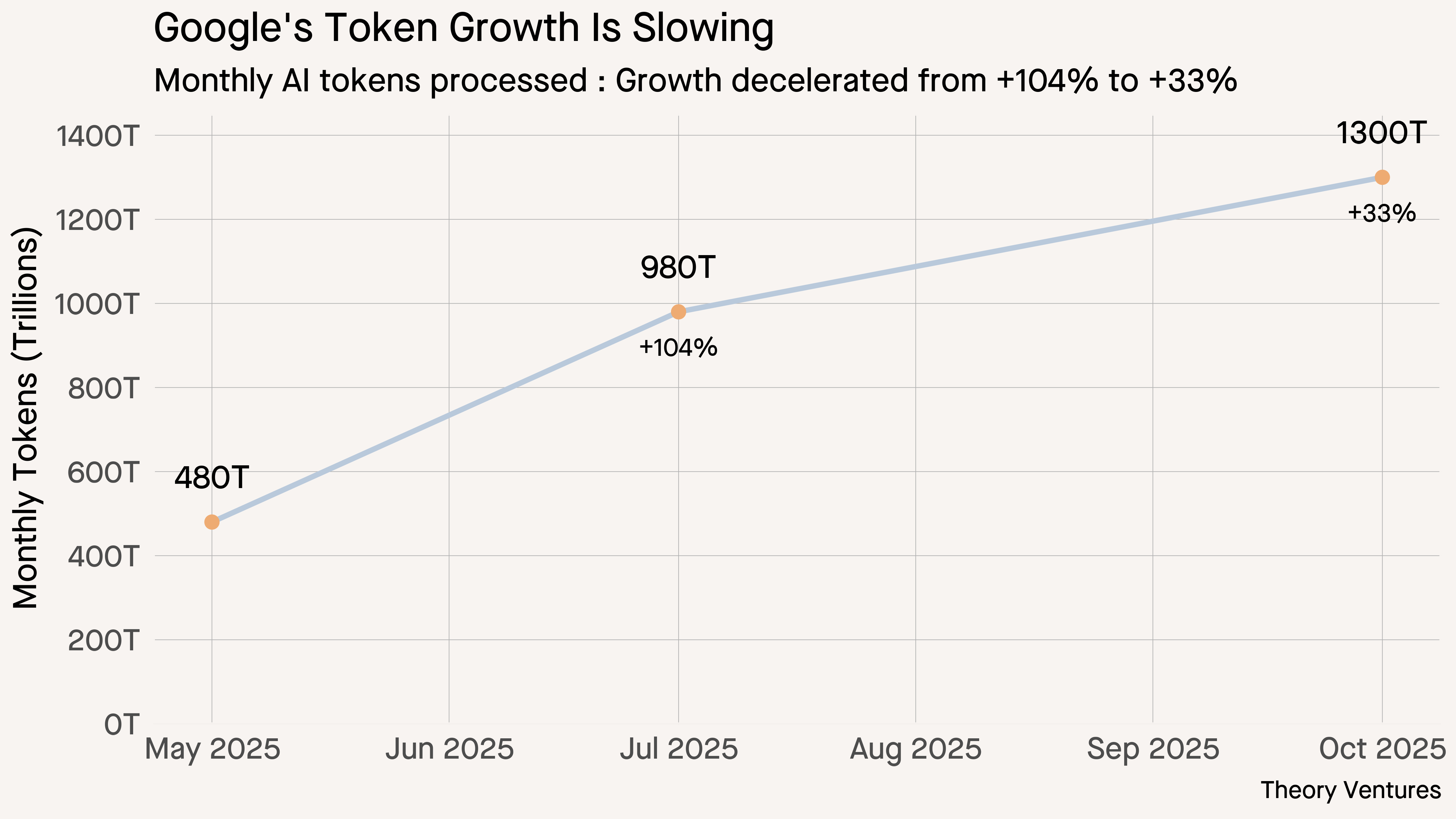

Is Token Consumption Growth Slowing Down?

Google's AI token processing reaches 1.3 quadrillion monthly tokens in October 2025, but growth decelerates from 250T to 107T per month. What's driving the slowdown?